Magic Empire Global's Financial Volatility and Growth Prospects in Hong Kong Capital Markets

MEGL’s evolving corporate finance advisory services face pressures from market cycles and operational losses despite strong liquidity.

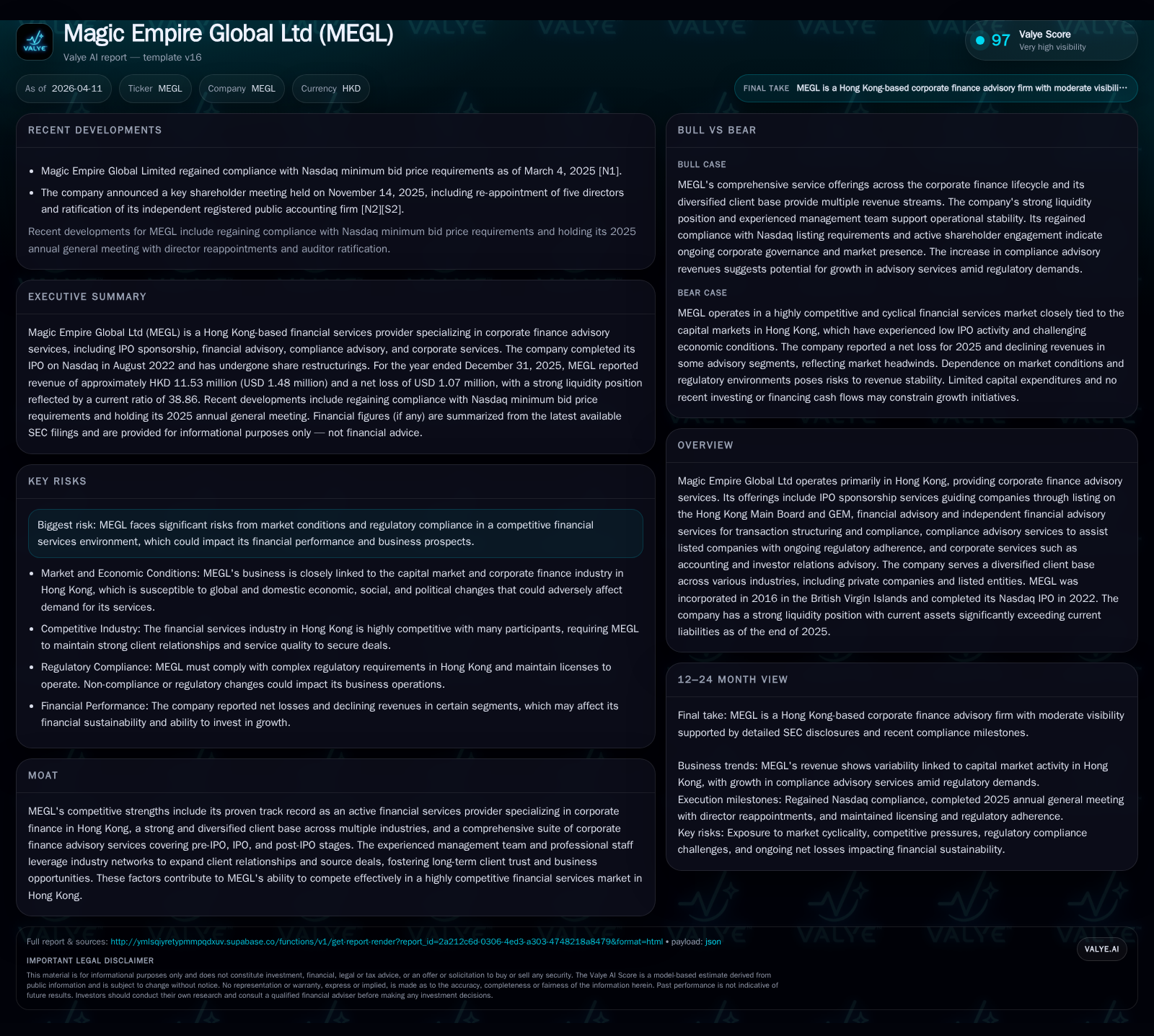

Magic Empire Global Ltd (MEGL), a Hong Kong-focused corporate finance advisory firm, has demonstrated a diversified service offering from IPO sponsorship to compliance advisory. Since its inception in 2016 and Nasdaq listing in 2022, MEGL's financial performance has been challenged by operating losses intensified in recent years. The firm's future growth depends heavily on Hong Kong’s capital markets and regulatory environment, while it maintains a solid liquidity buffer with current assets vastly exceeding liabilities. MEGL's management aims to leverage its experienced teams and industry networks to expand client relationships amid competitive pressures and sector cyclicality.

Company Overview

Magic Empire Global Ltd (MEGL) is a holding company incorporated in the British Virgin Islands in 2016. It operates through subsidiaries based primarily in Hong Kong providing specialized corporate finance advisory services. MEGL's core competencies lie within IPO sponsorship on both the Hong Kong Main Board and GEM markets, financial advisory including independent financial advice for transactions, compliance consulting for listed entities regarding ongoing regulatory responsibilities, and broader corporate services such as accounting support and investor relations advisory [S1][S4][S13][S15].

The company completed its initial public offering on the Nasdaq Capital Market in August 2022 under ticker "MEGL," signifying its ambitions to engage wider capital pools despite maintaining a localized operational footprint [S20][S11]. Over time, MEGL reshaped its share capital structure through authorized share increases, multi-class voting rights adjustments effective late 2024, and a share consolidation executed early 2025 designed to streamline equity distribution among Class A and Class B shares [S11][S10].

Historical Financial Performance

MEGL’s revenue derives substantially from fees tied to IPO sponsorships and various advisory mandates linked closely to Hong Kong's capital market activity. However, over recent years the company has encountered increasing operating losses reflective of sector drag and rising costs.

Historical performance (annual)

| FY | Net ($) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | -1067497 | -871336 | -1543976 | -75.3% |

| 2024 | -608912 | -598615 | -1316417 | -883.1% |

| 2023 | -61940 | 12097 | -360111 | +87.4% |

| 2022 | -492505 | -116690 | -577155 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | ROE% |

|---|---|---|

| 2025 | -6.9 | |

| 2024 | -3.7 | |

| 2023 | 202525 | -0.4 |

| 2022 | 512722 | -2.8 |

Source: SEC companyfacts cache [F1].

Operating income worsened substantially between FY 2023 (-$360k) to FY 2024 (-$1.32m), continuing into year-end FY 2025 with an operating loss of approximately $1.54 million [F1]. Correspondingly, net losses accelerated reaching roughly $1.07 million in FY 2025 after moderate losses previously recorded. Cash flow from operations mirrored this trend with increasing negative outflows ($871k negative CFO at end-2025), indicating increasing cash burn despite relatively stable asset bases [F1]. Dividends paid dropped sharply following FY 2023 likely reflecting the need to preserve liquidity amidst intensifying losses [F1].

Capital Structure and Liquidity

As of December 31, 2025, MEGL reported current assets totaling nearly HK$122 million ($15.7 million USD), dominated by ample cash balances ($15.5 million USD), compared with minimal current liabilities around HK$404 thousand (~$0.4 million USD). This resulted in an exceptionally strong current ratio nearing 39 times—reflecting substantial short-term liquidity buffer sufficient to weather operational losses [F1][S8][S16].

Capital expenditures have been practically dormant since FY 2024 following one-time investments mainly into motor vehicles during FY 2023 [S3][S12][S22]. Financing cash flows have also been largely inactive post-2023 dividend distributions underscoring conservative capital allocation oriented toward operational continuity rather than shareholder returns at present stages [F1][S10].

Business Model and Competitive Positioning

MEGL’s business model revolves around multi-stage corporate finance advisory engagements that span pre-IPO preparations including corporate structuring advice; execution stage IPO sponsorship duties according to stringent Listing Rules; post-listing compliance advisories; financial due diligence; transaction structuring counseling; and ancillary corporate services aimed at supporting issuers across public listing lifecycles [S4][S13][S15].

This comprehensive service suite affords MEGL competitive advantages by creating integrated client relationships facilitating cross-service referrals which can drive deal flow stability even amid market cyclicality. The firm serves a diversified client base across sectors such as online advertising digital ecosystems, real estate development/property management, supply chain logistics/manufacturing chemicals niche segments, education providers as well as natural resources explorations—all prone to varied economic cycles impacting transaction volume differently [S13][S15].

Despite this diversification strategy enhancing resilience somewhat against sector downturns, MEGL publicly acknowledges the critical dependence on broader conditions within Hong Kong’s capital market infrastructure characterized by high competition both from entrenched international banks/firms possessing larger human/financial resources plus numerous local boutique advisory providers competing aggressively on fees which compress profitability during slowdowns [S1].

MEGL’s seasoned senior management team leverages deep local market knowledge and professional networks enabling targeted client acquisition efforts supported by robust compliance risk protocols necessary under tightly regulated environments administered by the Hong Kong SFC governing sponsor roles as well as financial adviser standards ensuring adherence to evolving Listing Rule requirements [S4][S13][S18].

Future Growth Prospects

Growth prospects for MEGL hinge substantially on recovery or expansion phases within Hong Kong’s capital markets that stimulate IPO activities or M&A transaction volumes requiring sophisticated advisory input. Upcoming regulatory reform measures or increased enforcement actions can both raise demand for compliance-oriented advisories but also impose operational complexity requiring sustained investments in staff training/technology platforms—pressures that could cap gross margin improvements despite opportunity expansions [S1].

Additionally, internal capacity constraints particularly managing staff costs—which constitute largest expense line items consisting mainly of salaries/bonuses/Mandatory Provident Fund contributions—are recurring concerns limiting scalability of profit improvements absent enhanced revenue scale or pricing power gains achievable through unique differentiators or expanded geographic footprints beyond current domain focused strictly on Hong Kong exchanges alone [S1].

No explicit forward guidance is provided by the company on exact revenue or profit milestones; however stakeholders should monitor key indicators such as HK IPO deal volumes reported by HKEx statistics; shifts in regulatory policies affecting sponsor appointment practices; client wins within diversified industries signaling penetration increases; and efficiency improvements reflected in narrowing operating loss trends or positive cash flow inflections indicative of turnaround momentum.

Capital Allocation / Returns

Return measures remain depressed given consistent net operating losses over several years leading to negative annualized approximate ROE of about -6.9% when comparing trailing twelve months’ net loss against total equity levels approximated near $15.6 million end-2025 [F1]. Dividend payments were discontinued after FY 2023 consistent with preservation strategies amid profitability challenges while no share buybacks have been reported indicating restrained shareholder capital return activities reflective of focus on stabilizing core operations first [F1][S10].

Risks

MEGL faces significant risks deriving chiefly from volatile global/local economic conditions feeding into fragile capital market sentiments that directly reduce IPO pipeline sizes or delay transactions impacting fee-based revenues unpredictably. Regulatory changes modifying sponsor or advisor qualifications or engagement scopes could disrupt established client pipelines necessitating adaptative responses possibly incurring incremental costs.

Competition is further intensified by players possessing superior brand recognitions or deeper resource pools capable of aggressive pricing/multi-jurisdictional cross-selling making retention/acquisition more difficult especially for mid-tier active participants like MEGL.

Staff cost escalations without corresponding revenue growth would depress margins further aggravating net loss levels.

Finally, currency fluctuations present secondary risk elements but are partly mitigated given business conducted predominantly in HKD paired with disclosed stability assumptions around USD/HKD exchange pegging mechanisms sustaining consistent reporting comparability periods [S18].[F1]

Conclusion

Magic Empire Global Ltd exemplifies a niche corporate finance advisor focusing intently on servicing IPO sponsors along with post-listing compliance clients within the competitive yet strategically important Hong Kong financial ecosystem. Despite facing ongoing profitability headwinds shaped by sectoral cyclicality and expense inflation pressures reflected unmistakably in rising operating losses peaking at over $1.5 million annually recently coupled with negative cash flows from operations,[F1] the company retains substantial liquidity cushions enabling continued operation without immediate solvency concerns.[F1]

Its comprehensive service portfolio combined with management expertise provide a foundation for potential recovery anchored on cyclical improvements or strategic enhancements though transparency regarding forward trajectory remains limited formally.[N/A]

Investors or stakeholders monitoring MEGL should emphasize developments around Hong Kong capital market health metrics alongside company disclosures relating to client acquisition momentum or margin optimization initiatives which collectively will dictate medium-term viability within an intensely competitive arena.

Disclaimer: This analysis is based solely on publicly available disclosures including SEC filings up to April 10, 2026 ([F1],[S#]) without incorporating non-public data or proprietary insights. It does not constitute investment advice but rather an objective assessment highlighting historical performance factors alongside prospective opportunities and risks inherent within Magic Empire Global Ltd’s operating environment.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments