TV Channels Network Inc.'s Quest for Streaming Scale: Exclusive Content versus Capital Constraints

TV Channels Network blends niche exclusive concert content with an ambitious streaming platform, contending with capital and scalability hurdles in a crowded media space.

TV Channels Network Inc. (TVCN), founded in 2022, operates a proprietary pay-per-view streaming platform offering over 300 national channels and 100 live concert channels featuring exclusive legacy content such as the Legends of Classic Soul series. Despite a well-defined niche anchored by these exclusive licenses, TVCN has yet to generate revenue and faces acute capital limitations alongside critical infrastructure scalability challenges. The company plans aggressive subscriber acquisition backed by digital marketing but competes against streaming giants with vastly superior resources. Success hinges on rapidly scaling its technology and subscriber base while managing fixed licensing costs and liquidity constraints.

Early Growth Trajectory and Initial Business Milestones

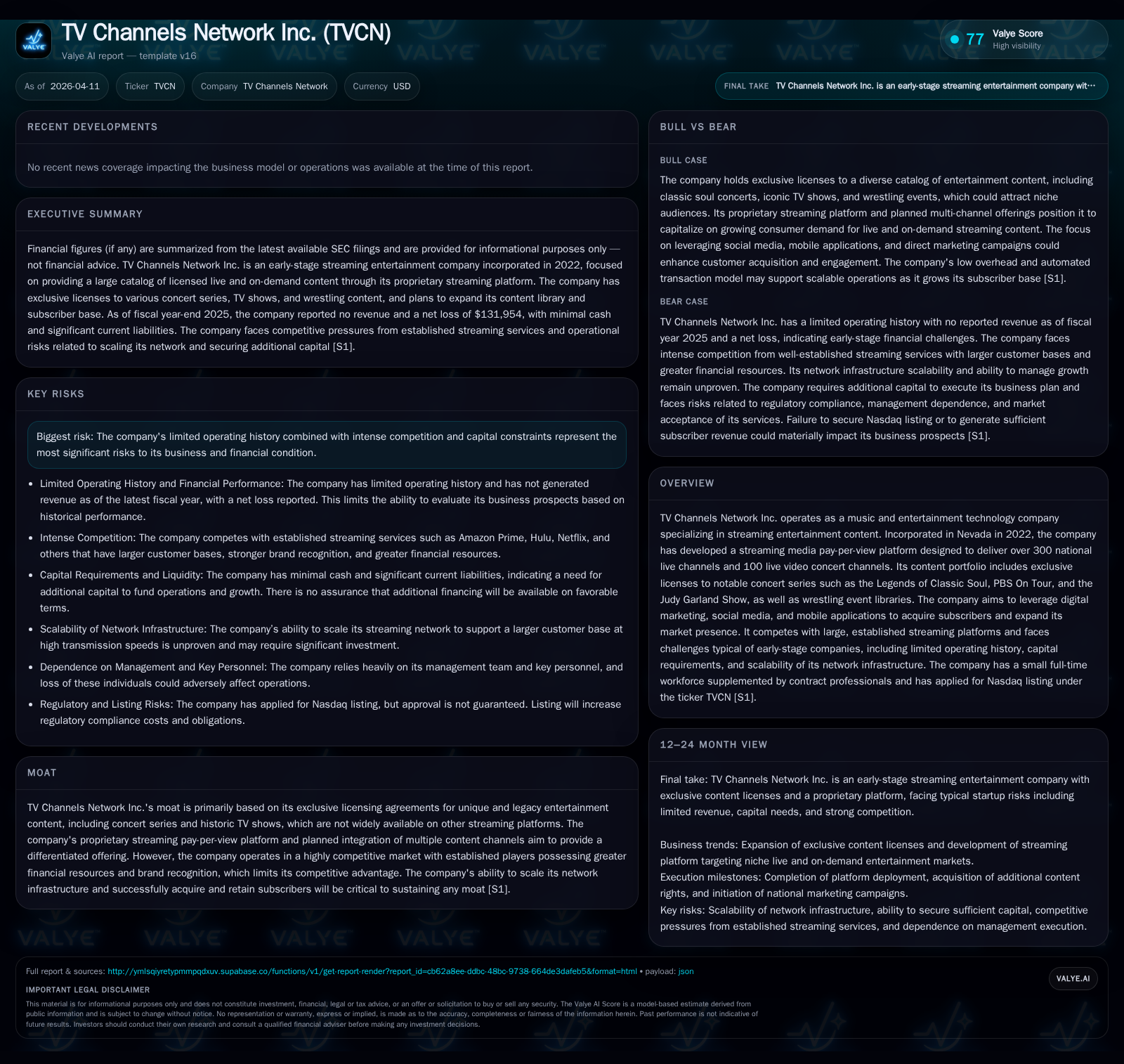

Incorporated in August 2022 in Nevada, TV Channels Network Inc. (TVCN) has had a highly limited operating history to date [S1][S26]. Its activities since inception have centered on establishing the corporate structure, drafting business plans, initial equity funding primarily from related-party sources, performing due diligence on online content suppliers, and initiating strategic referral partnerships targeting niche communities such as investment newsletters [S1][S26]. As of fiscal year-end 2025, the company reported zero revenue but incurred operating losses totaling approximately $131,954 USD reflecting pre-launch operations cost structures mainly aligned with platform development efforts [F1].

TVCN aims to differentiate itself as a premium streaming entertainment provider by launching a proprietary streaming pay-per-view platform that offers users access to over 300 national live channels supplemented by roughly 100 live video concert channels. The company intends to generate positive revenue within 45 to 60 days following its anticipated go-live date post-offering closure through various premium channel subscription packages [S1]. The historical lack of revenue combined with nascent operational milestones underscore investor caution given the absence of proven commercial traction.

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Exclusive Content Licensing as a Differentiator

A core competitive asset underpinning TVCN's strategy resides in its portfolio of exclusive content licensing agreements. These include six-year exclusive rights to the "Legends of Classic Soul" concert series—featuring revered soul groups such as The Four Tops and Harold Melvin's Blue Notes—and other significant holdings like the PBS On Tour concert library (~52 one-hour shows from 1997), historic wrestling event libraries through World Class Pro Wrestling partnerships, as well as a collection of 26 episodes from CBS's Judy Garland Show [S1][S5][S24].

These curated legacy assets create a differentiated niche in the broader streaming landscape dominated by players focusing on recent popular programming or broad movie libraries. TVCN’s ability to monetize these unique catalogs via its integrated video-on-demand pay-per-view platform aims at serving consumers attracted to rare concert footage and classic entertainment not readily accessible elsewhere.

Despite this moat potential, the exclusivity is bounded by the relatively specialized appeal of legacy concerts which might limit scale versus mass-market subscription services. Moreover, fixed multi-year licensing arrangements represent substantial up-front costs decoupled from usage metrics—a precarious cost structure demanding rapid subscriber uptake for profitability [S28].

Infrastructure Scalability and Technology Risk Factors

TVCN’s proprietary streaming media pay-per-view platform represents a tactical endeavor intended to simultaneously distribute hundreds of live channels and concert feeds with high-definition quality. However, the company's scant prior deployment experience introduces material uncertainties regarding its capability to scale network infrastructure effectively under high concurrent demand scenarios [S7].

Delays or underperformance in bandwidth provisioning could degrade user experience considerably. The system relies heavily on third-party telecommunications providers for transmission capacity; any failure or limitation imposed by these providers—notably if they compete or terminate contracts—may compromise service delivery and cause customer attrition [S8]. Furthermore, infrastructure upgrades required to sustain downstream transmission speeds are likely capital-intensive undertakings potentially straining already scarce financial resources.

The fast-evolving nature of streaming technology further demands agility which TVCN may lack compared to established incumbents capable of continuous innovation investments [S20]. These operational scalability risks stand as critical obstacles that must be overcome for sustainable growth.

Customer Acquisition Strategy and Market Positioning

Facing established competitors with deep pockets and sizable customer bases necessitates an aggressive yet efficient marketing strategy for TVCN. The company plans extensive utilization of national TV advertising campaigns coupled with robust digital promotion across social media networks including Instagram and Facebook targeting both general consumers and niche segments inclined toward classic music content genres [S3][S4][S6].

Mobile applications synchronized across multiple digital devices form another pillar given prevailing consumption trends favoring smartphones and tablets over traditional viewing modes. Strategic partnerships such as cross-branding initiatives with industry-specific newsletters also contribute to direct sales efforts enhancing brand visibility among targeted demographics.

TVCN emphasizes automation within its web-based service operations aiming for high-margin transactional business models scalable without corresponding increases in overhead—a notable advantage if execution proceeds smoothly [S3]. However, establishing brand recognition remains challenging as low barriers to entry enable numerous allied players to compete for consumer attention.

Capital Structure, Allocation, and Financial Health

Financial data reveals stark liquidity constraints characteristic of many early-stage streaming ventures attempting simultaneous platform development and content licensing. As of December 31, 2025 data indicates total cash equivalents on hand at $191 against current liabilities nearing $400K conveying severe short-term funding stresses that demand near-immediate resolution [F1][S15]. Operating losses reflect continuing expenditures predominantly related to technology buildout rather than commercial sales balance.

No dividends have been declared nor share repurchase programs initiated consistent with typical growth-phase priorities focused exclusively on reinvestment rather than returns distribution to shareholders [F1][S9]. Capital allocation presently prioritizes completion of platform features coupled with securing additional exclusive content rights poised to expand future offering breadth.

The company anticipates further financing rounds may be necessary given current resource depletion risk—but terms remain uncertain—potentially leading to shareholder dilution observed frequently among similar firms [S23]. This delicate balance constitutes one of the principal impediments facing management going forward.

Competitive Landscape: Challenges from Established Streaming Giants

Competition extends beyond pure-play video-streaming platforms including Netflix, Hulu (Disney-owned), Amazon Prime Video—and hybrid linear-IPTV services like DIRECTV Now—to encompass event promotion entities such as Live Nation specializing in live music experiences albeit not primarily digital distributors [S1][S7][S28]. These incumbents possess entrenched market penetration paired with expansive content libraries spanning fresh releases presented alongside back catalogs.

Disparities extend deeply into financial firepower where TVCN’s modest operating scale inhibits aggressive pricing or expansive technology experimentation without risking crippling cash burn rates. Customer loyalty establishes another hurdle; mainstream consumers gravitate toward familiar brands integrating multiple entertainment verticals whereas TVCN occupies predominantly niche oldies-concerts territory requiring convincing value propositions against established lifestyle subscriptions.

Pricing pressure within streaming markets coupled with rapid technological shifts can induce elevated churn adversely impacting lifetime value calculations especially given fixed upfront licensing costs intrinsic in TVCN’s model impeding margin stability unless critical mass is reached swiftly.

Future Growth Prospects and Strategic Constraints

TVCN envisions scaling its content portfolio substantially — targeting management’s stated goal of managing around 5,000 entertainment titles by year-end 2024 across various formats including movies, original/exclusive programming alongside live linear network licenses — aimed at broadening customer appeal beyond initial concerts niche [S5].

Product roadmap mentions expansion into artist production management fostering new recording artists plus increasing wrestling/sports event offerings providing diversified revenue streams contingent upon financing availability. Enhanced cloud-based audio/video distribution solutions promise improved supply chain visibility intended to increase operational agility during scale-up phases.

Nevertheless growth ambitions are tempered heavily by existing capital shortfalls plus operational risks tied to infrastructure scalability highlighted earlier — inflection points requiring careful navigation lest aggressive expansion outpace financial capacity causing execution strain.[S1]

Forward-looking Considerations: Key Milestones and Investor Watchpoints

With no explicit forecast guidance provided in public filings beyond qualitative remarks about impending platform launch timelines post-equity offering closure investors should closely monitor:

- Actual go-live date execution aligning with stated monthly subscription revenue goals within first two months post-launch;

- Subscriber growth trajectory metrics signifying market acceptance;

- Progress on upgrading telecommunications bandwidth capabilities critical for multi-channel HD streaming performance;

- Subsequent capital raises or strategic partnerships enabling sustained investment into additional rights acquisitions;

- Management execution robustness evidenced through timely marketing campaign roll-out efficacy;

- Development progress toward expanded interactive social media integrated applications attuned to mobile-first audiences.

These discrete milestones collectively determine whether foundational assumptions behind business plan fruition prove valid or require strategic recalibration given competitive intensity plus technological uncertainties.

Summary: Weighing Opportunity Against Operational Risks

TV Channels Network Inc.’s proposition rests broadly on harnessing a narrowly defined exclusive content moat comprising historic concert series plus select sports/wrestling libraries distributed through an integrated multiple channel pay-per-view streaming platform designed for next-generation user experience. This offers scope for differentiation within large but fragmented online entertainment markets dominated predominantly by mass-market incumbents.

However substantial risks surround:

- Scaling the technology stack adequately amidst service reliability demands;

- Managing fixed long-term licensing payment obligations absent immediate revenue inflows;

- Overcoming acute liquidity shortfalls impairing timely go-to-market initiatives;

- Achieving effective subscriber acquisition sufficient to justify escalating operating costs;

- Maintaining brand strength amidst fierce competition backed by heavy investment budgets.

While management’s vision aligns credibly with emerging consumption patterns favoring multi-device mobile synchronization coupled with niche legacy content appeal limitations fundamentally stem from financial resource scarcity constraining operational flexibility making business outcomes highly dependent on flawless execution across several dimensions simultaneously.

This analysis underscores the imperative for stakeholders to track near-term execution milestones carefully balanced against inherent early-stage venture uncertainties embodied throughout TVCN’s narrative disclosures.

Disclaimer: This report is prepared solely for informational purposes based on publicly available SEC filings as of April 2026. It does not constitute investment advice or recommendations. Readers should conduct independent due diligence before making any financial decisions related to TV Channels Network Inc.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments