Li Auto Inc. Confronts Profit Volatility Amid Rising R&D and Market Competition

Li Auto's recent financial slip contrasts with strong delivery growth and technological investments in China's evolving NEV sector.

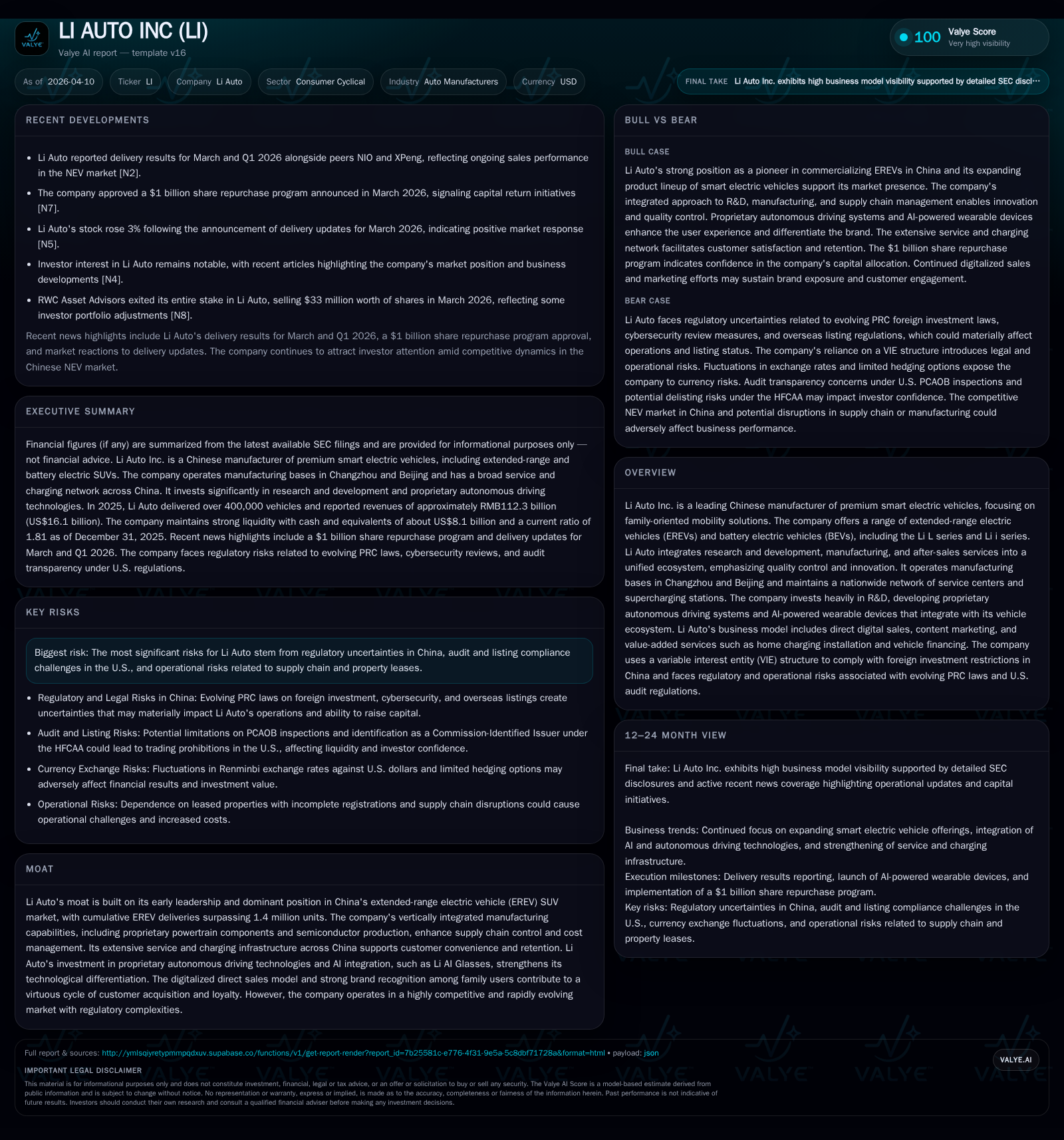

Li Auto Inc. has solidified its leadership position in China’s extended-range electric vehicle SUV market, boasting over 1.5 million cumulative deliveries as of end-2025. Despite this volume growth, the company reported a sharp operating loss in 2025, marking a reversal from profitable years prior, driven largely by significant research and development expenses and evolving market dynamics. Li Auto’s vertically integrated manufacturing, proprietary technology development, and expansive direct sales and service infrastructure underpin its moat; however, regulatory uncertainties and intensifying competition could limit near-term profitability. Capital allocation remains focused on growth with meaningful capital expenditures and a recently approved $1 billion share repurchase authorized in early 2026.

Company Overview and Market Position

Li Auto Inc. operates as a leading player in China's new energy vehicle (NEV) industry, specializing principally in premium smart electric vehicles that cater to family-oriented mobility needs [S1]. The company distinguishes itself as an early pioneer commercializing extended-range electric vehicles (EREVs) with volume production initiated in late 2019 by its flagship Li ONE model. As of December 31, 2025, cumulative deliveries exceeded 1.5 million units — primarily within the EREV SUV segment — establishing Li Auto's commanding presence in this lucrative niche [S1].

The firm employs a vertically integrated manufacturing strategy spanning proprietary powertrain development including SiC-based semiconductor manufacturing for its high-voltage electric drive systems, underpinned by dedicated plants in Changzhou and Beijing [S22]. This enables greater supply chain resilience amidst global component shortages that continue to challenge EV manufacturers broadly.

Historical Financial Performance

While Li Auto enjoyed profitable operations through much of the early-to-mid-2020s period, 2025 marks a notable shift in financial outcomes [F1]. Operating income swung from positive USD $961.6 million in FY2024 to a loss of USD $74.5 million in FY2025, representing over a 100% decline year-over-year [F1]. This reversal underscores mounting cost pressures linked to robust R&D investment as well as evolving competitive dynamics.

Operating cash flow experienced an even more pronounced deterioration, moving from strong inflows of USD $2.18 billion in 2024 to an outflow of USD $1.23 billion in the latest full fiscal year [F1]. Concurrently, capital expenditures declined by nearly half to USD $601 million as the company optimized production capacity expansion investments following earlier build-out phases [F1]. Net income figures prior to FY2022 remain limited but approximately suggest negative returns relative to shareholder equity — computed at about -0.5% ROE for latest periods using available valuation metrics [F1].

Financial Summary Table (USD Millions)

Historical performance (annual)

| FY | CFO ($bn) | OpInc ($mm) | Capex ($mm) |

|---|---|---|---|

| 2025 | -1.2 | -75 | 601 |

| 2024 | 2.2 | 962 | 1059 |

| 2023 | 7.1 | 1043 | 917 |

| 2022 | 1.1 | -530 | 743 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($bn) |

|---|---|

| 2025 | -1.8 |

| 2024 | 1.1 |

| 2023 | 6.2 |

| 2022 | 0.3 |

Source: SEC companyfacts cache [F1].

*Revenue figures are not explicitly reported within provided data.

Business Model and Product Strategy

Li Auto’s core approach revolves around offering technologically advanced extended-range electric SUVs alongside a growing portfolio of battery electric vehicles (BEVs), structured across its Li L series (EREVs) and Li i series (BEVs) [S5][S9][S10]. The products are engineered especially for families with an emphasis on safety, convenience, and comfort.

Selling directly through an extensive digitalized channel ecosystem enhances customer engagement efficiency while controlling acquisition costs. In addition to digital ordering platforms that require modest deposits convertible upon order confirmation within a day, Li Auto supplements customer experience via test drives at strategically located retail stores (over 540 locations nationwide), robust after-sales services from more than 560 service centers across major urban hubs, and extensive supercharging infrastructure exceeding nearly four thousand stations [S5][S9].

The company leverages innovative marketing strategies centered on content-driven campaigns utilizing short-video platforms targeting tech-savvy consumers alongside encouraging organic word-of-mouth referrals via satisfied owners [S9].

Value-added monetization includes home charger installations, vehicle financing services integrated into the purchasing journey, membership programs like "Li Plus," insurance offerings, used car trade-ins - creating multiple revenue streams beyond initial vehicle sales [S9][S25].

Future Growth Prospects

Li Auto’s growth hinges on several key vectors: expanding its BEV lineup to complement the established EREV series; elevating proprietary autonomous driving capabilities bolstered by AI-powered devices (e.g., Li AI Glasses); scaling manufacturing efficiencies through continued automation; and deepening customer loyalty via enhanced digital sales-service feedback loops [S10][S22]. The company also targets penetrating broader demographic segments within families seeking affordable premium smart EVs priced above RMB200,000 (~USD $28,600) [S12].

However, future profitability is at risk due to heightened competition from both domestic NEV giants such as NIO and XPeng (competing on similar price points and tech features) as well as global incumbents increasing investment into Chinese markets [N3][N4][N5]. Regulatory risks remain salient including potential impacts from tightened Sino-American audit compliance regimes under the Holding Foreign Companies Accountable Act which threatens trading eligibility of ADS shares if audit inspections fail [S6][S13]. Additionally, PRC foreign exchange controls restrict liquidity movement from offshore subsidiaries complicating dividend flows [S4][S18].

The Chinese government’s evolving regulatory stance on cybersecurity reviews for overseas listings could also impose unforeseen compliance burdens or delays affecting capital raising plans [S6]. These gen-pop risks could constrain Li Auto’s ability to raise fresh equity or debt on favorable terms if required.

Forecasts / Milestones / What To Watch For (Analysis)

While explicit revenue guidance was not provided within available documents or news releases through April 2026 [N2], key monitoring points include:

- Quarterly delivery volumes versus competitors’ performance during key sales seasons,

- Margins evolving post-R&D peak investment phase,

- Regulatory developments regarding U.S.-China audit oversight,

- Progression of the BEV product pipeline launch cadence expected through mid-late decade,

- Operational efficiency measured by unit cost improvements enabled by proprietary semiconductor production,

- Impact of value-added services adoption rates on overall user lifetime value.

Investors should also watch management commentary around capital expenditure plans beyond current levels (notably down ~43% YoY indicating potential tapering), share buyback execution following the recently authorized $1 billion program announced March 24, 2026 ([N10]), and institutional shareholding changes such as RWC Asset Advisors’ complete exit earlier that month ([N11]) suggesting shifting sentiment.

Returns / Capital Allocation

Li Auto maintains a strong liquidity position with cash and equivalents around USD $8.1 billion end-2025 despite operational challenges driving negative cash flow last year [F1][S7][S18]. However, the stark swing from previously positive free cash flow points toward temporary strain likely due to ramped up R&D outlays ($11.3B RMB or roughly USD $1.7B), product line expansions, and working capital fluctuations tied to supply chain adjustments.

Capital expenditure trimming from over USD $1 billion to approximately USD $601 million aligns with entering more stable production phases after rapid facility build-outs earlier [F1][S18], prepping for margin improvements if demand sustains.

Dividend distributions are subject to PRC regulatory controls on foreign exchange remittances compounded by statutory reserve requirements restricting repatriation from subsidiaries [S19][S20]. The company has not indicated dividend payments or yield targets but has prioritized share buybacks signaling confidence in intrinsic valuation supported by sustained volume momentum.

Risks Summary

Apart from financial volatility risks tied to large-scale technology investments and margin pressures inherently present in fast-growing automotive manufacturers expanding digitally integrated premium product lines, several other constraints loom prominently:

- Regulatory uncertainty stemming from PRC government foreign investment policies,

- Potential delisting threats due to PCAOB audit inspection access limitations,[S6][S13]

- Geopolitical tensions impacting trade policies,

- Supply chain disruptions given intensive reliance on semiconductor components,

- Competitive pressures from incumbent global automakers aggressively entering Chinese NEV space ([N3]).

- Legal complexities around enforcement of shareholder rights given Cayman Islands incorporation coupled with China jurisdiction complications limiting overseas regulatory investigations effectiveness ([S17]).

Conclusion

Li Auto Inc.’s trajectory reflects both pioneering accomplishments in capturing significant share of China’s extended-range electric SUV segment alongside fierce operational challenges impacting near-term profitability metrics. Its robust direct sales network combined with proprietary technologies offer tangible competitive moats but require navigating a complex regulatory environment alongside intensifying marketplace rivalry.

Maintaining focus on technological innovation including further advances into BEV platforms and autonomous systems while controlling manufacturing costs will remain critical strategic pillars going forward. Close attention should be paid to quarterly operational updates detailing how effectively Li manages R&D spending against delivery growth trends amid macroeconomic headwinds.

This analysis is based solely on information provided through company filings and public news sources up to April 10, 2026. It omits investment recommendations or price forecasts per policy guidelines.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments