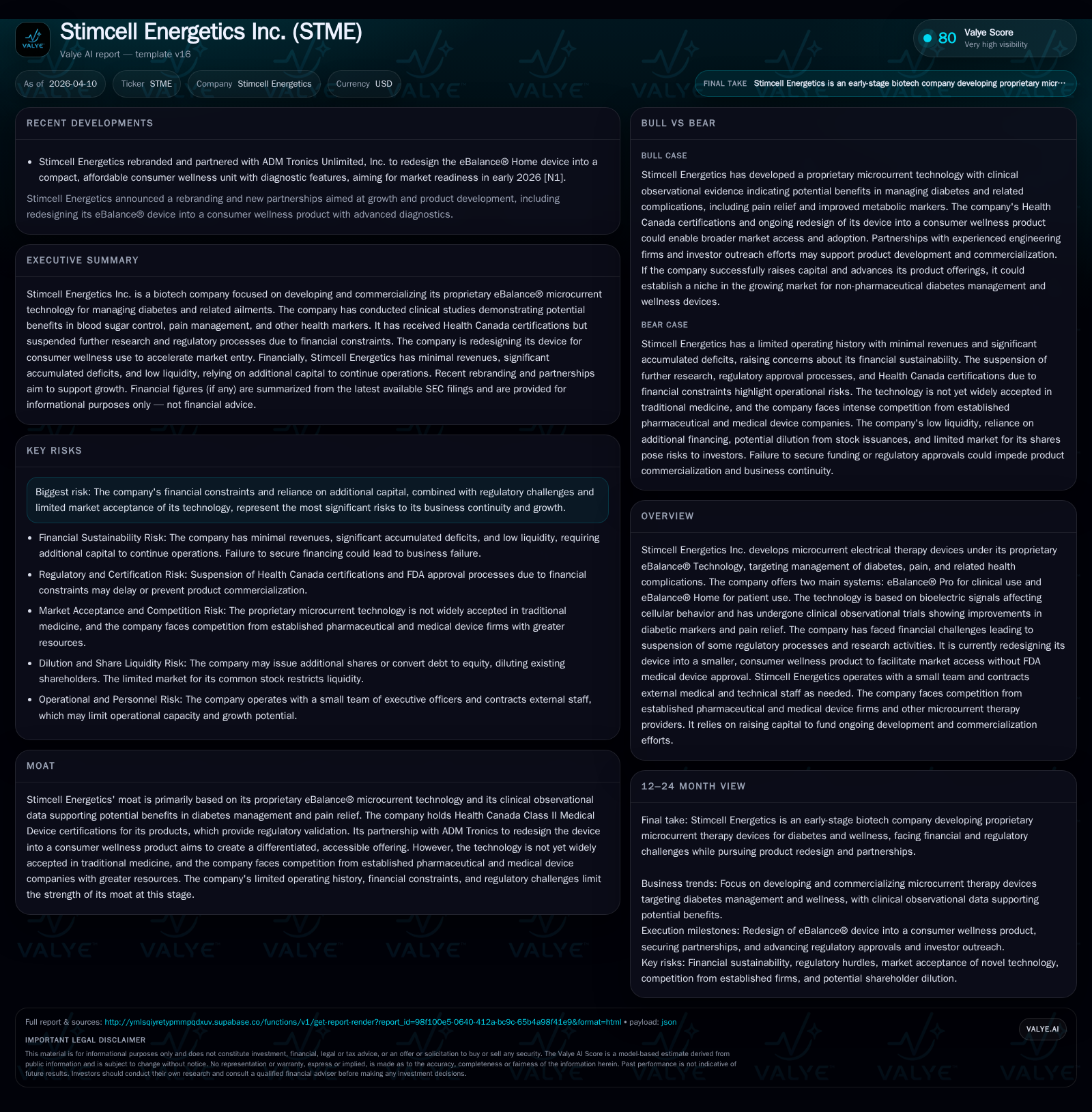

Stimcell Energetics Recasts Its Growth Blueprint with eBalance® Innovation and Market Reset

Stimcell Energetics shifts from clinical microcurrent therapies toward consumer wellness devices amid financial strain and regulatory hurdles.

Stimcell Energetics has historically pursued growth through its proprietary eBalance® microcurrent electrical therapy technology targeting diabetes and pain management. However, continuous financial losses, zero revenues by FY2024, and regulatory setbacks including suspension of Health Canada licenses have stalled commercialization. Responding to these challenges, the company is redesigning its device into a smaller consumer wellness product to ease market entry without FDA medical device approval. This pivot reflects an attempt to unlock growth by circumventing regulatory bottlenecks and capitalizing on wellness trends but faces competition from entrenched medical device makers and requires fresh capital to sustain operations.

From Microcurrent Innovation to Market Challenges: A Historical View

Stimcell Energetics Inc. has pursued a growth path centered on its proprietary eBalance® Technology, an innovative application of microcurrent electrical therapy (MEY) aimed at modulating bioelectric signals to influence cellular behavior for health benefits. The company’s early years saw incremental development efforts culminating in the launch of two product systems: the eBalance® Pro for clinical practitioners and eBalance® Home designed for patient self-use.

Despite this innovation focus, Stimcell's revenue trajectory paints a stark picture of commercial struggles. Revenues peaked modestly at about $95.8k USD in FY2020 before plunging to zero by FY2024 [F1]. This collapse coincides with regulatory license cancellations that effectively suspended the company's selling activities in key markets [S18]. Concurrently, the company endured persistent net losses ranging from approximately $906k in FY2019 to around $697k in FY2022 [F1], indicating ongoing challenges transforming R&D investments into profitable sales.

Operating cash flows mirror this downward momentum with negative CFO stretching from nearly -$451k USD in FY2022 to roughly -$146k USD most recently [F1]. Capital expenditures have largely tapered off since FY2020, underscoring constrained investment capacity [F1]. Moreover, the company undertook a notable reverse stock split (1-for-15) alongside rebranding in late 2024 as part of financial stabilization efforts [S1]. These milestones symbolize attempts to recalibrate market perception amid operational headwinds.

Historical performance (annual)

| FY | CFO ($) |

|---|---|

| 2025 | -141600 |

| 2024 | -145898 |

| 2023 | -272209 |

| 2022 | -450591 |

Source: SEC companyfacts cache [F1].

*Data not explicitly available for revenue or net income for these years [F1]

Negative figures reflect ongoing loss-making operations; revenue ceased post-2023 due to regulatory license loss [F1]

Clinical Evidence and Regulatory Barriers Impacting Growth Trajectory

The eBalance® Technology leverages MEY delivering low-intensity electrical currents below sensory thresholds aimed at epigenetic modulation—a process influencing gene expression without altering DNA sequences—to improve cellular function related to diabetes complications and pain relief [S1]. This mechanism positions Stimcell’s devices uniquely within therapeutic microcurrent modalities but also outside conventional pharmaceutical paradigms.

Clinical observational trials conducted by the company indicated improvements in diabetic biomarkers and symptomatic pain relief; however, these findings have yet to gain broad clinical adoption or rigorous validation seen with standard randomized controlled trials [S1]. Furthermore, Stimcell's products received Health Canada Class II Medical Device Certifications—an important regulatory achievement—allowing initial market entry [S18]. Yet financial constraints compelled cancellation of mandatory annual audits leading to loss of these certifications between 2022-23 [S18].

Attempts at FDA genome-wide 510(k) clearance stalled as well due to cost and resource limitations; the company formally withdrew its applications [S18], highlighting the classic barrier faced by med-tech startups lacking deep-pocketed support.

This multifaceted regulatory environment dramatically restricts revenue-generating opportunities. Adherence demands extensive quality management systems compliance (ISO 13485:2016 standard), manufacturing rigor, labeling controls and post-market surveillance—each incurring substantial cost and expertise requirements rarely feasible for small teams contracting external specialists as Stimcell does [S24], [S27].

Pivot Strategy: Redesigning eBalance® for Consumer Wellness Market

Recognizing these bottlenecks, in February 2025 Stimcell entered a strategic partnership with ADM Tronics Unlimited Inc., a leader in electronic medical device engineering, to develop an optimized consumer wellness variant of its technology [S18]. The new eBalance® Wellness microcurrent device aims to be smaller, more affordable and designed explicitly for general wellness claims rather than medical treatment indications [N1], [S3].

This pivot intends to bypass onerous FDA medical device regulations by marketing under wellness product guidelines which carry fewer entry barriers. Such a shift could accelerate time-to-market and reduce costs substantially.

Notably, the redesigned unit is planned for completion by fall 2025 with an early 2026 launch target projected [N1]. This direct-to-consumer approach contrasts prior emphasis on clinical professional systems reflecting broader sector trends where wearables and home-use devices command growing attention.

However, this transition is not without risk: regulatory circumvention may limit reimbursement potentials; consumer skepticism around efficacy must be addressed through education; technological downsizing could impair performance clarity; and competition within crowded wellness electronics could compress pricing power.

Financial Overview: Cash Flow Challenges and Capital Allocation Dynamics

Stimcell’s financial profile underscores acute liquidity shortages threatening operational sustainability. The latest current ratio approximates a perilous 0.02 indicating near-total erosion of working capital relative to liabilities [F1]. Negative operating cash flows persist unabated—recently at approximately -$142k annually—exacerbated by zero revenues since FY2024 post-license cancellations [F1], [S9]. Capital expenditures remain minimal or nonexistent since FY2022 emphasizing tight control over outlays amid constrained resources [F1].

The company has not paid nor anticipates paying dividends on common stock given its focus on funding business development activities rather than shareholder returns [S11], [S12], [S19]. No share repurchase programs exist. Equity dilution through debt conversion into common shares has been employed as a measure to reduce liabilities but adds shareholder dilution risk [S15], [S26].

Capital discipline centers largely on surviving until successful delivery of the new consumer-ready unit combined with securing additional financing. The recent engagement of Stonegate Capital Partners for research coverage and institutional investor outreach might facilitate improved capital access through enhanced market visibility and credibility [S3].

Absent fresh equity or debt injections aligned with business milestones there is material risk that Stimcell’s ability to restart clinical trials or pursue broader commercialization will be compromised severely.

Competition Spotlight: Incumbents in Diabetes Management and Pain Relief

Stimcell operates within fiercely contested domains targeting diabetes management complications and chronic pain relief arenas dominated by global pharma-medical companies. Competitors named include Bayer Corp., Becton Dickinson Corp., LifeScan (a J&J division), MediSense Inc., TheraSense Inc., among others known for traditional pharmacological treatments or glucose monitoring technologies well integrated into healthcare workflows [S1], [S4].

Within the microcurrent therapy niche itself exist competitors like BodiHealth Systems focusing on US pain markets or Electromedical Products International which markets Alpha-Stim® PPM devices addressing similar symptoms via proprietary waveform technologies.

Entrenched practitioner trust built on extensive clinical evidence bases coupled with reimbursement coverage mechanisms create substantial barriers for newer entrants like Stimcell relying on emerging modalities without widespread acceptance or intellectual property exclusivity—the company's eBalance® Technology is unpatented—as noted in filings [S16], [S18], [S22]. Marketing penetration strategies adopted by big players leverage scale advantages allowing aggressive pricing tactics whereas small firms face uphill battles securing meaningful market share especially when technical efficacy debates persist.

What’s on the Horizon? Key Milestones and Strategic Watchpoints

Explicit company forecasts are elusive given current financial constraints yet several pivotal developments merit monitoring as markers for trajectory shifts:

- Completion timeline of the redesigned eBalance® Wellness consumer device targeted Fall 2025 enabling early commercial launches expected in early 2026 per corporate communications [N1], [S3]

- Progress on any regulatory filings under wellness product classifications versus medical device routes shaping speed-to-market potential [S18]

- Updates regarding reactivation or resubmission plans for FDA/Health Canada licenses if capital conditions improve [S28]

- Outcomes from new clinical studies or observational data collection post pivot validating claims applicable for wellness consumers versus traditional therapies

- Institutional investor feedback cycles tied to Stonegate advisory agreement evaluating outlook revisions during their quarterly research reports prepared commencing March 2026 deployment period [S3]

- Financial restructuring events including further equity issuances or debt conversions anticipated per prior disclosures aiming at shoring up liquidity citing strategic necessity under present operating deficits[S15], [S26]

These factors serve as "red flags" or catalysts depending on execution success underpinning potential business model transition validation over next quarters.

Investment Considerations Amid High-Risk Emerging Technology Dynamics

Stimcell presents a classic profile typifying speculative biotech-med tech ventures where innovative IP-driven platforms confront realities of limited operating history intertwined with resource scarcity. Its reliance on unpatented microcurrent electrical therapy places an emphasis on clinical data narrative acceptance yet this remains marginal within orthodox medical frameworks at present.

Financial fragility is paramount amongst risks—with deeply negative cash flows demanding continuous financing rounds dilutive to shareholders alongside restricted trading liquidity in penny stock markets impacting exit possibilities[S7], [F1]. Competition pressure from dominant incumbents underscores commercialization barriers further complicated by absent payer reimbursement guarantees prevalent across emerging med tech disruptors.

Counterbalancing these risks are opportunity vectors deriving from rising consumer interest in non-pharmaceutical wellness solutions combined with regulatory environment openings favorable toward declassified wellness devices enabling faster innovation cycles. If successfully executed product redesign attains credible efficacy demonstrated via transparent evidence accumulation this could enable differentiated positioning within a growing segment accelerating adoption curves.

A risk-reward paradigm suggests only investors capable of enduring prospective total loss but seeking asymmetric returns could contemplate speculative exposure framed within informed due diligence emphasizing finance strategy resilience benchmarks going forward.

This analysis synthesizes information exclusively from public filings and credible news sources as indexed above. It does not constitute investment advice but intends technical insight suitable for buy-side research contexts. Readers should undertake independent evaluation consistent with their specific informational needs.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments