EvoAir Holdings Inc.: Assessing Financial Struggles and Growth Ambitions in Eco-Friendly HVAC

EvoAir’s patented green HVAC technology and Asia-focused manufacturing underpin revenue growth but face hurdles from persistent net losses and liquidity constraints.

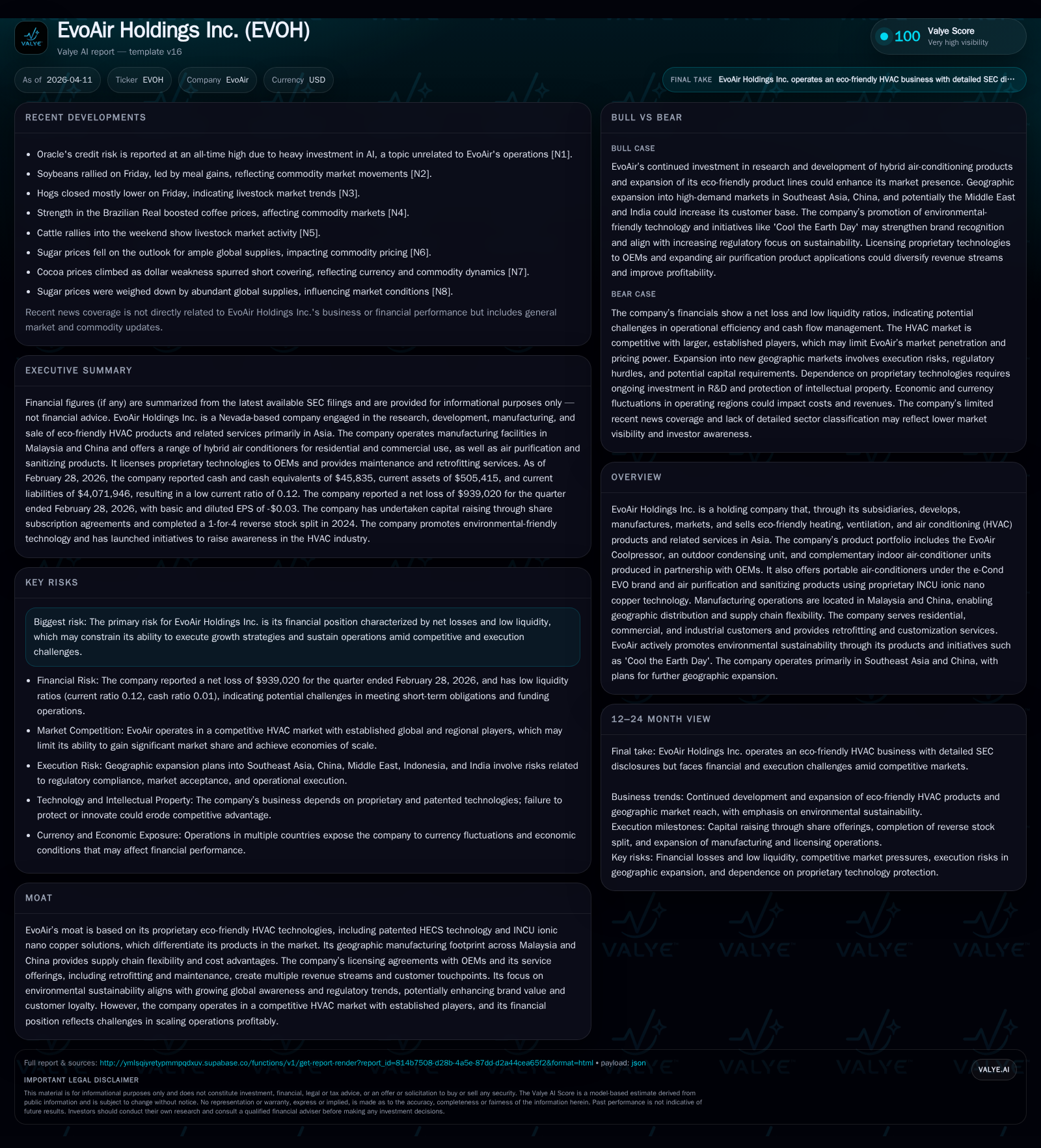

EvoAir Holdings Inc. operates in the eco-friendly HVAC sector with proprietary technologies such as HECS and INCU ionic nano copper, supported by manufacturing facilities across Malaysia and China. Despite a 23% revenue uptick to $135,557 for FY2024, the company has grappled with widening net losses surpassing $25 million and negative operating cash flow, exposing operational and scale challenges. Management targets growth through product diversification, geographic market expansion across Asia, and licensing agreements, offsetting competition and capital limitations. Key milestones include preparations for uplisting on Nasdaq, intended to enhance capital access amid tight liquidity. EvoAir’s ability to convert its innovative technology platform into a sustainable profit profile remains contingent on navigating financial headwinds and execution risks.

Revenue Growth and Operational Performance: Past Trends and Recent Changes

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | -15 | -1158760 | -15 | +43.5% | ||

| 2024 | 135557 | -26 | 30822 | -26 | +23.1% | -327.2% |

| 2023 | 110134 | -6 | -1674395 | -6 | -1.8% | -15.8% |

| 2022 | 112176 | -5 | -1540167 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) |

|---|---|

| 2025 | -1 |

| 2024 | 0 |

| 2023 | -2 |

| 2022 | -2 |

Source: SEC companyfacts cache [F1].

EvoAir Holdings Inc. has evidenced consistent top-line advancement over recent fiscal years driven primarily by its eco-friendly HVAC product sales within Asian markets. Revenue reached $135,557 for the fiscal year ended August 31, 2024 ([F1]), a notable 23.1% increase compared to $110,134 in the prior year. This trajectory underscores demand traction for products like EvoAir Coolpressor outdoor units and e-Cond EVO portable air conditioners.

However, underlying this revenue growth are acute operating challenges typified by persistent negative profitability metrics. Operating income plummeted further into red territory at -$26.3 million in FY2024 from -$6.1 million previously ([F1]). This stark deterioration signals a pronounced struggle with operating leverage—typical of manufacturing-centric HVAC firms facing high fixed costs while scaling volumes insufficiently.

Net income mirrored this exacerbation of losses, swelling from an adverse -$6 million (FY2023) to nearly -$25.9 million (FY2024) ([F1]). Despite incremental revenue gains, fixed cost absorption remains suboptimal indicating scalability constraints.

Operating cash flows captured a fleeting improvement: CFO shifted to a modest positive $30,822 in FY2024 after prior negatives exceeding $1.5 million ([F1]). Yet this improvement lacked sustainability as FY2025 returned to an estimated operating cash outflow near -$1.16 million ([F1]), highlighting ongoing operational stress.

These figures reflect typical sector issues—manufacturing inefficiency coupled with nascent market penetration create a steep path towards profitability even when technologies hold promise.

Drivers Behind EvoAir’s Product Innovation and Geo-Strategic Manufacturing Footprint

EvoAir’s competitive differentiation roots deeply in proprietary eco-friendly HVAC technologies supported by granted patents on its HECS (Highly Efficient Cooling System) platform and INCU ionic nano copper air purification tech ([S1]). Such IP-driven innovation elevates product value beyond commoditized suppliers prevalent in the industrial HVAC landscape.

The company’s core offerings encompass:

- EvoAir Coolpressor: Outdoor condensing units engineered for energy efficiency and low environmental impact.

- Indoor Air Conditioner Units: Developed via OEM partnerships enhancing collaborative market reach.

- e-Cond EVO Portable Units: Capturing the growing portable AC segment amid urban consumer demand.

- Air Purification Solutions: Utilizing proprietary nano copper technology to sanitize indoor air quality.

Manufacturing operations are strategically split between Malaysia and China ([S14]), conferring supply chain agility essential for managing geopolitical trade tensions, fluctuating raw material costs, and region-specific logistical challenges typical of multinational production networks focused on ASEAN and Greater China markets.

This dual-facility footprint acts as an operational moat by enabling cost optimization opportunities, mitigating single-market disruptions while supporting diverse customer verticals ranging residential through commercial-industrial segments.

Financial Position and Liquidity Constraints Impacting Growth Execution

EvoAir’s financial statements outline material liquidity constraints that jeopardize its ability to scale or sustain R&D investments critical for innovation continuation. As of February 28, 2026, current assets stood at roughly $505k against current liabilities exceeding $4 million yielding an alarming current ratio near 0.12 ([F1],[S8]). This stark imbalance reveals severe working capital shortages potentially restricting operational continuity without external funding.

Accumulated deficits have grown steadily from approximately $39.4 million at August 31, 2024 to nearly $55.9 million as of February 28, 2026 ([S3],[S8]) signaling chronic losses eroding shareholder equity.

Cash flow analysis corroborates these issues with sustained negative free cash flow evident: latest fiscal data reflect cash used in operations surpassed investment needs resulting in estimated FCF near -$1.18 million due mainly to operational inefficiencies ([F1]).

Management explicitly acknowledges these going concern risks yet pursues growth strategies premised on external capital raises alongside operational improvements ([S3],[S8]). The delicate balancing act between conserving liquidity while expanding capacity underscores elevated execution risks common among development-stage manufacturing firms aiming at technology commercialization.

Strategic Initiatives Targeting Market Expansion and Product Diversification

To counterbalance financial strains, EvoAir pursues multi-pronged strategic initiatives including broadening its product lineup beyond established offerings toward novel HVAC segments responsive to climate-conscious Asian consumers ([S3],[S5],[S8]).

Geographic expansion efforts aim to deepen penetration within Southeast Asia alongside mainland China leveraging existing manufacturing proximities while exploring licensing models to monetize IP across adjacent markets or private label arrangements ([S3],[S5],[S8]).

Service-oriented segments such as retrofitting existing installations and ongoing maintenance contracts complement product sales enhancing recurring revenue potential—a tactical pivot aligned with industry trends favoring integrated solutions over one-off equipment sales (;[S18]).

While these initiatives align well with sector best practices for diversification amidst competitive pressure, feasibility remains contingent on resolving liquidity limitations that currently hinder scale-up investments required for accelerated market outreach.

Capital Allocation Dynamics: Lack of Dividends, Modest Capex, and Funding Plans

Consistent with EvoAir's developmental stage status amidst financial constraints is the absence of shareholder distributions—no dividends or share buybacks have been recorded recently ([F1],[S10],[S16]).

Capital expenditure decreased sharply from a peak near $146k in FY2024 down to roughly $17k in FY2025 ([F1]), signaling austerity-driven conservation of cash rather than aggressive capacity build-outs. This retrenchment likely impacts future production scaling but is necessitated by immediate liquidity preservation priorities.

Concurrently, management is actively preparing for an uplisting onto the Nasdaq Capital Market intended to broaden access to institutional investors thereby improving fundraising capabilities critical for sustaining R&D pipelines and expanding commercial footprints ([S3],[S5],[S21],[S25]). Such uplisting efforts are archetypal within technology-centric emerging public companies seeking liquidity enhancement amid constrained capital structures.

Overall capital allocation reflects prudent stewardship balancing immediate survival against ambivalent growth aspirations given evolving market access conditions.

Critical Milestones Ahead: Uplisting Plans and Funding Efforts to Watch

The foremost near-term milestones revolve around securing sufficient funding via equity raises catalyzed by anticipated uplisting to Nasdaq—a key step toward legitimizing EvoAir’s capital market presence ([S3],[S5],[S25]).

Market participants should monitor disclosures regarding successful completion of these fundraising rounds as inflection points necessary for executing product rollout expansions or increased marketing expenditures which are presently curtailed due to funding scarcity.

Additionally, operational scaling outcomes including incremental revenue improvements beyond reported modest figures will be important signals validating management's strategy effectiveness under prevailing resource constraints.

Absent clear progress on these fronts, continued financial strain could further imperil R&D momentum critical for sustaining technological competitive advantages embedded within its patented HECS platform.

Risk Assessment: Competitive Pressures, Low Liquidity, and Execution Risks

EvoAir navigates an intensely competitive HVAC industry marked by dominant incumbents with established distribution networks and scale economies which dwarf EvoAir’s modest footprint (;[S1]).

Financially fragile status characterized by persistent net losses above $25 million annually paired with scant liquidity ratios (~0.12) amplifies execution risk notably impacting R&D sufficiency required to maintain technological leadership ([F1],[S3],[S8]).

Liquidity crunches risk stifling operational flexibility increasing dependency on external capital injections which may prove challenging given nascent revenue scales.

Despite promising proprietary eco-friendly technology assets creating an intellectual moat against commoditization pressure, success hinges critically on navigating funding cycles timely while scaling efficiently under intense competitive dynamics common in advanced HVAC sectors.

This analysis synthesizes public SEC filings up through April 2026 alongside company disclosures without offering investment advice or forecasting specific outcomes. Readers should consider inherent uncertainties surrounding early-stage industrial manufacturers navigating liquidity constraints amid competitive markets when evaluating EvoAir Holdings Inc.'s prospects.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments