IX Acquisition Corp.: Cash Constraints and Business Combination Risks Cloud Prospects

The company's liquidity challenges and regulatory uncertainties cast a shadow over its planned merger with AKOMM Inc.

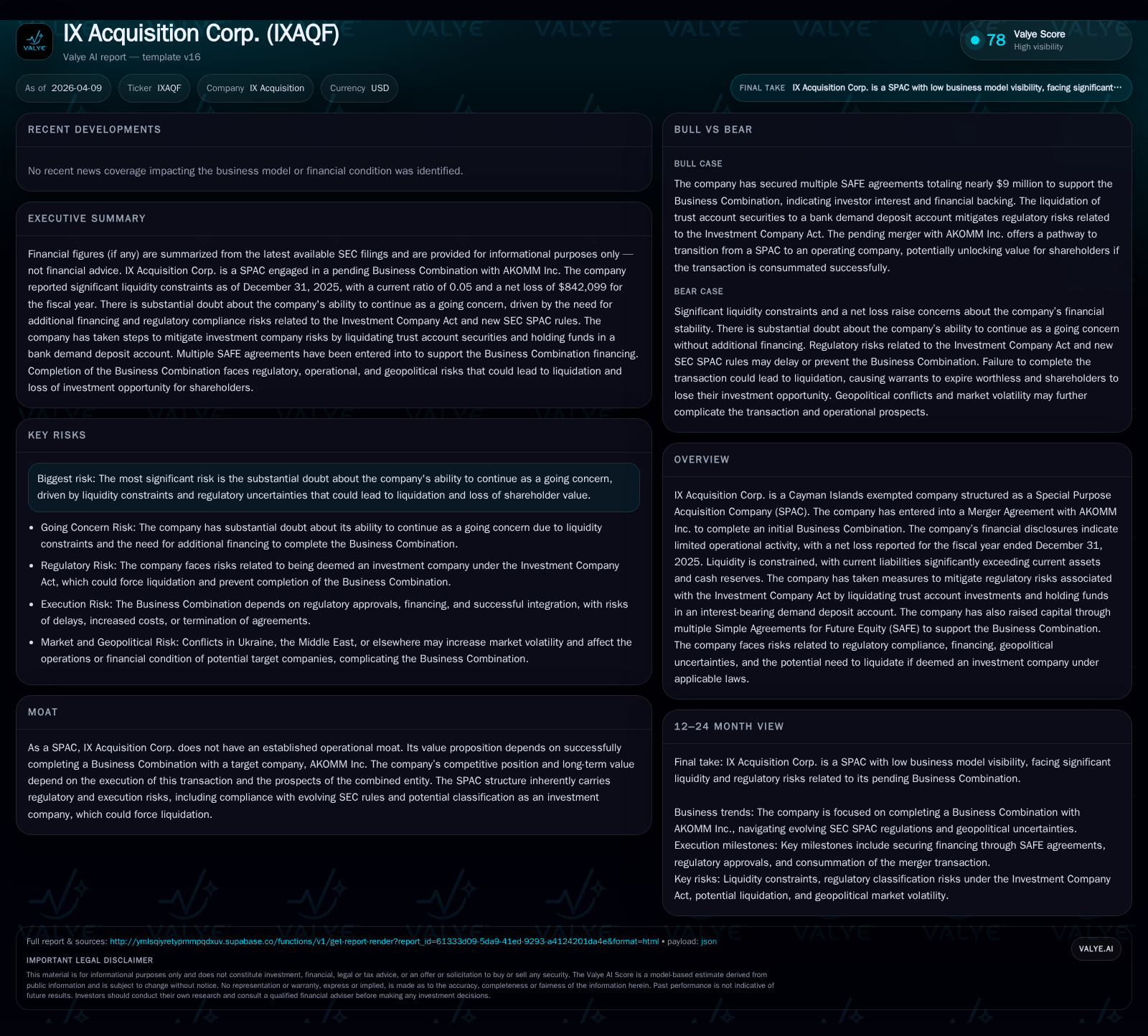

IX Acquisition Corp. operates as a SPAC focused on completing a business combination with AKOMM Inc. While operating losses have narrowed significantly, the company faces acute liquidity pressures, evidenced by a current ratio near 0.05 and negative equity exceeding $15 million at the end of 2025 [F1]. Regulatory headwinds from new SEC SPAC rules effective July 2024 and risks tied to Investment Company Act classifications increase the threat of forced liquidation [S8][S9][S10]. Capital raised through multiple SAFE agreements provides some financing flexibility, but operational and merger execution risks remain material [S21][S14]. The company’s outlook hinges on timely deal completion amid constrained cash resources and evolving regulatory scrutiny.

Historical Financial Performance: A Brief Overview

IX Acquisition Corp.’s financial statements over the four fiscal years ending December 31 illustrate a profile consistent with a Special Purpose Acquisition Company (SPAC) yet to complete its initial business combination. Operating income remained negative throughout but showed marked improvement in FY2025 at approximately -$205k compared to -$2.75 million in FY2024, suggesting tighter expense control or reduced transaction-related costs [F1]. Net income also improved substantially, narrowing losses from around -$2.3 million in FY2024 to about -$842k in FY2025.

Operating cash flow shifted from negative outflows exceeding $1 million in FY2024 to a positive inflow near $596k in FY2025, likely reflecting timing differences in working capital management or financing activities including proceeds from SAFE agreements [F1]. However, balance sheet stress remains acute: current assets totaled roughly $379k against current liabilities exceeding $7 million at year-end 2025, yielding a critically low current ratio near 0.05—a strong indicator of liquidity risk amid complex merger execution demands.

Equity deteriorated further from negative $13.6 million at end-2024 to negative $15.5 million by end-2025, reflecting cumulative net losses and contingent obligations associated with business combination efforts and related financing instruments.

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -1 | 595839 | 0 | +63.0% |

| 2024 | -2 | -1392690 | -3 | -156.6% |

| 2023 | 4 | -605726 | -1 | -56.7% |

| 2022 | 9 | -558681 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 5.4 |

| 2024 | 16.7 |

| 2023 | -42.2 |

| 2022 | -70.4 |

Source: SEC companyfacts cache [F1].

Figures sourced from SEC filings via companyfacts snapshot [F1].

Drivers Behind Recent Financial Trends

IX Acquisition’s operating results reflect typical SPAC dynamics: absent meaningful operating revenues prior to merger completion with AKOMM Inc., expenses largely consist of deal sourcing costs, regulatory compliance fees including legal and accounting expenses, and administrative overhead.

Notably, on November 13, 2023 the company strategically liquidated trust account investments previously held in U.S. government treasury securities and money market funds into lower-yield interest-bearing demand deposits to mitigate risk of being classified as an investment company under the Investment Company Act [S2][S6][S7][S8]. This action reduced interest income potential relative to previous periods.

Financing costs increased due to multiple Simple Agreements for Future Equity (SAFE) raising approximately $6.5 million intended to support merger funding and working capital needs within the corporate structure [S21]. While providing necessary capital influxes enabling ongoing operations and deal negotiations, these arrangements contribute to net loss levels through associated expenses until conversion upon merger closure.

Overall earnings remain negative but recent improvements suggest expense discipline possibly linked to winding down certain activities as the merger progresses.

Regulatory Environment Impacting IX Acquisition

New SEC regulations effective July 1st, 2024 impose enhanced disclosure requirements on SPAC transactions involving shell companies like IX Acquisition [S8][S9][S10]. These "SPAC Rules" increase transparency around financial information and projections associated with business combinations.

Additionally, SEC guidance emphasizes enforcement risks related to unintended classification as an unregistered investment company under Section 3(a)(1)(A) of the Investment Company Act [S10][S11]. To address this risk proactively IX Acquisition liquidated trust account securities into bank deposits despite lower yields—a tradeoff accepted to preserve entity viability pending successful deal closure.

Non-compliance could trigger accelerated liquidation timelines forcing premature wind-down rather than successful business combination completion—jeopardizing investor value.

Strategic Path Forward: Merger Prospects and Risks

IX Acquisition entered into a definitive Merger Agreement with AKOMM Inc., aiming for an initial Business Combination that would transform IX from a shell entity into an operating company via reverse merger or similar transaction structure [S14]. The agreement includes customary contingencies such as obtaining required regulatory approvals timely.

Risks include potential delays or restrictions on governmental consents; post-merger integration challenges including realization of cost synergies; and financing dependencies tied to SAFE instruments which convert at closing prices embedding dilution though providing critical capital support [S14][S21].

Management must also manage operational continuity amid prolonged negotiations which historically can disrupt focus ahead of closing.

No explicit timeline milestones beyond public disclosures are available; close monitoring of completion dates will be essential.

Liquidity Position and Capital Structure Considerations

Liquidity metrics reveal extreme short-term solvency stress: current assets near $379k contrast sharply with current liabilities over $7 million at December 31st resulting in a current ratio approximating just 0.05 [F1]. Cash & equivalents stand at about $179k limiting flexibility amid growing payables and SAFEs awaiting conversion or repayment events linked directly to merger success scenarios [F1][S26].

Management discloses substantial doubt about continuing as a going concern driven by liquidity constraints and deadlines requiring either transaction completion or liquidation within roughly one year from late-2025 reports issued around April 9th [S2][S6][S7].

Capital structure complexity includes sponsor promissory notes repaid periodically along with accrued working capital advances detailed across recent filings supporting ongoing corporate functions during extended negotiation phases [S26].

This situation underscores operational sustainability challenges pending regulatory approvals coupled with timely access to planned SAFE conversions for solvency relief.

Capital Allocation Focused on Deal Execution; No Shareholder Distributions Reported

IX Acquisition’s capital deployment centers exclusively on supporting its planned initial Business Combination rather than shareholder returns such as dividends or share buybacks—none reported since inception consistent with standard SPAC lifecycle practices emphasizing deal facilitation over income distributions [F1][S19]-[S28].

SAFE fundraising totaling approximately $6.5 million across multiple tranches finances merger-related expenses including working capital needs during protracted pre-closing phases documented within Commercial Funding Repayment Agreements containing conversion price formulas and escrow provisions aligned with incentive structures aimed at sponsor alignment while increasing complexity around timing expectations vis-à-vis shareholders [S21].

Recent improvements yield an approximate return on equity near +5.4% calculated as net income over negative equity base; this metric reflects accounting effects more than sustainable profitability given ongoing losses and structural characteristics typical of SPACs prior to business combination completion [F1].

Positive operating cash flow emerged only recently mitigating concerns about cash burn rates; however usage flexibility remains predominantly earmarked for executing combination steps rather than discretionary shareholder payouts until post-merger operating revenues materialize.

Risks Related to Investment Company Act Classification and SEC Compliance

IX Acquisition faces fundamental risks from possible classification as an unregistered investment company under Section 3(a)(1)(A) of the Investment Company Act based on fund holding patterns or evolving SEC staff interpretations affecting SPACs broadly [S3][S4][S6]-[S7][S12]-[S13].

Such classification could compel abandoning business combination efforts followed by mandatory liquidation potentially erasing investor principal aside from residual trust account recoveries after expenses—an outcome mitigated currently by liquidating securities into demand deposits despite lower yields accepted pragmatically for compliance purposes.

These legal risks compound execution challenges heightened by new SEC disclosure standards effective mid-2024 raising deal transparency but also increasing costs and time needed for completion possibly causing earlier liquidation triggers absent waiver or extension measures.

Investor confidence is vulnerable amid this regulatory tightening landscape demanding careful monitoring.

Outlook: Key Milestones and Monitoring Points Ahead

While no precise forward guidance on closing dates or interim funding injections is publicly available beyond documented SAFE tranches, stakeholders should focus on critical junctures including:

- Timely completion feasibility aligned with regulatory deadlines imposed by new SPAC rules effective July 1st,

- Trust Account balances post-liquidity transformations supporting redemption rights if exercised,

- Shareholder voting outcomes on definitive merger proxies,

- Progress toward satisfying all material conditions precedent notably governmental approvals without delay,

- Any SEC enforcement actions or interpretive guidance impacting eligibility under Investment Company Act definitions,

- Timely conversion of SAFEs delivering essential working capital relief,

- External geopolitical uncertainties influencing market volatility potentially affecting target valuations, and eventual integration performance post-merger concerning synergy realization timelines typically uncertain but critical for combined entity value creation.

Continuous monitoring of these factors will be crucial for investors evaluating IX Acquisition’s trajectory toward either successful combination unlocking value or compelled liquidation resulting in orderly wind-down consistent with regulatory compliance mandates.

Disclaimer: This analysis is based solely on public SEC filings and official company disclosures available up to April 9th, 2026; no confidential information was accessed nor speculative assumptions made beyond documented facts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments