Banco BBVA Argentina’s Financial Resurgence and Strategic Outlook Amid Inflationary Pressures

Strong earnings growth and disciplined capital management underpin BBVA Argentina’s resilience amid volatile macroeconomic conditions.

Banco BBVA Argentina has achieved a remarkable surge in net income from ARS 9.4 billion in 2021 to ARS 364.8 billion in 2024, supporting a robust return on equity of approximately 13.9%. This financial resurgence is backed by solid capital adequacy with a total capital ratio of 17.5% at the end of 2025 and prudent liquidity risk management frameworks. The bank’s ongoing digital transformation and customer-centric initiatives have enhanced deposit and lending growth, despite tightening regulatory dividend restrictions and rising credit risks from inflationary pressures. Going forward, managing interest rate repricing gaps, credit quality deterioration especially in retail loans, and Central Bank controls on dividends will be critical to sustaining growth and returns.

Accelerating Earnings on the Back of Expanding Equity Base

Banco BBVA Argentina has demonstrated extraordinary profitability growth in recent years against a challenging inflationary backdrop. Net income surged from ARS 9.36 billion in FY2021 to ARS 364.8 billion by FY2024, representing an extraordinary compound acceleration and culminating in a year-over-year increase of approximately 132% from FY2023 to FY2024 [F1]. This explosive earnings expansion was supported by strategic credit growth coupled with margin management as inferred from disclosures related to repricing risk [S1]. Concurrently, shareholders' equity ballooned from ARS 163 billion in FY2021 up to approximately ARS 2.62 trillion in FY2024 [F1]. Such comprehensive growth yielded an approximate return on equity (ROE) of about 13.9% for FY2024, underscoring strong profitability relative to capital employed.

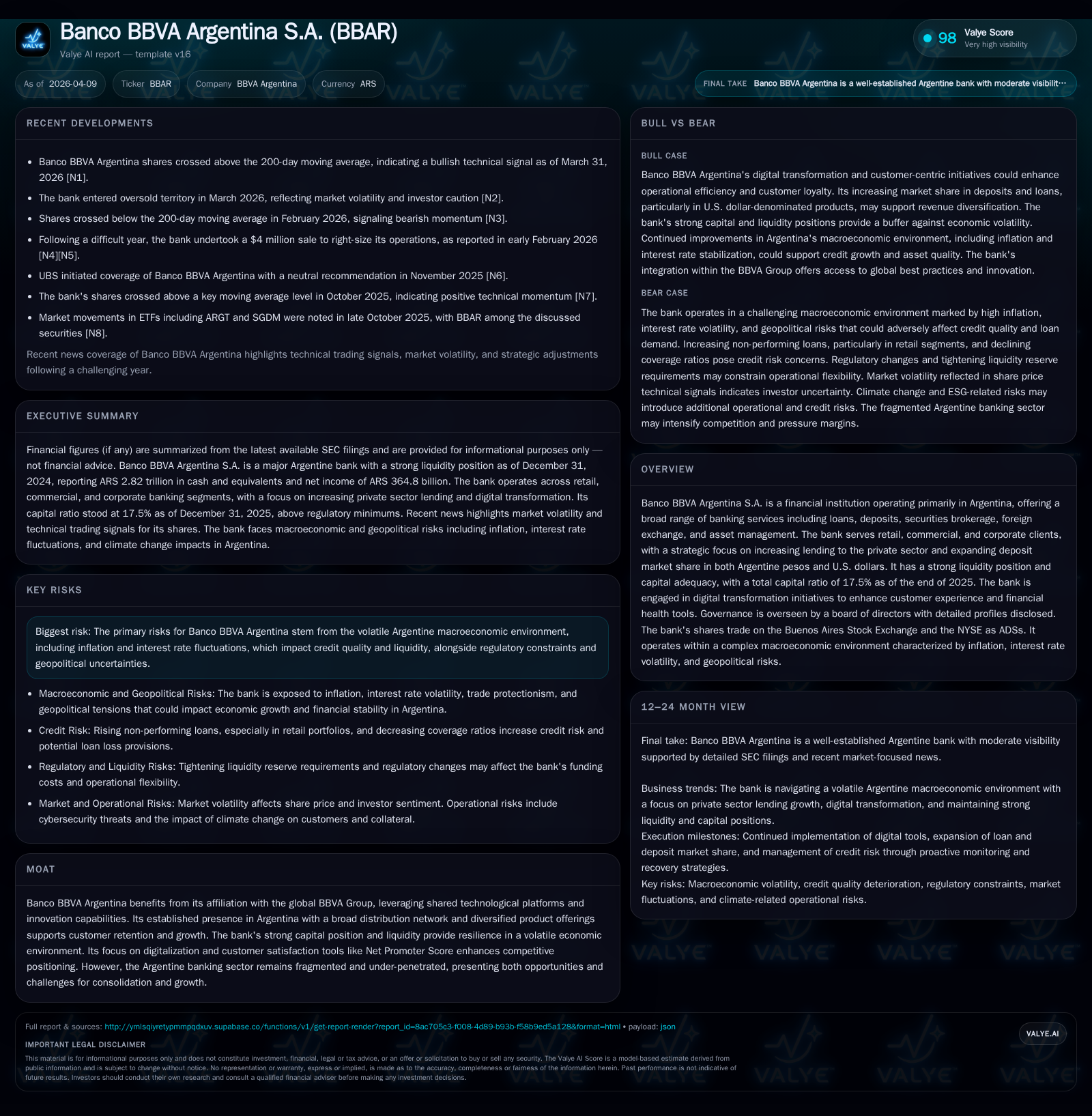

Historical performance (annual)

| FY | Net ($bn) | Net YoY |

|---|---|---|

| 2024 | 364.8 | +132.0% |

| 2023 | 157.3 | +171.3% |

| 2022 | 58.0 | +519.5% |

| 2021 | 9.4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($bn) | ROE% |

|---|---|---|

| 2024 | 507.5 | 13.9 |

| 2023 | 54.5 | 11.1 |

| 2022 | 17.5 | 16.0 |

| 2021 | 9.0 | 5.7 |

Source: SEC companyfacts cache [F1].

The drivers behind this performance reflect strategic priorities shifting towards expanding private-sector lending during fiscal tightening by the Argentine government, supported by enhanced deposit mobilization predominantly in both pesos and U.S. dollars [S23]. The profit surge also aligns with controlled expansion of loan portfolios that benefit from digital tools for rapid credit decision-making.

Liquidity and Capital Strength Provide a Buffer in a Volatile Market

Maintaining strong liquidity reserves has been crucial for BBVA Argentina given Argentina's economic fluctuations characterized by inflation volatility and currency movements [S6]. As of end-2025, the bank held liquidity indicators like Loan-to-Stable Customer Deposits (LtSCD) and Liquidity Coverage Ratio (LCR) comfortably within limits set forth by its Board [S4][S5]. Liquidity risk management extends intraday monitoring to ensure sufficient cash flow under stressed conditions.

Capital adequacy remains robust with a total capital ratio reported at approximately 17.5% by December 31, 2025 [S6], exceeding minimum regulatory requirements amid real-term credit growth pressures on capital [S6]. Economic capital models incorporate Basel-aligned methodologies covering credit, concentration, interest rate, market, operational, reputational, and strategic risks; credit risk consumes the largest share at about half of economic capital allocation [S15]. Stress testing using historical resampling techniques reaffirms solvency even under adverse macro scenarios [S15]. In asset-liability management, BBVA strategically maintains excess U.S. dollar-denominated assets over liabilities minimizing translation impacts due to exchange rate fluctuations [S16]. Notably, estimated net income impact from a ±10% peso currency valuation change approximates ±ARS15.8 billion as of year-end [S16].

Digital Transformation Initiatives Boost Customer Engagement and Efficiency

Leveraging the backing of the global BBVA Group’s technological ecosystem grants Banco BBVA Argentina significant competitive advantages in innovating client-facing platforms and operational processes [S6]. The bank’s digitalization strategy accelerates retail adoption rates since early pandemic years with ongoing refinement via collaborative cross-border developments within its parent group's platform network.

The focus on customer experience is quantified through tools such as Net Promoter Score (NPS), which guides service enhancements contributing to improved customer satisfaction levels [S6]. Digitally enabled credit underwriting tools including automated scoring and dynamic offer adjustments facilitate both speedier loan approvals and more tailored credit products—critical amidst inflation-driven demand variability [S7]. Simultaneously BBVA enhances product breadth including deposit offerings aligned with multi-currency client preferences fostering sustained market share gains across retail and commercial segments.

Macroeconomic Headwinds: Inflation, Currency Dynamics, and Regulatory Environment

Argentina’s persistently high inflation creates complex challenges impacting asset quality through increases in non-performing loans (NPLs), particularly evident within retail portfolios—credit cards and personal loans saw marked strain in late 2025 pushing the NPL ratio from about 1.5% at end-2024 up to nearly 4.9% as of December 31, 2025 [S7]. Correspondingly coverage ratios diminished materially reflecting increased provisioning needs.

Interest rate risk management is central given timing mismatches ('repricing gaps') between assets and liabilities; parallel rate shocks could reduce net portfolio values but increase net interest income due to re-pricing benefits documented by the Bank's sensitivity analyses showing manageable exposures under significant rate shifts such as immediate +500 basis points increments [S16]. Exchange rate volatility affects net interest income via derecognition or asset-liability valuation differences; hence conservative positioning of dollar assets over liabilities supports mitigation efforts.

On the regulatory front, the Central Bank tightly controls dividend authorizations under Communication "A" series rules including notable curbs introduced starting January 2023 restricting distributions to portioned installments capped at fractions of distributable profits with specific mandates regarding foreign exchange restrictions for non-resident shareholders seeking cash dividends requiring reinvestment into local bond securities [S19].

Dividend Strategy Amid Evolving Central Bank Dividend Authorization

Dividend payments have experienced triple-digit nominal escalations alongside surging earnings—from roughly ARS9 billion paid in FY2021 climbing sharply to over ARS507 billion disbursed during FY2024 as permitted within regulated boundaries [F1][S19]. However, actual payout capability is subject not only to accounting profit but also legal distributable profit definitions incorporating deductions for unrealized reserve items per BCRA frameworks.

Given continuing restrictions via Communications "A"7659 (Dec-22), "A"7719 (Mar-23), "A"7984 (Mar-24), and "A"7997 (Apr-24), banks require periodic Central Bank approval often staggered over multiple monthly installment payments limiting liquidity outflows despite record earnings [S19]. Non-resident shareholders face further constraints needing dividend monies channeled into eligible bond purchases unless special dispensation applies.

This tightly regulated environment demands judicious balancing between tangible shareholder returns vs retention of capital buffers necessary for ongoing risk absorption amid uncertain macroeconomic tides.

Risks: Credit Quality, Litigation, and Regulatory Compliance Challenges

Credit risk concentration manifests predominantly in retail segments where rising delinquencies heighten provisioning requirements reducing coverage ratios from historically comfortable levels near double digits down to about mid-90%s reflecting asset quality stress as inflation pressures mount [S7]. Commercial portfolio provisions have risen more modestly but warrant active surveillance.

Operationally significant litigation includes a pending class action filed by ACYMA alleging improper foreign currency conversion fees charged on certain credit card transactions without transparent exchange rates disclosure potentially exposing BBVA Argentina to damages or reputational harm if outcomes are unfavorable [S3].

In compliance domains, restrictive monetary policy controls require continuous engagement with regulators concerning dividend distribution regimes while adhering strictly to anti-money laundering statutes among other governance obligations overseen by dedicated control committees balanced with business unit coordination [S11][S22].

What to Monitor: Upcoming Milestones and Market Signals

Key forward-looking indicators worthy of close observation include: updates or relaxations to Central Bank dividend authorization policies which shape free cash flow availability; digital transformation progress particularly new feature introductions impacting customer acquisition/retention; non-performing loan trends especially within retail categories; and technical market signals such as recent bullish crosses beyond two hundred day moving averages indicating investor sentiment shifts [N1][N2].

Technological platform rollouts from parent entity create potential for scalable innovations yielding competitive differentiation whilst domestic macroprudential measures bear watching given their capacity to alter credit demand/supply dynamics substantially.

Capital Allocation Review: Balancing Dividends, Shareholder Returns, and Investment

The bank pursues capital discipline emphasizing liquidity preservation alongside measured shareholder return distributions primarily via dividends instead of share repurchases which remain minimal or unreported suggesting cautious deployment consistent with emerging market volatility considerations [F1][S19].

Cash flow statements indicate ample operating cash generation supporting dividend funding yet deliberate restraint persists reflecting internal prioritization of solvency over aggressive payout policies—a prudent stance given inflation uncertainties compounded by regulatory constraints.

Additionally investing into technology-driven service improvements signifies recognition that long-term value creation requires marrying traditional balance sheet strength with digital-enhanced client engagement capabilities fostering sustainable franchise growth.

This analysis leverages publicly available regulatory filings dated up through April 2026 alongside recent market news articles without offering investment advice or price guidance. Readers should weigh Banco BBVA Argentina's performance within broader country-specific macroeconomic contexts acknowledging inherent emerging market risks alongside operational execution achievements.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments