ChampionsGate Acquisition Corp: Weighing Growth Prospects Against Redemption Risks

A comprehensive assessment of ChampionsGate Acquisition Corp’s early SPAC performance, target acquisition approach, and the nuanced impact of shareholder redemption rights.

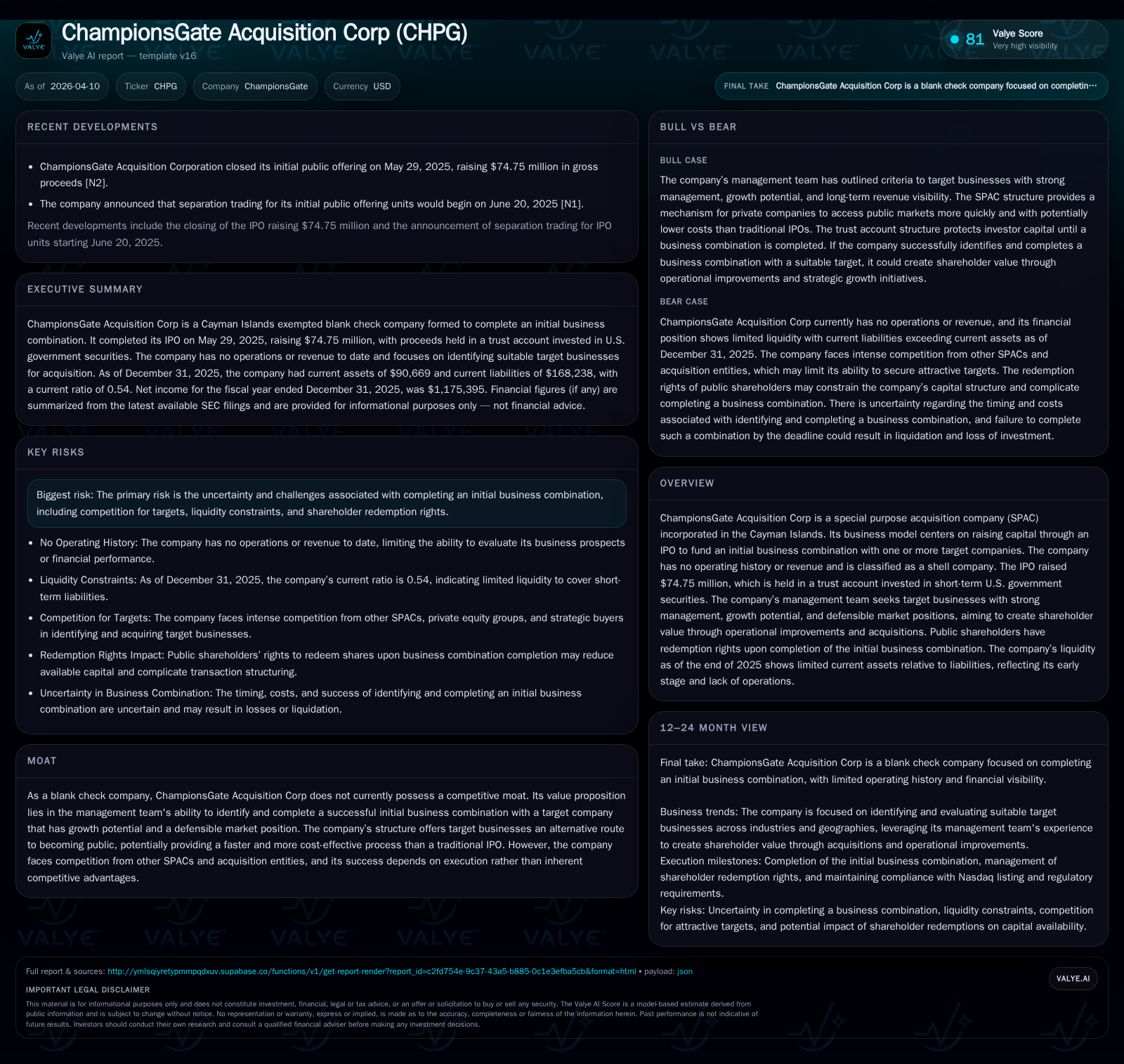

ChampionsGate Acquisition Corp, a Cayman Islands-incorporated blank check company, initiated its IPO in May 2025 raising approximately $74.75 million to pursue initial business combinations with promising targets. Its management team emphasizes selection of firms with strong leadership, organic and acquisition-driven growth potential, and defensible market positions while leveraging public company benefits. However, operational history is absent, and financial metrics reflect typical SPAC early-stage dynamics with negative operating income but positive net income due primarily to non-operating factors. Public shareholder redemption rights create significant deal structuring challenges, squeezing available capital and complicating negotiations. The company must complete its acquisition within prescribed timelines or face liquidation at IPO proceeds levels, all amid rising competition for attractive targets in the saturated SPAC market.

From IPO to Present: Performance Snapshot of a Blank Check Company

ChampionsGate Acquisition Corp completed its IPO on May 29, 2025, issuing 7,475,000 units (including overallotment) at $10 each, accruing gross proceeds of about $74.75 million [S5]. This capital is held in a U.S.-based trust account maintained primarily in short-term U.S. treasury bills with maturities under 185 days or equivalent government money market funds [S8], ensuring principal protection while generating minimal interest income.

Given its status as a Cayman Islands exempted entity classified as a shell company, ChampionsGate lacks operations or revenue streams to date [S1][S5]. The company recorded an operating loss of approximately $603K for the fiscal year ending December 31, 2025—the deficit stemming mostly from administrative and offering-related expenses without offsetting operational income [F1]. Meanwhile, a net income figure of about $1.17 million emerges from non-operating activities such as interest accrued on trust funds or accounting treatment effects rather than earnings from business operations [F1]. Liquidity is tight relative to short-term liabilities; current assets approximate $90.7K against $168.2K in current liabilities yielding a current ratio of roughly 0.54—indicative of limited working capital outside the trust account [F1]. This profile is typical for SPACs pre-acquisition where major assets are restricted in trusts, underscoring the company's initial developmental phase.

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Note: Revenue is absent due to lack of operating activity; ROE computed using net income relative to equity reflects losses resultant from operating expenses.

Management's Criteria for Target Selection: Searching for Growth and Market Defensibility

The management team explicitly focuses on identifying target businesses that align with several strategic pillars: well-established management capable of driving growth and profitability; niche deal sizes amenable to expansion via organic revenue growth complemented by synergistic add-on acquisitions; long-term revenue visibility supported by defensible market positions near inflection points such as product innovation opportunities or operational enhancements; and advantage from transitioning into U.S.-public company structures that afford marketing and capital raising opportunities [S3].

This selective approach ensures focus on smaller enterprises that might be overlooked by larger acquirers but have latent growth potential exploitable through tactical operational improvements—leveraging public listing benefits like enhanced liquidity, investor access, and acquisition currency advantages that help accelerate value creation over time [S3]. By targeting such entities close to pivotal transformational junctures (e.g., scaling management capabilities or launching novel products), ChampionsGate aims to maximize equity appreciation post business combination.

Redemption Rights and Their Impact on Deal Structuring and Target Negotiations

A defining dynamic influencing ChampionsGate's business model revolves around shareholder redemption rights. Upon completion of the initial business combination—or related shareholder approval processes—public shareholders may elect to redeem their Class A ordinary shares for cash equal roughly to the per-share balance held in the trust account plus accrued interest (initially anticipated as around $10 per share) [S7][S8]. This creates an inherent capital uncertainty: if substantial redemptions occur, the pool of funds available for deployment into acquisitions shrinks directly.

To mitigate disproportionate blocking risks by single large holders exerting undue leverage via redemptions exceeding a threshold (set at no more than 15% of IPO shares per beneficial owner without prior consent), ChampionsGate established contractual limitations aiming to discourage abusive redemption practices while preserving broad shareholder voting rights [S9][S12]. Nonetheless, these rights inject complexity into negotiations because potential target businesses—and their advisers—can view high redemption risk unfavorably since it elevates execution uncertainty and reduces available cash consideration.

Furthermore, redemption rights introduce structural constraints whereby the company must balance maximizing transaction value with securing adequate post-transaction capital structure stability—often requiring sponsor participation via private investments or loans if redemptions exceed expectations [S1][S8]. This tradeoff naturally tempers transaction flexibility and demands diligent investor communication strategies.

Capital Structure and Allocation: Trust Account Management and Funding Constraints

Capital raised through the IPO is sequestered largely within a trust account dedicated solely to safeguarding investor contributions pending completion of the initial business combination or liquidation events [S5][S8]. Under regulatory rules aligned with Rule 2a-7 of the Investment Company Act, funds may only be deployed toward approved purposes including taxes arising from interest earnings but otherwise cannot be used for operational expenses prior to transaction consummation.

Absent any revenues or earnings-generating activities presently, ChampionsGate finances ongoing formation and search-related costs through proceeds outside the trust—which stem from sponsor private placements totaling about $2.3 million—and loans from affiliates as required during this pre-combination phase [S5][F1]. No dividends or share buyback programs exist given the company’s nascent lifecycle and zero operational cash flow generation capacity today [F1][S4][S8].

Overall capitalization is structured conservatively with fund preservation prioritized until an appropriate target is secured and combined into a post-merger public entity while managing dilution through founder shares retention by sponsors.

Forecasting Milestones: What Success Looks Like for ChampionsGate

Key upcoming milestones revolve centrally around successfully identifying and closing an initial business combination by November 29, 2026—the stipulated deadline per current charter which may be extended to August 29, 2027 subject to amendments—and satisfying Nasdaq listing requirements including achieving requisite ownership thresholds post merger to maintain exchange compliance [S1][S9].

Should ChampionsGate fail to consummate such combination by these deadlines, it will cease operations except for termination procedures which involve prompt redemption of public shares at approximately the IPO price plus accrued interest (subject to minor dissolution expense deductions) while warrants become worthless—a liquidation scenario posing downside risk for investors seeking upside exposure [S1][S9].

Future events also include strategic evaluations on whether shareholder approvals will be pursued depending on regulatory requirements or tender offer rules surrounding proposed combinations—a discretionary decision impacting timing and structure of redemption processes alongside proxy solicitation activities [S7][S14]. Monitoring public vote participation rates will be crucial as quorum requirements could influence transaction progress.

Risk Factors Unique to ChampionsGate’s Business Combination Strategy

Several material risks underscore ChampionsGate’s current state: its foundational lack of operating history prevents traditional fundamental analysis on performance prospects; auditors express substantial doubt about ongoing viability absent successful mergers (going concern risk) emphasizing dependency on timely business combinations; competitive pressure grows amid an expanding universe of SPACs scrambling for a limited number of viable targets potentially inflating acquisition prices or causing bidding failures; prevailing macroeconomic volatility—including capital markets turbulence cited in filings—further clouds financing possibilities; redemption rights create execution risks where large-scale redemptions curtail deployable capital compromising deal attractiveness; lastly jurisdictional complexities related to Cayman incorporation may inject additional governance nuances impacting shareholder protections compared with domestic entities [S1][S6][S19][S27].

These interrelated factors combine dynamically challenging management's ability to realize stated objectives within imposed temporal constraints.

SPAC Sector Context: Positioning Within Rising Competition for Targets

ChampionsGate operates amidst intensifying competition where specialized investment vehicles including other blank check companies, private equity funds focused on middle-market transactions, leveraged buyout sponsors pursuing strategic platforms, as well as publicly traded industrial businesses hunting acquisitions jostle aggressively for similarly sized targets [S13].

Corporate differentiation hinges heavily on management stature combined with targeted deal size criteria enabling nimble pursuit of niche sectors underserved by larger consolidators while leveraging unique advantages offered by public listing process expediency—a significant value proposition versus traditional IPO routes demanding longer timelines and higher costs [S3][S13]. Nonetheless heightened competition risks eroding bargain purchase opportunities forcing elevated valuations which may compress future returns potential.

Investor Returns: Analyzing ROE and Cash Flow Implications in Early Stages

Financially ChampionsGate exhibits characteristics expected from blank check companies during early stages prior to consummation of acquisitions: reported ROE approximates negative 74.7% calculated using net income versus equity base reflecting absence of revenue offset coupled with standalone operational expenses incurred during formation period [F1]. Meanwhile cash flow from operations remains neutral or negative given no earnings-backed inflows limiting internally generated liquidity enhancing dependence on sponsor funding sources currently.

Net income figures that appear positive derive mainly from accounting recognition related to interest accrued on trust holdings—not reflective of sustainable profitability nor indicative of ongoing economic performance ultimately contingent upon successful completion of initial business combination deals yielding operational cash generation capacity going forward [F1].

Investors should interpret periodic financial results within this context recognizing early-stage cost absorption inherent in SPAC launch cycles preceding value-creating commercial activity.

Disclaimer: This report is prepared solely for informational purposes based on available regulatory filings and does not constitute investment advice or recommendations regarding any security. The analysis herein does not incorporate speculative assumptions beyond presented data nor anticipates future outcomes beyond stated facts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments