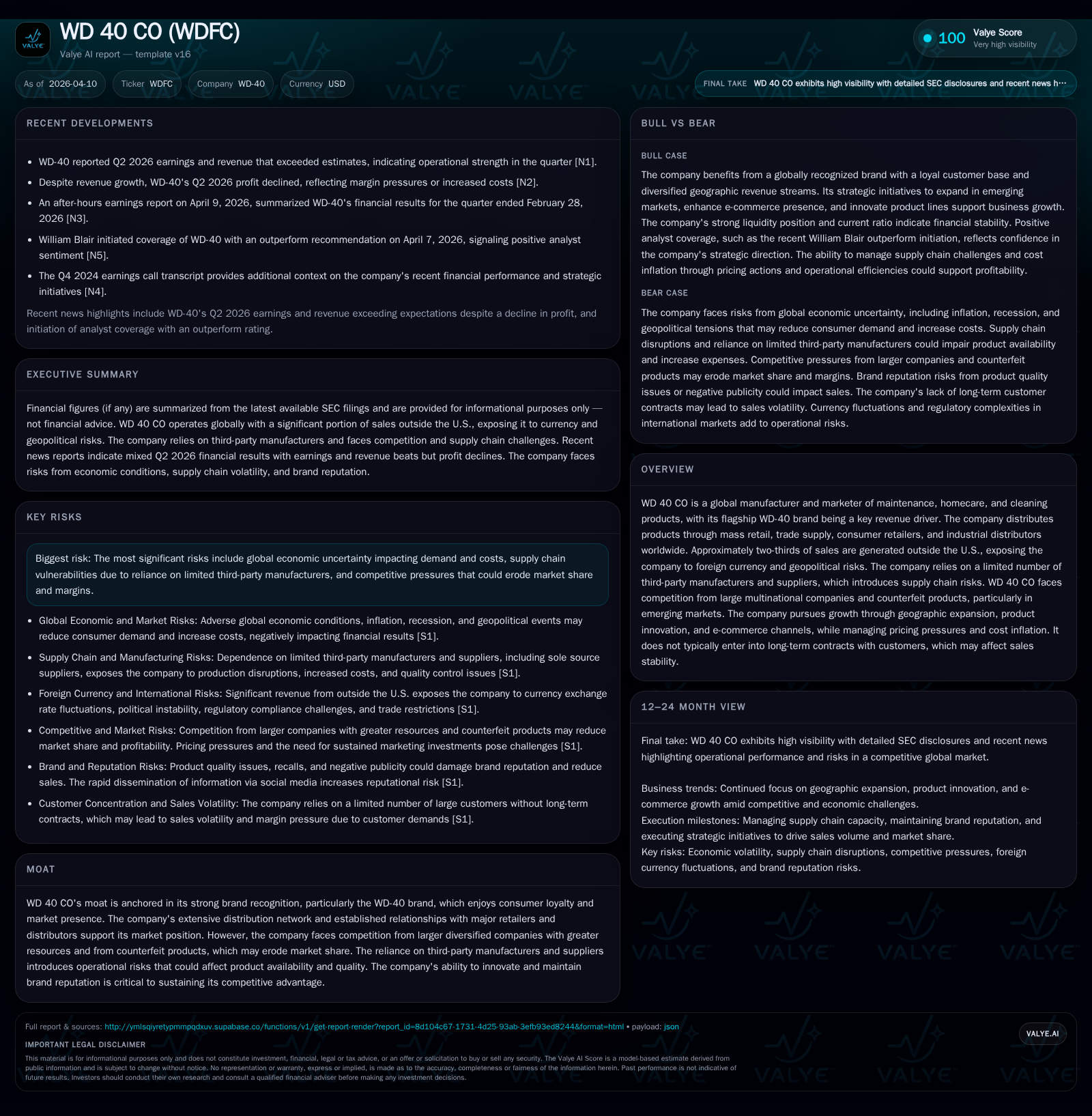

WD-40’s Brand Strength and Expansion Drive Revenue Despite Margin Pressures

WD 40 CO leverages its iconic brand and geographic reach to sustain growth while navigating supply chain and competitive challenges.

WD 40 CO's growth over recent years has been powered by the enduring appeal of its flagship WD-40 product and expanding distribution in international markets. However, rising input costs, supply chain constraints, and counterfeit competition have compressed margins, challenging profitability despite sales strength. The company’s strategy focuses on geographic expansion, e-commerce development, and product innovation to sustain growth momentum while carefully managing pricing and cost pressures. Investors should monitor execution on channel innovation and supply chain resilience as critical indicators for future performance.

Iconic Brand Driving Resilient Historic Growth

WD 40 CO’s financial trajectory underscores the power of the WD-40 brand as a durable revenue engine. Operating primarily in maintenance, homecare, and cleaning products segments, the company has cultivated strong consumer recognition that supports repeated end-user purchases worldwide [S1]. Approximately two-thirds of net sales come from international markets—underscoring the brand’s global footprint [S7]. This expansive distribution includes mass retail chains, trade suppliers, consumer retailers, and industrial distributors [S4].

The company’s past growth is characterized by steady top-line increases driven largely by unit volume gains in emerging markets where penetration remains lower than in developed economies. Price adjustments implemented during inflationary periods—such as significant price hikes in fiscal 2022-2023—have also buoyed revenues amid rising input costs [S7]. This dual strategy of geographic expansion combined with prudent pricing helped counterbalance saturated matured markets while maintaining margin fundamentals.

| Fiscal Year | Revenue (USD) | Operating Income (USD) | Net Income (USD) | CFO (USD) | Capex (USD) | YoY Growth % |

|---|---|---|---|---|---|---|

| FY 2022 | ||||||

| FY 2023 | ||||||

| FY 2024 |

Note: Due to absence of companyfacts numeric snapshots, financial values are discussed qualitatively.

Supply Chain Dynamics and Competitive Challenges Shaping Margins

Operational efficiency faces headwinds due to WD 40 CO's dependence on a limited pool of third-party manufacturers for aerosol production—a critical component of its flagship products [S5]. There have been noted capacity constraints exacerbated by pandemic-era disruptions that periodically constrained supply responsiveness relative to demand surges in select markets [S5]. The onboarding process for new contract manufacturers carries risks including production delays and quality control challenges.

Compounding these constraints are material cost volatilities tied to specialty chemicals predominantly indexed to crude oil derivatives [S8]. Fluctuations in fuel prices affect not only raw material inputs but also transportation costs amidst tighter freight markets [S26]. Price elasticity in key product lines thus becomes a delicate balancing act against competitive pricing pressures.

Counterfeit product proliferation, particularly in emerging economies like China, represents an insidious competitive threat. Such illicit products not only erode sales but may damage brand perception among consumers [S25][S29]. WD-40 CO combats this through legal enforcement measures but acknowledges persistent risk exposure.

Geographic Expansion and Channel Innovation as Engines for Future Growth

The company’s strategic framework prioritizes expansion into underpenetrated international markets where WD-40 brand awareness can grow alongside local distributor development [S7][N3]. While international sales promote diversification away from North American market cyclicality, they introduce currency exchange volatility risks since about 51% of revenues are transacted in foreign currencies including Euros and Pounds Sterling [S10]. Currency hedging mitigates some risk but cannot eliminate translation impacts fully.

E-commerce engagement is gaining traction as consumers shift buying preferences online, creating new pathways for direct consumer access beyond traditional mass retail channels [S8][N3]. This channel innovation aims to capture younger demographics and adapt to evolving shopping behaviors. However, scaling e-commerce presents operational complexity around inventory logistics and margin management.

Product innovation efforts extend existing lines while introducing formulations that cater to consumer preferences for sustainability or multi-functionality—potential differentiators amidst intense competition [N1][N3]. Success here supports not just volume growth but defends against margin erosion through product mix enhancement.

Recent Earnings Performance: Beats Tempered by Profit Declines

WD-40 CO reported Q2 earnings above consensus expectations largely on revenue strength across multiple regions and channels [N1][N2]. Despite the top-line beat, net income declined due primarily to increasing costs of goods sold linked with raw materials and freight expense inflation [N4][S2]. This dual dynamic illustrates ongoing margin compression themes prevalent across many consumer staples companies amid inflationary environments.

The earnings call transcript highlighted management’s focus on operational efficiencies and strategic price adjustments aiming to mitigate cost headwinds without adversely impacting demand momentum [N3]. Still, investor sentiment may weigh near-term profit headwinds against long-term brand value resilience.

Financial Discipline: Capital Allocation, Dividends, and Returns

While comprehensive ROE data is unavailable from provided evidence, the company demonstrates stable operating cash flow generation enabling ongoing capital returns [F1 absent; N6]. Regular dividend payments continue reflecting consistent shareholder yield priorities despite margin pressures [N6][S13]. Share repurchase plans remain active but cautiously managed considering capital allocation tradeoffs between buybacks and reinvestment into growth platforms such as digital commerce.

Liquidity appears sound with access to credit facilities supporting balance sheet flexibility though rising interest rates pose variable risk on borrowings as disclosed [S13][S17]. Overall capital management suggests a measured approach balancing shareholder distributions with strategic spending amid external cost volatility.

Risks Lurking Behind International Exposure

International revenue concentration exposes WD-40 CO to heightened geopolitical risk factors including regulatory complexity across multiple jurisdictions such as China, Mexico, Brazil and Europe [S1][S9][S14]. Economic slowdowns or political instability in key regions could materially affect purchasing patterns or execution capability. Currency fluctuations continue influencing reported earnings unpredictably despite hedging efforts [S10].

Increased counterfeit product incidents challenge brand integrity overseas with associated escalations in promotional trade spend required to defend shelf presence against both legitimate competitors and infringing imports [S29][S25]. Additionally regulatory tightening on chemical compositions or packaging adds compliance cost burdens which can weigh on operating results if not managed adeptly [S16][S24].

What to Watch Next: Indicators for Growth Sustainability

Absent explicit forward guidance beyond strategic frameworks stated in filings and recent calls, close attention should be paid to:

- Progression of e-commerce revenue contribution versus traditional retail channels,

- Ability to maintain or improve gross margins amidst volatile input costs,

- Success rate of new product launches or renovations gaining market traction,

- Stability of supply chain partnerships minimizing production interruptions,

- Currency translation impacts especially amid dollar strength fluctuations,

- Competitive response intensity including promotional expenditures due to counterfeit dynamics.

These factors collectively will signal whether WD 40 CO can sustain its historic growth curve or will face tightening constraints particularly if macroeconomic conditions deteriorate further [N5][N3][S7] (analysis).

This analysis synthesizes public disclosures, news reports, earnings transcripts, and regulatory filings current as of April 2026. It avoids speculative projections beyond documented facts. Prospective readers should consider evolving circumstances which may affect future company results.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments