CXJ Group's Financial Struggles Amid Expansion in China’s Automotive Aftermarket

CXJ Group pursues aggressive franchise network growth in China’s auto aftermarket while grappling with financial losses and regulatory complexities.

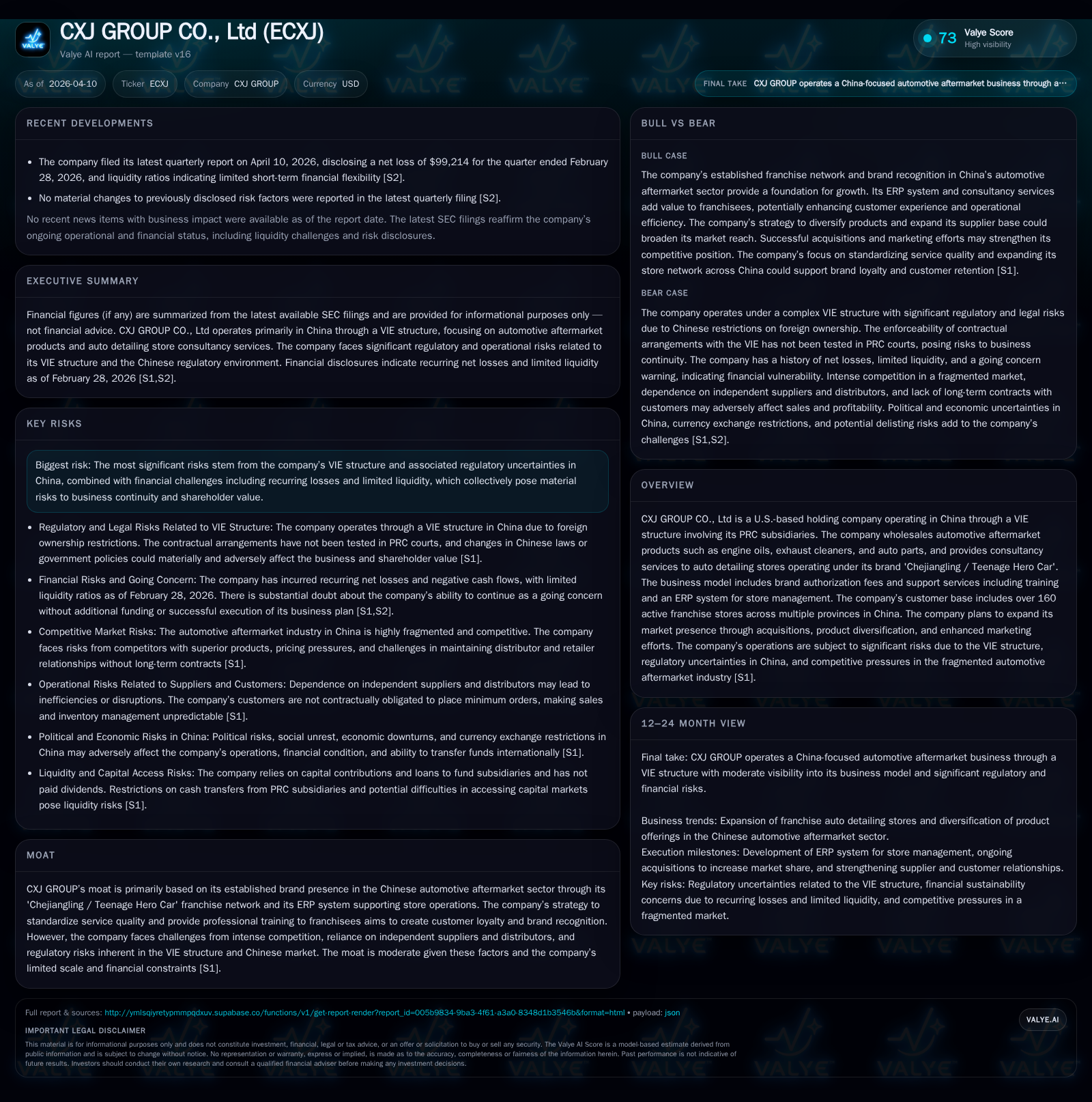

CXJ Group Co., Ltd operates a franchise-based automotive aftermarket business in China through a VIE structure. Despite expanding its 'Chejiangling / Teenage Hero Car' franchise to over 160 stores and planning significant future growth, the company has sustained deepening operating losses and cash flow deficits through fiscal 2025. CXJ’s reliance on independent suppliers and an untested VIE contractual framework exposes it to significant operational and regulatory risks. Capital allocation remains constrained with minimal asset investment, negative equity, and limited liquidity, raising questions about funding its ambitious expansion plans without material financial restructuring.

CXJ Group’s Business Model and Franchise Expansion Strategy

CXJ Group Co., Ltd (ECXJ) functions as a U.S.-based holding company conducting its core business operations in China via a variable interest entity (VIE) structure. This arrangement allows the company indirect exposure to the Chinese automotive aftermarket—a sector restricted from foreign ownership—through contractual control rather than direct equity ownership of its PRC subsidiaries [S1],[S6].

The company's principal business involves wholesaling automotive aftermarket products such as engine oils (notably its NOVATE synthetic motor oil), exhaust cleaners like Ksoncar, and various auto parts across multiple provinces in China. Crucially, CXJ operates an extensive franchise network branded as “Chejiangling / Teenage Hero Car” targeting localized auto detailing stores. These franchised stores are situated strategically within three kilometers or about ten minutes’ drive from residential areas to capture convenient neighborhood auto service demand [S4].

Beyond product sales, CXJ provides consultancy services which include professional training programs for store personnel, standardized operational guidelines covering store décor and service procedures, and technical support systems—most prominently an enterprise resource planning (ERP) platform enabling integrated management of inventory and daily operations accessible via both PC and mobile devices. The ERP system is central to driving operational efficiencies across the franchise network and fostering brand consistency [S4],[S11].

As of May 31, 2025, the company reported more than 160 active franchise stores spanning 23 provinces and 132 cities across China—a footprint reflecting concerted efforts at gradual network scaling. Company management has articulated ambitions to expand this network by approximately 1,000 additional franchises over the next five years through organic growth supplemented by acquisitions aimed at enlarging market presence and diversifying product offerings [S4]. Their strategy emphasizes leveraging economies of scale afforded by a broadened operations platform alongside incremental revenue streams from brand authorization fees.

Historical Financial Performance: Growing Losses despite Network Growth

Despite operational expansion and network scaling efforts, CXJ Group's financial results over recent fiscal years reveal deepening profitability challenges. A summary of key financial metrics from FY2022 through FY2025 illustrates this trend starkly [F1]:

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -2 | -418525 | -2 | 2934 | -6.9% |

| 2024 | -2 | -590038 | -2 | 2934 | -87.6% |

| 2023 | -1 | -378815 | -1 | 4429 | -110.2% |

| 2022 | -1 | 443523 | 0 | 1914 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | -421459 | 146.9 |

| 2024 | -592972 | -585.8 |

| 2023 | -383244 | -47.2 |

| 2022 | 441609 | -28.4 |

Source: SEC companyfacts cache [F1].

Over the four-year span ending FY2025 ([F1]), operating income losses worsened from $498k to about $2.25 million—more than quadrupling in magnitude despite expansions in their franchise footprint. Net income mirrored this deterioration reflecting persistent negative earnings. Operating cash flow turned negative starting FY2023 after a positive inflow in FY2022; although modestly improved in FY2025 compared to FY2024 (-$418k vs -$590k), it remains deeply suboptimal given the scale of ongoing losses.

Capex figures remained low throughout these years consistent with an asset-light model focused on franchising rather than capital-intensive physical infrastructure investments.

This widening loss profile amid growing store count suggests significant cost absorption related to expansion activities coupled with ongoing competitive pressures reducing margins or delaying profitability breakeven points.

Critical Dependencies: Supply Chain and Distributor Relationships

CXJ sources almost all its automotive aftermarket products through approximately eight independent suppliers who themselves engage contract manufacturers mainly located domestically or internationally as per respective SKUs [S3]. The company does not own manufacturing plants or packaging equipment but relies fully on these external partners for product availability.

This dependence introduces contract manufacturers risk — any termination or interruption of supply agreements could disrupt product deliveries critical to both wholesale customers and franchised retail outlets. Additionally, given distributors also handle competitors' products simultaneously [S7], distributors’ preferences can sway towards competitors', eroding CXJ's sales volumes.

The fragmented supplier landscape adds vulnerability to supply chain bottlenecks especially amid geopolitical tensions or logistic disruptions common in the global automotive aftermarket industry chain.

Effective management of these supplier relationships is vital for sustaining inventory levels aligning with demand fluctuations generated by their franchise network scaling.

The Regulatory Quagmire: VIE Structure and China’s Political-Risk Backdrop

Operating via a VIE contractual arrangement entails pronounced regulatory uncertainty under PRC law where foreign ownership restrictions bar direct foreign equity participation in value-added telecommunications-like sectors encompassing CXJ’s activities [S1],[S5],[S6].

These contracts confer economic benefits without formal legal ownership of the VIE subsidiaries by CXJ's U.S.-listed holding company structure—unproven within PRC judiciary frameworks regarding enforceability especially under shifting policy climates.

Heightened scrutiny on U.S.-listed Chinese firms raises additional risk around potential PCAOB audit limitations possibly culminating in delisting scenarios that would materially impact shareholder value [S1].

Moreover, regulatory changes may impose sudden constraints on cross-border fund transfers limiting dividend repatriation or intra-group financing critical for sustaining domestic operations [S12].

Such contractual exposure complicates external financing accessibility while increasing compliance costs and investor apprehension about governance risk.

Future Growth Prospects: Store Expansion, Product Diversification, and Strategic Acquisitions

Management anticipates robust franchise network growth aiming for an incremental ~1,000 stores over five years broadening into new geographic markets beyond current focus provinces including Henan and Shandong [S4]. Product portfolio diversification intends to enrich customer offering encompassing additional aftermarket consumables beyond existing engine oils and exhaust cleaners [S16].

Acquisition targets will be evaluated based on cost efficiency potential alongside revenue contribution synergies including existing customer bases and supplier networks enhancing competitive positioning [S16].

However absent explicit forward guidance or detailed milestones regarding timelines or profitability outlooks for such expansions requires cautious interpretation ([N#] news absent).

Execution risks linked to financing adequacy amid ongoing financial losses alongside regulatory uncertainties could critically hamper these ambitions limiting operational leverage gains derived from scaled ERP system deployment.

Capital Allocation, Liquidity Crunch, and Returns on Equity

CXJ's financial statements paint a picture of constrained capital dynamics marked by:

- Minimal capex investment ($2.9k annually approx.) consistent with a franchising service model relying mainly on third-party owned assets rather than fixed capital accumulation.

- Cash balances at quarter-end February 28, 2026 stood at roughly $145k with current assets totaling ~$414k against very high current liabilities near $2.28 million yielding an acute current ratio of just about 0.18—indicative of severe short-term liquidity stress [F1],[S17].

- Shareholder equity turned sharply negative at approximately -$1.55 million by FY2025 driven by accumulated deficits surpassing paid-in capital stock values reflecting multi-year operating losses steadily eroding net asset base.

- ROE calculation using net loss over negative equity yields a mathematically high but economically non-standard figure around +146%, which here underscores loss absorption exceeding equity dilutions rather than true value generation [F1].

- No dividends nor stock buybacks have occurred post combination; earnings retention is aimed at supporting ongoing operations but with limited cash flow generation capability so far [F1],[S27].

Altogether these data suggest operating cash burn outpacing available liquidity requiring external capital injections or restructuring initiatives for sustainable scaling—no evidence yet that such measures are underway.

Risks to Watch: Liquidity, Regulatory Compliance, and Market Competition

Key risk factors identified include:

- Ongoing liquidity constraints threaten operational continuity if new capital is unavailable fulfilling obligations amidst expanding overhead tied to franchise rollout [F1],[S17].

- VIE contractual uncertainties pose material legal enforcement challenges potentially exacerbated by fast-evolving PRC regulatory policies constraining foreign-held entities or triggering delisting risks from unsatisfactory auditing access commitments under U.S. law enforcement standards [S1,S5,S6,S23].

- Supply dependence on independent contract manufacturers leaves CXJ vulnerable to distribution disruptions or margin pressure if suppliers prioritize competitors or encounter logistic issues exacerbated under geopolitical tensions impacting cross-border trade flows [S3,S7].

- Intense fragmentation within the Chinese automotive aftermarket imposes fierce competition both from established domestic players with larger scale advantages and evolving foreign entrants demanding continuous product innovation plus competitive pricing tactics undermining CXJ's market share gains [S20,S8].

- Lack of comprehensive insurance coverage for liabilities beyond basic property/accident risks exposes possible uninsured losses impacting results unexpectedly particularly given the relatively modest size and resource limitations facing CXJ's corporate structure [S5].

- Enforcement difficulty over U.S.-based judgments against PRC-domiciled affiliates further complicates investor protection measures amid jurisdictional complexity [S19].

Overall investors need closely monitor policy developments affecting VIE’s permissibility status along with management's success executing store growth within tight financial parameters amidst escalating operating expenses paired against limited balance sheet flexibility.

This report provides a fact-based evaluation grounded exclusively in filed SEC disclosures up to April 10th, 2026 ([F1],[S#]) without speculative assumptions beyond stated company plans or numerical data observed therein. It intends solely for informational use devoid of any investment advice or trading recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments