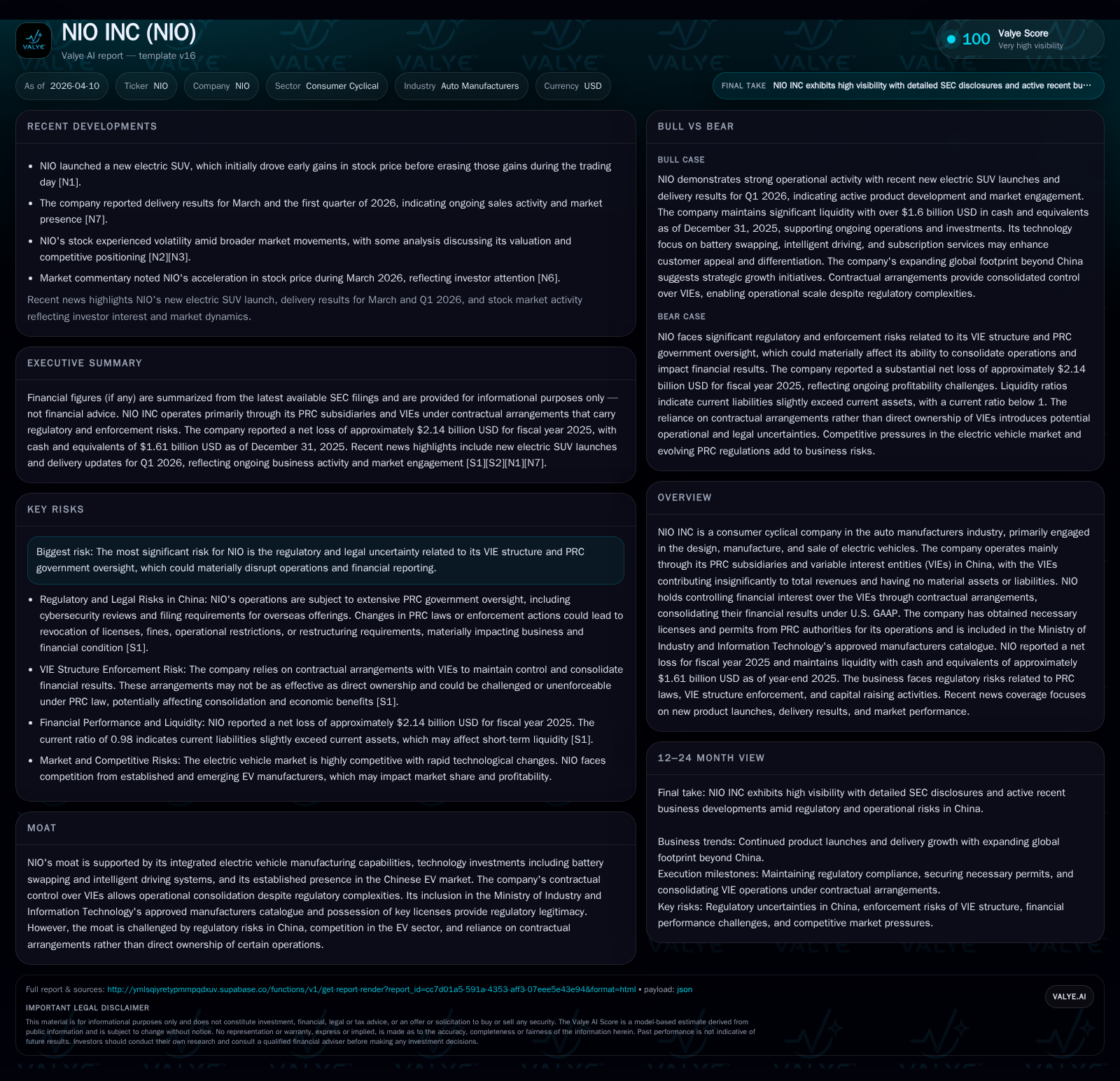

NIO Inc.'s Strategic Growth and Regulatory Risks Shape Financial Performance and Outlook

NIO Inc. balances technological innovation and market expansion with complex regulatory challenges impacting its operational control and financial consolidation.

NIO Inc., a leading Chinese electric vehicle manufacturer, has experienced narrowing operating losses and improved cash flow generation in recent years, supported by increased deliveries and technological advancements such as battery swapping. Despite posting a net loss in 2025, NIO maintains over $1.6 billion in cash and equivalents. The company relies on contractual VIE structures for operational control, which introduces regulatory uncertainty amid evolving PRC laws. Future growth depends on navigating China's regulatory landscape, expanding production capacity, and sustaining product differentiation. Investors should monitor regulatory developments alongside delivery metrics and capital structure evolution.

Historical Financial Performance

NIO Inc., operating primarily through its PRC subsidiaries and contractual VIE structures, reported continuing net losses but improving operating trends through fiscal year 2025 [F1][S1]. While recent revenue figures beyond 2018 are not explicitly stated in the latest data, operating income and net loss trajectories illustrate the firm’s financial challenges amid its growth phase.

Historical performance (annual)

| FY | Net ($bn) | CFO ($mm) | OpInc ($bn) | Capex ($bn) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -2.1 | 428 | -2.0 | 0.9 | +30.4% |

| 2024 | -3.1 | -1075 | -3.0 | 1.3 | -5.2% |

| 2023 | -2.9 | -195 | -3.2 | 2.0 | -39.4% |

| 2022 | -2.1 | -561 | -2.3 | 1.0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($bn) | ROE% |

|---|---|---|

| 2025 | -0.4 | -359.2 |

| 2024 | -2.3 | -375.4 |

| 2023 | -2.2 | -81.1 |

| 2022 | -1.6 | -60.5 |

Source: SEC companyfacts cache [F1].

Note: Monetary figures are in millions USD; capital expenditures declined approximately 31% year-over-year from 2024 to 2025; operating income improved roughly 33% year-over-year.

Despite persistent net losses exceeding $2 billion annually since at least 2022 [F1], NIO has demonstrated signs of operational improvement with reduced losses from peak negatives experienced during FY2023-24 periods [F1]. Notably, operating cash flow turned positive for the first time in several years during FY2025 with nearly $428 million generated [F1], indicating improved working capital management or underlying business performance.

Capital expenditures remain significant as the company continues investing in manufacturing capabilities and technology initiatives including battery swapping infrastructure and intelligent driving systems [S1][S4]. These investments are capital-intensive but vital for competitiveness within China’s rapidly evolving electric vehicle market.

The company’s book equity declined sharply from over $3 billion at the end of FY2023 to below $600 million by FY2025 [F1], driven primarily by accumulated losses outpacing retained earnings.

Drivers Behind Past Performance

Key factors influencing NIO’s historical results include:

- Market Penetration: Increasing presence in China’s EV sector supported by innovative powertrain technologies such as battery-as-a-service offerings.

- Product Launches: Introduction of new SUV models expanded consumer appeal but incurred upfront costs impacting profitability [N1][N8].

- Scaling Challenges: High manufacturing ramp-up costs affecting margins; managing supply chain complexities amid competition from incumbent OEMs and Chinese EV startups.

- Regulatory Structure: Reliance on VIE contractual arrangements allowed access to restricted sectors but imposed legal risks affecting investor sentiment [S1][S7][S11].

Future Growth Prospects

Looking ahead, NIO’s growth will likely be shaped by:

- New Product Pipeline: Continued rollouts like recent electric SUVs aim to capture more domestic market share [N1].

- Technological Differentiation: Enhancements in intelligent driving systems along with battery swapping network expansion may drive customer retention and recurring revenues via subscription services [S1][S4].

- Regulatory Environment: Uncertainty around China’s evolving foreign investment laws tied to VIEs remains a significant risk; adverse changes could disrupt control over key operations or impair financial consolidation [S4][S8][S11].

- Market Competition: Intensifying competition among Chinese EV makers including XPeng, Li Auto, and Tesla represents an ongoing challenge for margin expansion and volume growth [N8].

While explicit guidance for FY2026 is not provided, important milestones include quarterly delivery updates, cost structure improvements reflected in future earnings releases, successful navigation of any additional licensing or regulatory filings required by authorities such as the China Securities Regulatory Commission (CSRC), as well as capital markets activity that could affect liquidity resources [S4][S15].

Returns & Capital Allocation

NIO currently does not pay dividends nor has it announced share buybacks given the ongoing necessity for heavy reinvestment into production capacity and technology development [S18][S19][S20]. With multiple convertible notes outstanding due between 2027–2030 [S16][S17], managing debt maturities alongside cash flow generation is critical.

The approximate return on equity based on last reported net income relative to equity is highly negative (-359%) reflecting large accumulated losses against diminished equity base [F1]. However, positive CFO in FY2025 marks an inflection point possibly indicating leverage on improved unit economics going forward.

Industry Analysis — Navigating Regulatory Complexity & Operational Control Structures

NIO operates under a common yet intricate structure among Chinese tech-related companies listed abroad involving Variable Interest Entities (VIEs). While these arrangements afford access to restricted sectors such as internet content provision combined with automotive licensing, they expose investors to considerable policy uncertainty given potential PRC government intervention which could invalidate contract enforceability or force restructuring [S4][S7][S11]. The company consolidates these entities under US GAAP based on deemed financial control via contracts rather than direct equity ownership — a distinction with material impact if regulations tighten unexpectedly.

Moreover, NIO's listings on multiple exchanges including NYSE and Singapore Exchange subject it to dual compliance frameworks where Cayman Islands law governance practices differ from U.S./NYSE norms which may complicate shareholder protections [S9]. The Holding Foreign Companies Accountable Act (HFCAA) risk fluctuates with PCAOB inspection capabilities over auditors located in China/Hong Kong but recent developments lessen immediate delisting threats though monitoring remains prudent [S6][S15].

Recent Developments & Market Perception

Recent news highlights product cadence with new electric SUV launches driving variable stock price reactions amid broader market volatility [N1][N2][N7]. Delivery volume reports for Q1 2026 suggested continued momentum alongside peers XPeng and Li Auto though market appetite remains sensitive to regulatory newsflow along with macroeconomic conditions affecting EV demand domestically [N8][N9]. Analysts debate valuation attractiveness given rich technological outlook contrasted against profit volatility [N4][N13].

Conclusion & Watch Points

In summary, NIO illustrates a high-growth EV manufacturer navigating internal scaling expenses and external regulatory headwinds inherent to Chinese tech-enabled automotive firms utilizing VIE frameworks [F1][S4]. Sustainable profitability hinges on expanding sales volumes through new models paired with cost containment while managing evolving compliance requirements mandated by PRC authorities.

Key factors investors should monitor include quarterly delivery metrics aligned against cost trends; any official announcements related to enforcement actions surrounding VIE contracts; changes in domestic licensing statuses; convertible debt maturity management; and shifts in capital structure policies potentially introducing dividends or buybacks once profitability stabilizes.

Disclaimer: This report is intended solely for informational purposes based on available data as of April 10, 2026 without offering investment advice or recommendations regarding securities discussed herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments