Kustom Entertainment Transforms Amid Media-Tech Convergence

Examining how Kustom Entertainment balances its video tech legacy and entertainment expansion through strategic pivots and competitive challenges.

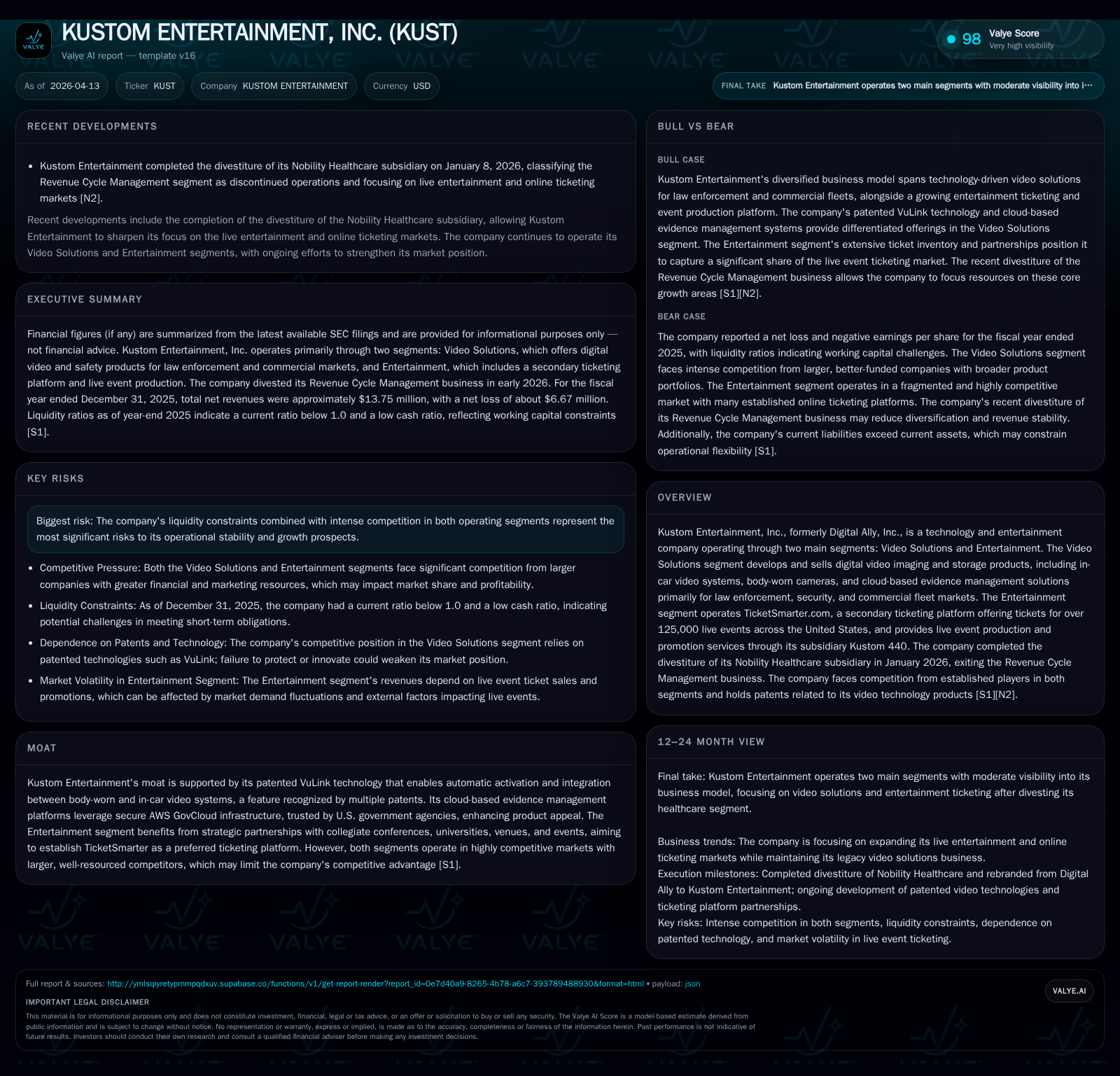

Kustom Entertainment, Inc. operates dual segments: Video Solutions for law enforcement and commercial fleets, and an Entertainment segment centered on TicketSmarter secondary ticket platform and event production. The company’s patented VuLink technology and cloud-based platforms underpin competitive differentiation in video solutions, while TicketSmarter seeks market share through collegiate partnerships. Despite steady revenue around $13.75 million in 2025, profitability remains challenged with operating losses narrowing yet persistent net deficits and liquidity pressures. The recent divestiture of its Revenue Cycle Management business refocuses operations but raises near-term capital allocation questions amid ongoing litigation and competitive intensity in both segments.

Two Sides of Growth: Video Solutions and Entertainment Segments Overview

Kustom Entertainment operates two principal business lines reflecting its hybrid identity as both a legacy technology provider for public safety and an emerging player in live event entertainment.

The Video Solutions segment specializes in digital video imaging products tailored largely for law enforcement, security agencies, and commercial fleets [S3][S4]. Key hardware products include the FirstVu line of body-worn cameras (FirstVu Pro, FirstVu II, FirstVu HD) and in-car video systems (EVO-HD, DVM-800 series). Central to this offering is the patented VuLink technology which enables automatic synchronization and activation between body cameras and vehicle-mounted systems triggered by emergency vehicle signals or g-force events—a significant procedural innovation reducing manual device activation [S21]. Complementing hardware is a suite of SaaS platforms such as EVO Web and FleetVu Manager hosted on AWS GovCloud for secure evidence management, chain-of-custody tracking, and operational reporting favored by government security customers who require compliance with stringent data handling regulations [S21]. This system-level integration is a pillar of Kustom's technological moat.

In contrast, the Entertainment segment drives growth through TicketSmarter.com, a nationwide secondary ticket marketplace boasting listings for over 125,000 live events across sports, concerts, college venues, and theater [S4][S5]. This platform collects service fees as a percentage of ticket face values alongside revenues from tickets held as inventory sourced via primary sellers or partners. Additionally, the wholly owned Kustom 440 extends into event production and promotion services ranging from small private gatherings to large concert festivals, offering end-to-end logistical execution including artist booking and staging [S4]. TicketSmarter has strategically partnered with more than 35 collegiate conferences and hundreds of venues establishing it as a preferred reseller channel within collegiate sports circuits [S12]. These market relationships are critical given the highly fragmented nature of secondary ticketing where brand trust drives consumer choice.

Tracking Recent Financial Performance

Kustom Entertainment’s total net revenues were approximately $13.75 million in fiscal 2025 compared to about $13.52 million in 2024 reflecting overall stability [F1][S3]. The Video Solutions segment reported revenues around $5.1 million while the Entertainment segment generated approximately $8.65 million in 2025 [S3][S4].

Operating loss narrowed year-over-year from roughly -$15.2 million in 2024 to about -$10.9 million in 2025 indicating improving cost control despite ongoing top-line pressures [F1]. Net losses persisted at approximately -$6.7 million [F1]. Operating cash flow improved nearly 50% year-over-year but remained negative at roughly -$5.1 million after capital expenditures which declined sharply to $258k—down over 87% from prior years—signaling constrained investment during this transition phase [F1]. The divestiture of Nobility Healthcare completed early 2026 removed prior revenue cycle management operations classified as discontinued [S18][S19].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -7 | -11 | 0 | -119.1% | |

| 2024 | 35 | -5 | -15 | ||

| 2023 | -10 | -22 | |||

| 2022 | -19 | -19 | -30 | 2 | -174.1% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) |

|---|---|

| 2025 | |

| 2024 | |

| 2023 | 4 |

| 2022 | 4 |

Source: SEC companyfacts cache [F1].

*Note: The unusual positive net income figure for FY2024 may reflect non-recurring items or accounting adjustments since CFO remained negative.

The company faces ongoing liquidity constraints as reflected by a current ratio of approximately 0.86 at fiscal year-end 2025 along with negative free cash flow estimated near -$5.37 million after capital expenditures [F1]. Return on equity is deeply negative near -46%, illustrating sustained losses relative to equity book values [F1].

Competitive Landscape

Kustom’s patented VuLink technology provides a distinctive feature enabling automatic coordination between body-worn cameras and vehicle-mounted devices triggered by various emergency signals—addressing a key operational limitation faced by law enforcement agencies [S21][S16]. This innovation supports their competitive positioning against larger incumbents like Axon Enterprises dominating body-worn camera markets worldwide; Panasonic System Communications serving public safety contracts; WatchGuard Video; and others competing across hardware and software layers [S10]. In commercial fleet markets the company competes against firms such as Lytx (formerly DriveCam), Samsara, and SmartDrive Systems.

Within entertainment ticketing markets served by TicketSmarter intense rivalry exists among established platforms including Ticketmaster (Live Nation), StubHub (eBay), SeatGeek alongside mobile-first resellers [S12]. Kustom differentiates through strategic partnerships encompassing over three hundred universities and more than thirty-five collegiate conferences to establish preferred reseller status within collegiate sports circuits—a niche approach amid broader market fragmentation.

Strategic Outlook & Challenges

Growth initiatives focus on expanding TicketSmarter’s network partnerships across collegiate venues nationwide while scaling recurring cloud subscription offerings within Video Solutions’ SaaS platforms such as EVO Web—targeting increased recurring revenue streams that complement declining hardware sales [S12][S24]. However liquidity constraints combined with working capital pressures pose headwinds alongside escalating component costs influenced by tariffs despite supplier diversification efforts [S7][N1]. The company completed divestiture of its Revenue Cycle Management business early in calendar year 2026 to sharpen focus on core segments [S11][S19].

Capital Allocation & Financial Stewardship

Capital expenditures have contracted significantly from multimillion-dollar levels exceeding $6 million several years ago to approximately $258k in fiscal 2025 signaling tight investment discipline amid restructuring efforts [F1]. Operating losses have driven negative equity returns near -46% illustrating challenging profitability dynamics [F1].

Historically the company engaged in share repurchases totaling roughly $4 million annually during earlier periods but has reduced buyback activity given ongoing losses constraining available capital [F1][S9][S11]. No dividends have been declared reflecting priority on operational stabilization over shareholder returns.

Legal Proceedings Impacting Operations

Kustom remains involved in several legal matters including an unsatisfied judgment nearing $4 million against defendants related to Culp McAuley entities with uncertain collection prospects; however management does not currently anticipate material adverse impact on ongoing operations or cash flows [S6][S8][S13][S14][S22]. Other cases involve breach of contract claims related to pharmaceutical supply failures under negotiation or settled.

The company follows conservative accounting policies recognizing liabilities only when probable and reasonably estimable thereby mitigating unexpected financial exposures though litigation inherently carries uncertainty [S6][S14]. A jury trial scheduled for October 2026 may influence future outcomes requiring monitoring.

Conclusion

Kustom Entertainment exemplifies the complexities faced by smaller firms navigating legacy industrial technologies while pursuing growth through digital entertainment platforms amidst resource constraints. Its proprietary innovations such as VuLink offer unique advantages but remain challenged by larger competitors wielding scale advantages across hardware and software domains. As it executes strategic pivots including segment divestitures alongside managing legal exposures under tight liquidity conditions its ability to deliver sustainable profitability depends heavily on successful scaling of recurring revenue models and strengthening market presence within competitive niches.

Disclaimer: This analysis presents factual information based solely on publicly available filings ([F1]/[S#]) and news ([N#]) documents as referenced above without providing any investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments