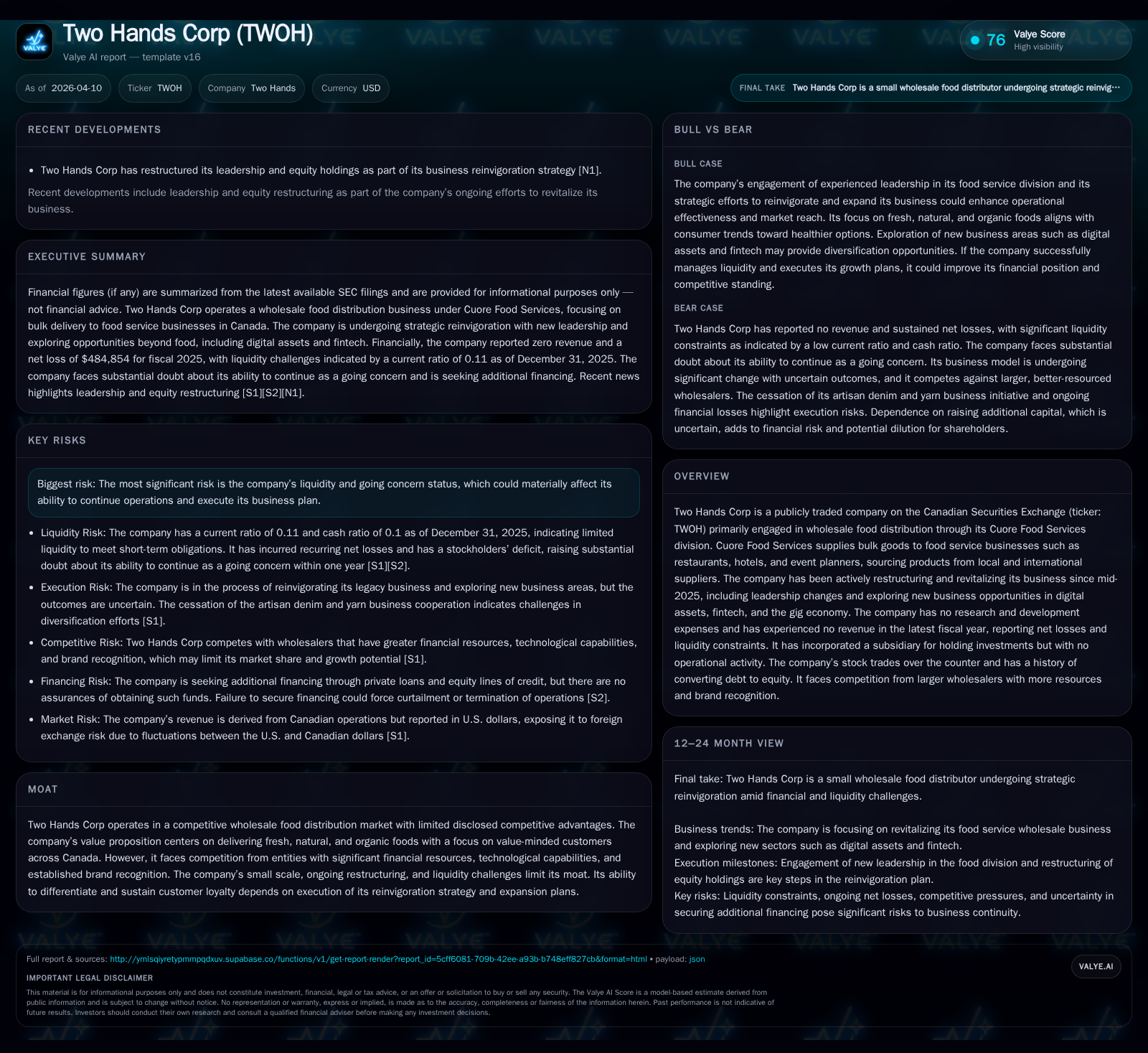

Two Hands Corp’s Revival Journey: From Revenue Collapse to New Horizons

Two Hands Corp faces severe liquidity challenges and zero revenue in 2025 while pursuing a strategic pivot into digital and gig economy sectors.

Two Hands Corp (TWOH) saw a precipitous decline in its core wholesale food business revenue from over $700K in 2024 to zero in 2025, coinciding with sustained net losses and worsening liquidity. The company’s legacy Cuore Food Services division operates in a highly competitive bulk food delivery market primarily serving Canadian value-focused customers but lacks significant scale or moat. Amid these operational and capital constraints, management announced a strategic overhaul in mid-2025 with plans to revitalize existing operations alongside new ventures spanning digital assets, fintech, and the gig economy. The firm’s complex convertible debt structure, sizable derivative liabilities, and ongoing stock dilution risks amplify financial strain. Future performance hinges on securing additional funding and successful diversification, with no formal forecasts provided by management.

Historical Decline and Operational Challenges: The Vanishing Revenue

Two Hands Corp’s fiscal trajectory portrays a striking collapse in its core economic engine during 2025. After generating revenues exceeding $700,000 USD annually across the previous three years — $731K in 2022, $783K in 2023, and $710K in 2024 — the company reported zero revenue for FY2025 according to the latest filings [F1]. This absolute revenue evaporation signifies either full cessation or suspension of the primary wholesale food distribution operations through Cuore Food Services.

Despite this dramatic top-line drop, operating losses narrowed moderately from approximately -$1.17 million USD in 2024 to -$1.06 million USD in 2025 [F1], implying certain cost containment or reduction initiatives amidst structural downsizing. Net losses also improved sharply from -$2.43 million to -$485 thousand USD over this interval [F1]. Yet these gains mask intensifying cash flow pressures as operating cash flows deteriorated further into negative territory — plunging over threefold to nearly -$808 thousand USD last year compared to -$251 thousand USD during 2024 — signposting operational cash burn despite retrenchment measures [F1]. Capital expenditure outlays remained negligible at roughly $10,749 USD historically with no increase documented for 2025.

The anti-dilutive nature of outstanding convertible notes prevented conversion accounting during loss periods but introduces complexity around reported earnings per share and effective dilution risk going forward [S1][S2]. These hybrid securities carry embedded derivatives such as conversion resets that the company must mark-to-market each reporting period, compounding accounting burdens [S3].

The Cuore Food Services Legacy and Its Market Position

Cuore Food Services constitutes TWOH’s foundational wholesale segment supplying bulk goods principally fresh, natural, and organic products to commercial foodservice clients including restaurants, hotels, and event catering businesses across Canada [S13][S18]. Inventory is sourced both from company-owned warehouses and through ad hoc procurement agreements with local and international suppliers ensuring competitive pricing.

This bulk delivery model caters primarily to value-focused customers spanning all demographics and geographies domestically—an important positioning given inflationary pressures heightening demand for cost-conscious procurement among hospitality sector operators [S18]. However, TWOH contends with fierce competition from significantly better-capitalized firms wielding financial heft alongside advanced technology platforms enabling efficiency gains in supply chain logistics and customer engagement [S13][S18]. Two Hands’s relatively small scale restricts its ability to compete on pricing or technology rollout effectively.

Hence while Cuore's product mix aligns well with broad market trends favoring organic/natural foods supplemented by dynamic value deals aimed at driving customer loyalty and brand affinity, the lack of proprietary sourcing advantages or technological moat leave it vulnerable without substantial reinvestment or strategic differentiation [S13][S18].

Liquidity Strains and Capital Structure Complexities

Liquidity challenges permeate TWOH’s financial structure at multiple levels. At December 31, 2025, current assets stood at approximately $254K USD against current liabilities surpassing $2.26 million USD — translating into a precarious current ratio near 0.11 indicative of acute short-term solvency risk [F1]. Cash & equivalents were low at about $228K.

The capital base is heavily leveraged mainly through complex non-redeemable convertible notes alongside related party notes payable bearing interest typically at 8% annually unsecured but due on demand [S3][S8][S16]. Embedded derivatives associated with these convertible instruments—including conversion reset mechanisms and redemption options—are bifurcated for accounting purposes under ASC Paragraphs 815-15-25-1 et seq., requiring periodic fair value assessments that can produce marked-to-market volatility recognized within earnings statements [S3][S27].

Additionally, the company faces obligations including accounts payable near three-quarters of a million dollars plus convertible debt balances exceeding one million dollars total [S19][F1]. This complicated structure exposes shareholders to dilution risks arising from anti-dilutive convertible notes presently excluded from EPS calculations yet potentially convertible upon future profitability or capital events [S1][F1].

Management reports ongoing dialogues with investors concerning private loan facilities along with equity lines of credit but no binding commitments presently exist beyond advances made by the CEO serving as bridge financing for organizational overheads such as legal and accounting fees essential for continued operations [S4][S6][S8].

Management’s Reinvigoration Strategy: A Shift Beyond Food Distribution

In mid-2025 amid deteriorating legacy performance metrics, Two Hands articulated a renewed strategic roadmap aimed at revitalizing its existing wholesale food business while simultaneously exploring new sectoral horizons encompassing digital asset management, fintech solutions, and gig economy service platforms [N1][S1][S2]. This dual approach attempts to leverage core competencies within food distribution while planting exploratory stakes into adjacent high-growth verticals where capital infusion might offer diversified returns.

The establishment of Meridan Capital Management Inc., an incorporated Nevada subsidiary purposed solely for holding investments without active operations so far, exemplifies early-stage structural realignment intended to facilitate external investment initiatives beyond traditional business lines [N1][S1]. Concurrently, earlier textile-related ventures announced in January 2025 concerning artisan denim products faded by mid-year reflecting management's pivot towards higher-potential domains rather than broad diversification without clear focus.

The company underscores intentions "to continue evaluating opportunities both inside and outside the food industry," yet refrains from issuing formal guidance or explicit forecasts on expected returns or timeline milestones highlighting the nascent stage of these plans amid prevailing resource constraints.

Expansion Prospects Within and Outside Core Operations

Absent explicit company-provided projections regarding expansion outcomes across either revamped food services or novel digital-fintech-gig economy businesses, key performance drivers remain speculative but anchored by disclosed operational insights.

Within core food services scope, growth considerations center around geographic expansion throughout Canada coupled with enhancement of product portfolios emphasizing fresh natural/organic lines targeting an evidently wide-ranging value-conscious customer base across socio-economic strata [S13][S18]. Notwithstanding potential consumer appeal benefits derived from dynamic pricing deal offerings designed to foster brand loyalty as cited by management disclosures [S13], TWOH's modest scale relative to entrenched competitors possessing robust logistics networks limits near-term growth velocity absent substantial capital deployment.

In contrast outside legacy operations sectoral entry hurdles include intense competition against digitally native fintech firms leveraging artificial intelligence for financial services automation as well as platform-based gig economy enterprises commanding network effects difficult for traditional brick-and-mortar oriented companies like TWOH to replicate swiftly without significant R&D investment—an area where TWOH reports zero expenditures historically—indicative of an outsourced or acquisitive growth posture rather than organic innovation capacity currently [S1][N1].

Customer retention strategies emphasizing value-driven deals within food distribution might mitigate attrition but face stiff headwinds given competitors’ superior marketing budgets allied with technological sophistication.

Financial Performance Snapshot with Historical Trends

Below is a summarized fiscal snapshot capturing TWOH's financial performance metrics over recent years highlighting trends:

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 0 | 0 | -807887 | -1 | -100.0% | +80.1% |

| 2024 | 709526 | -2 | -250503 | -1 | -9.4% | +70.2% |

| 2023 | 783489 | -8 | -451932 | -1 | +7.1% | +62.4% |

| 2022 | 731302 | -22 | -840745 | -18 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | 24.9 | |

| 2024 | 68.2 | |

| 2023 | -462681 | 291.8 |

| 2022 | -851494 | 467.7 |

Source: SEC companyfacts cache [F1].

Note: Derived year-over-year percentages denote trajectory between consecutive fiscal years; capex stable around ~$10K until latest disclosure lacking new data; net income improvements reflect diminishing absolute loss magnitude though not profitability. Current ratio at end-2025 stands alarmingly low near 0.11 indicating severe liquidity stress given working capital deficiency observed through negative equity trends worsening since FY2019.

Capital Allocation and Return Metrics

Amid ongoing negative free cash flow conditions highlighted by operating cash flow of approximately -$808K USD offset partially by minimal capex spending historically (~$10K), Two Hands has not declared dividends nor engaged in share repurchases consistent with preservation strategy under financial distress [F1]. Compensation strategies include stock-based awards potentially diluting shareholders over time as part of expense management efforts described in filings [S1][S2].

An approximate return on equity calculated using FY2025 net income (-$485K) divided by negative equity (-$1.95M) yields about +25%, though this figure must be interpreted cautiously due to the adverse balance sheet context including accumulated deficit exceeding $95 million impairing conventional profitability assessments.

Convertible notes accompanied by embedded derivatives introduce further complexity around shareholder dilution potential depending on future conversion events or refinancing outcomes impacting per-share economics disproportionately absent significant operational recovery or capital appreciation catalysts.

Milestones Ahead: Key Events and Watchpoints for TWOH

Looking forward the primary concerns coalesce around securing vital financing resources sufficient to avoid curtailment of operations given forecasted annual cash necessities approximating $300K primarily toward general administration alongside legal/accounting requisite functions during implementation phases of new business initiatives slated over next twelve months indicated by management commentary [S3][N1].

Investors should monitor closely progress surrounding:

- Success of ongoing discussions aiming at private loans/equity credit lines providing liquidity buffer;

- Executions on announced diversification plans outside traditional food distribution including active deployments within digital asset / fintech / gig platforms;

- Any substantive updates on operational status regarding Cuore Food Services revival efforts;

- Potential shifts in convertible debt positions impacting capital structure stability. Failure to realize viable financing could trigger existential threats compromising continued corporate viability despite strategic aspirations delineated publicly.

This analysis synthesizes documented facts strictly from official SEC filings contemporaneous as of April 10th 2026 alongside trusted news sources without conjecturing speculative outcomes beyond stated disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments