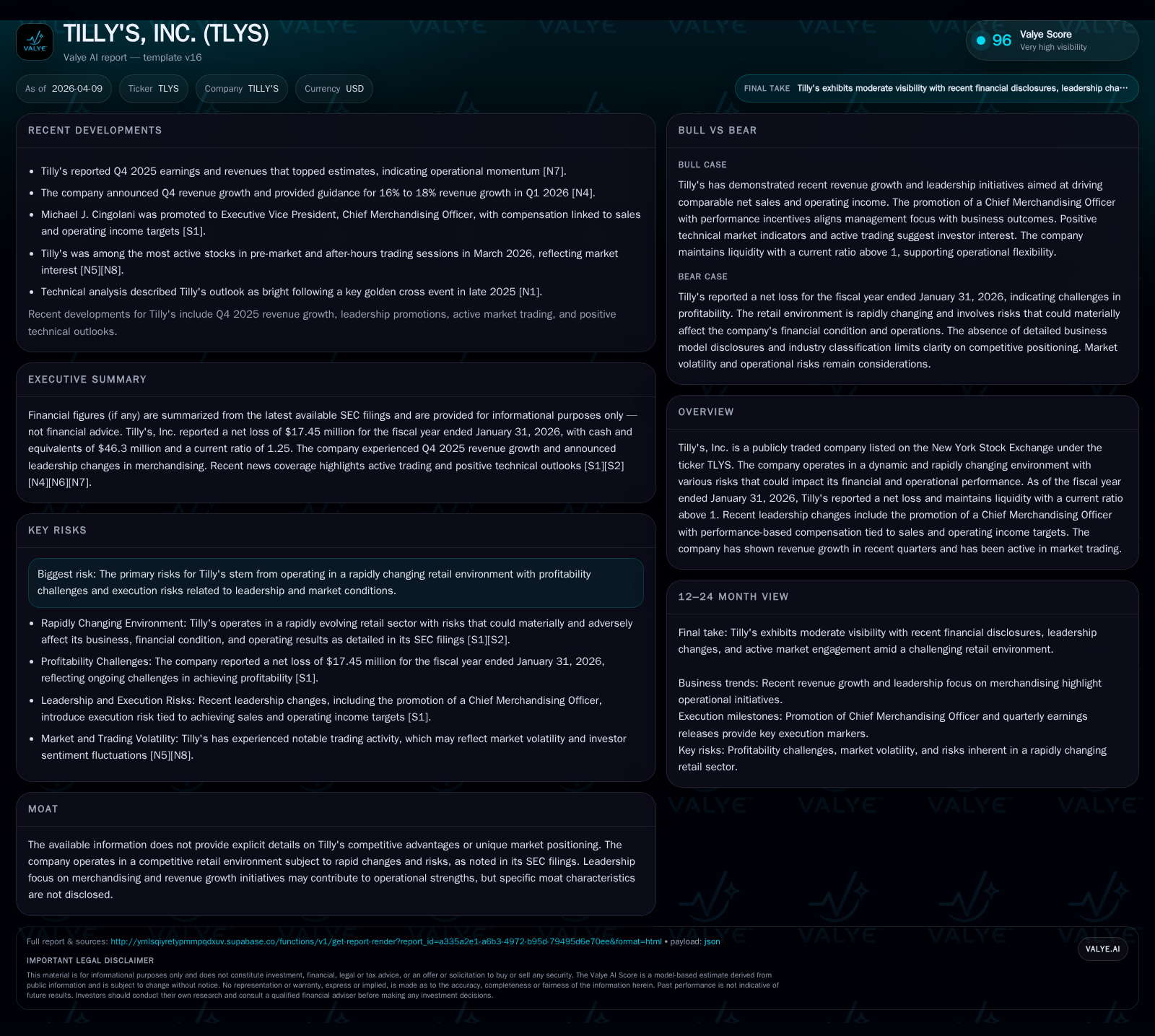

Tilly's, Inc. Shifts Gear Toward Revenue Growth Despite Profitability Pressures

Tilly's recent financials reveal early signs of operational recovery driven by merchandising leadership, amid ongoing losses and a focus on liquidity preservation.

Tilly's, Inc. is transitioning from multi-year operating losses toward modest revenue growth, spurred by strategic merchandising leadership changes. Fiscal 2025 showed a near 3% decline in revenues, but a more than 60% improvement in operating income losses alongside a positive swing in operating cash flow. Management projects strong revenue growth in Q1 2026, underscoring confidence in top-line momentum while ongoing profitability challenges remain. The company maintains solid liquidity with a current ratio above one and stable cash reserves. Capital allocation remains disciplined with no recent dividends or buybacks; equity incentive plan amendments and CEO option cancellations highlight management’s realignment efforts. Risks persist from rapid market shifts and execution demands inherent in retail.

From Past Losses to Recent Sales Uptick: Financial Trajectory

Tilly's has experienced a multi-year decline in revenues since the fiscal year ended FY2022, with sales dropping from $177.8 million then to $139.6 million as of FY2025, marking a cumulative downward trajectory influenced by competitive pressures and evolving retail dynamics [F1]. The latest fiscal year showed a year-over-year revenue decline of approximately 2.7%, extending the soft revenue environment.

Yet within this top-line contraction lies a notable operational improvement: operating income losses have shrunk substantially from -$49.8 million in FY2024 to -$19.3 million in FY2025 — an impressive narrowing by over 61%. Correspondingly, net losses retreated by more than 62% to -$17.45 million [F1]. This suggests cost controls and efficiency measures have contributed positively despite ongoing revenue challenges.

Cash flow trends corroborate this operational turning point. After consecutive years of negative operating cash flow—dropping as low as -$42 million in FY2024—the company posted positive CFO of $4.1 million for FY2025 alone, representing a near doubling (109.8%) versus the prior year [F1]. Still, free cash flow remains marginally negative when accounting for reduced capital spending of $4.7 million (down 43%) [F1]. These cash flow improvements provide crucial breathing room for the company’s turnaround initiatives.

Importantly, recent quarterly trends reported post-FY results indicate an inflection point on the revenue front: Q4 FY25 results beat estimates amid increasing same-store sales growth [N1][N3], pointing toward emerging top-line momentum.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 140 | -17 | 4 | -19 | -2.7% | +62.2% |

| 2024 | 143 | -46 | -42 | -50 | -13.8% | -34.0% |

| 2023 | 166 | -34 | -7 | -31 | -6.4% | -456.4% |

| 2022 | 178 | 10 | -1 | 11 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | -1 | ||

| 2024 | 0 | -50 | |

| 2023 | 0 | 0 | -21 |

| 2022 | 0 | 11 | -17 |

Source: SEC companyfacts cache [F1].

Leadership and Merchandising: New Strategic Drivers

A key inflection behind the improving financial metrics appears linked to strategic leadership modifications, most notably within merchandising operations—a critical lever for specialty retailers like Tilly's.

On March 10, 2026, Tilly's elevated Michael J. Cingolani to Executive Vice President and Chief Merchandising Officer after serving as Senior VP and General Merchandising Manager [S17]. His compensation package explicitly ties annual bonus potential (targeting up to 150% of base salary) to exceeding budgeted comparable net sales figures and pre-bonus operating income targets for fiscal year activity [S17][N2].

This alignment signals the board's heightened emphasis on driving top-line sales through refined merchandising strategy while concurrently improving operating efficiency—two complementary objectives necessary for exiting prolonged unprofitability.

Merchandising leadership has been repositioned as pivotal not merely for assortment curation but also for balancing inventory risk with maximizing sell-through rates amid rapidly changing consumer preferences.

Forecasting Growth and Profitability Milestones

Concrete guidance addresses the near term optimism around volume growth: management anticipates first-quarter fiscal year 2026 revenue to grow between 16% and18%, reflecting strength carried from recent quarters [N1]. This anticipated acceleration follows positive Q4 performance which exceeded consensus on both top-line and earnings per share metrics [N3].

However, explicit profit milestone forecasts remain less detailed publicly—no firm targets on when operating losses might fully reverse have been disclosed [N2]. The trajectory from large operating deficits toward smaller ones, combined with positive ongoing cash flows, suggests breakeven or marginal profitability could emerge if current trends persist.

Investors should watch upcoming quarterly comparable store sales data and gross margin developments closely as indicators of sustainable operational improvements.

Capital Structure, Liquidity, and Financial Flexibility

Financial flexibility remains intact despite ongoing losses—an essential factor supporting Tilly's ability to implement turnaround plans.

As of January 31, 2026, cash & equivalents stood at approximately $46.3 million while current assets totaled around $125 million against current liabilities near $100 million [F1], resulting in a healthy current ratio of about 1.25 [F1]. This level suggests sound short-term liquidity buffers that could meet operational working capital needs without reliance on external financing.

Recent filings show no material near-term debt maturities or restrictive covenants threatening liquidity [S7][S8][S9][S10]. This balance sheet stability affords management runway to recalibrate merchandising assumptions and invest selectively within capex constraints—evidenced by step-down capital spending in FY2025—while navigating competitive pressures.

Shareholder Returns and Capital Deployment Trends

Capital allocation reflects prudent stewardship amid restructuring priorities.

The company has not declared dividends or engaged in share repurchases since fiscal year ended February 1, 2024 [F1], consistent with conserving cash during loss-reduction phases.

Governance actions include amending the Third Amended and Restated Equity Incentive Award Plan to increase maximum shares granted per award annually up to 2,500,000 shares [S14][S16]. Concurrently, CEO Nathan Smith mutually agreed with the company to cancel previously granted time-based and performance-based stock options totaling up to 1,800,000 shares but received replacement awards under this amended plan promptly after cancellation [S14].

These moves signal an effort to better align executive incentives with long-term shareholder value creation tied to performance milestones rather than historical stock option terms alone.

No new dividend programs or buyback initiatives have been announced post these changes [F1], indicating retention of capital is prioritized until sustained profitability returns.

Risks in a Rapidly Changing Retail Environment

Tilly's operates amidst significant sector volatility characterized by shifting consumer demand patterns accelerated digital disruption and intense pricing competition [S2][S4][S5][S6].

The company highlights risks linked to execution uncertainties from leadership transitions compounded by macroeconomic pressures affecting discretionary consumer spending habits [S2][S4].

Material risk factors include inventory management challenges amid shortening fashion cycles; supply chain disruptions exacerbated by global trade complexities; plus e-commerce evolution competing for consumer mindshare — all catalyzing operational hurdles potentially disrupting progress toward profitability stabilization.

Investors monitoring Tilly's progress must consider these fundamental sector headwinds alongside internal transformation efforts as intertwined determinants shaping medium-term outcomes.

This analysis synthesizes publicly available financial statements, SEC disclosures, and recent earnings commentary without extrapolating beyond provided evidence or offering investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments