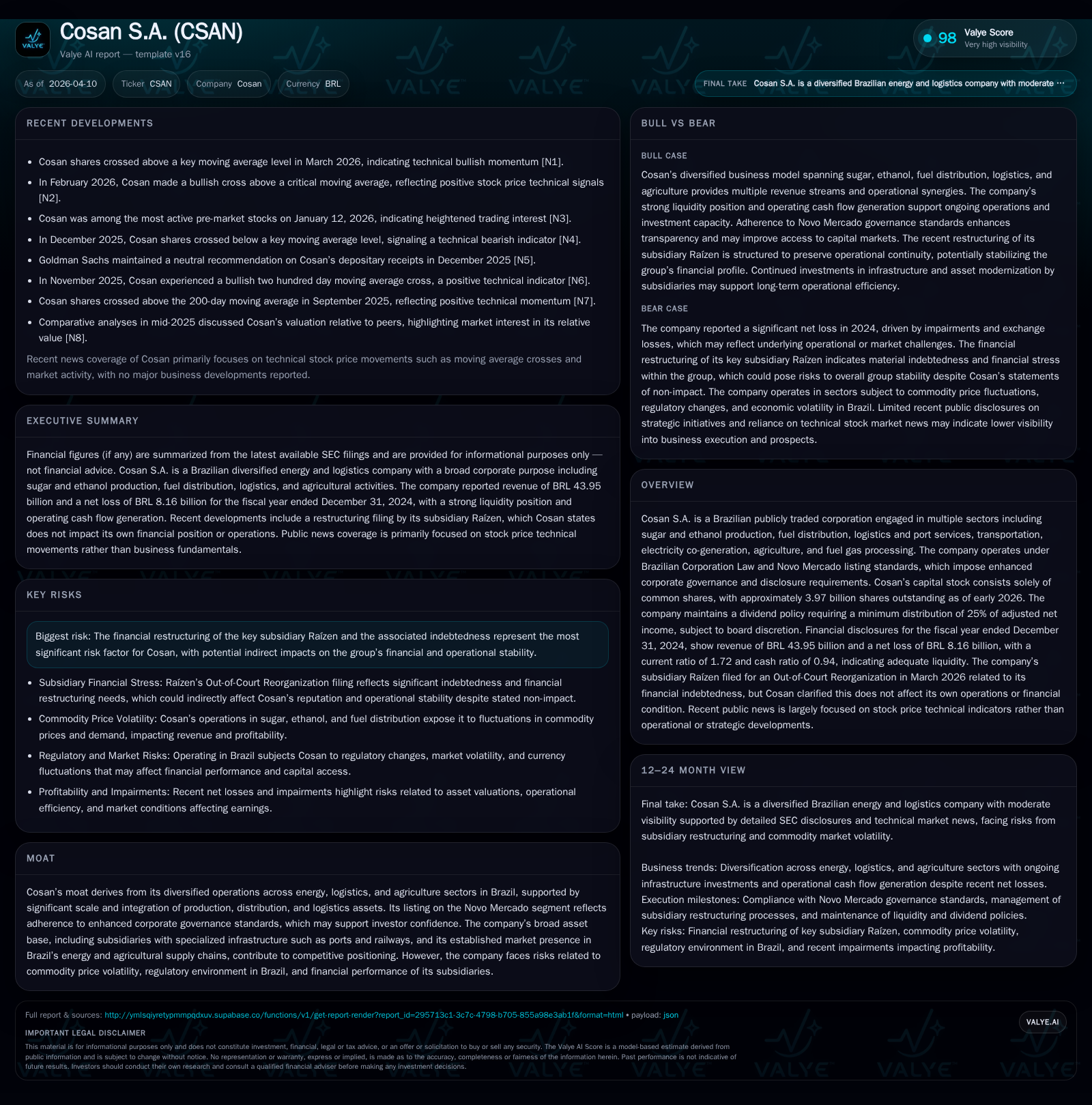

Cosan S.A.’s Strategic Rebound: From 2024 Losses to Growth and Restructuring

Cosan moves to stabilize after 2024’s severe net losses by leveraging its diversified portfolio, executing capital structure improvements, and focusing on operational resilience across Brazil’s energy and logistics markets.

In 2024, Cosan S.A. reported robust revenue growth of 11.4% but experienced a stark net loss driven primarily by non-cash impairments and financial pressures linked to its joint venture Raízen. The company's operational segments across fuel distribution, natural gas, lubricants, logistics, and agriculture showed resilience despite macroeconomic challenges in Brazil. Early actions in 2026 include significant debt prepayments, a refinancing push through equity offerings at Compass, and governance enhancements aimed at simplifying the portfolio and bolstering financial stability. Key risks remain centered on Raízen’s ongoing debt restructuring and regulatory challenges affecting subsidiaries like Rumo. Going forward, monitoring Raízen’s plan approval progress and core EBITDA trajectories will be essential indicators of Cosan’s recovery path.

Financial Performance Inflection: Dissecting 2024 Results and Trends

In the fiscal year ended December 31, 2024, Cosan S.A. recorded consolidated revenues of BRL 43.95 billion, marking an 11.4% increase over the prior year’s BRL 39.47 billion [F1]. However, this top-line growth contrasted sharply with the net income line as the company reported a substantial loss of BRL 8.16 billion in 2024 compared to a net profit of BRL 4.88 billion in the previous year [F1]. This swing reflects non-cash impairment charges, foreign exchange volatility effects on financial instruments, and significant interest expenses impacting consolidated results notably at the corporate level [S1][S14].

Gross profit remained resilient above BRL13 billion but was offset by elevated costs in some segments alongside high financial charges related to legacy indebtedness.

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2024 | 44.0 | -8.2 | +11.4% | -267.1% |

| 2023 | 39.5 | 4.9 | -0.7% | +73.2% |

| 2022 | 39.7 | 2.8 | +53.6% | -57.9% |

| 2021 | 25.9 | 6.7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($bn) | ROE% |

|---|---|---|

| 2024 | 1.2 | -20.7 |

| 2023 | 1.2 | 9.6 |

| 2022 | 1.2 | 5.9 |

| 2021 | 2.0 | 23.2 |

Source: SEC companyfacts cache [F1].

Note: ROE approximated as net income divided by equity per fiscal year; dividends paid reflect distributions reported for respective years [F1].

Segment Dynamics Fueling Operational Resilience

Cosan operates through six key segments providing broad exposure across Brazil's energy and infrastructure sectors:

- Raízen: Joint venture active in ethanol production, sugar commercialization, bioenergy including solar and biogas projects, electric power resale, fossil fuel trading via Shell-branded stations across Brazil and Latin America [S1]. Despite its integrated value chain advantages, Raízen faces financial stress leading to debt restructuring.

- Compass: Distributor of piped natural gas serving industrial, residential, commercial, automotive clients primarily in South, Southeast and Midwest Brazil; ongoing network expansion investments support demand growth [S1][S4].

- Moove: Producer and distributor of lubricants under Mobil brand plus proprietary lines across ten countries spanning South America, North America and Europe; cost reductions partially offset volume declines affected by currency fluctuations abroad [S1][S14].

- Rumo: Rail logistics operator focusing on grain and sugar transport with warehousing and port facilities; investment continues in locomotive fleet renewal and infrastructure expansions amid regulatory tax disputes [S1][S10][S14].

- Radar: Agricultural property management investing in high-appreciation farmland assets incorporating technological upgrades such as irrigation systems enhancing yields [S1][S14].

- Cosan Corporate: Corporate structure incurring administrative costs plus managing corporate finance activities including holdings in climate tech funds influencing consolidated results significantly given scale [S1].

This diversified portfolio provides operational balance mitigating sector-specific volatility inherent in commodities and infrastructure.

Raízen Debt Restructuring: A Pivotal Milestone

In March 2026, Raízen initiated an out-of-court reorganization filing addressing approximately BRL65.1 billion of unsecured financial indebtedness plus intercompany claims with creditor support exceeding the requisite threshold for proceeding submission [N2][S2]. The plan contemplates capital contributions by shareholders, conversion of debt into equity stakes potentially diluting current interests, replacement of certain debts with new instruments, corporate reorganizations segmenting business lines within Raízen group, and asset divestments.

This restructuring is strictly financial with no disruption to operational contracts or business continuity commitments maintained by Raízen; the impact on Cosan is limited to equity method accounting adjustments pending final plan ratification within a court-mandated timeframe of up to ninety days from filing acceptance [N2][S2].

Management affirms that Cosan’s standalone credit profile remains soundly insulated from Raízen’s financial restructuring except for deferred equity earnings uncertainties until resolution completion.

Operating Environment & Business Outlook

Brazil’s macroeconomic context during this period featured moderate GDP growth (1.8%) paired with controlled inflation (4%), presenting a mixed backdrop:

- Energy Distribution (Compass): Expansion capex continues alongside customer migration toward free market contracts which modify revenue profiles but enhance cost pass-through flexibility under regulated tariffs [S14][S15].

- Fuel Marketing & Bioenergy (Raízen): Commodity price volatility impacts ethanol margins despite integrated sourcing capabilities; renewable energy initiatives support longer-term outlook.

- Logistics (Rumo): Ongoing administrative proceedings related to concession contract compliance add regulatory risk; investments focus on asset modernization supporting agricultural export logistics criticality [S10][S14].

- Agriculture Assets (Radar): Value appreciation potential driven by farmland productivity gains offsets cyclical farming risks affecting real estate transaction volumes.

Navigating tariff frameworks alongside environmental regulations requires active legal defense while capitalizing on public-private partnership opportunities remains central for transport/logistics competitiveness.

Liquidity & Capital Structure Highlights

As of December 31, 2025:

- Current assets totaled approximately BRL30.77 billion versus current liabilities near BRL17.91 billion yielding a current ratio around 1.72, indicating solid short-term liquidity coverage [F1].

- Cash and equivalents increased substantially to about BRL30 billion from roughly BRL17 billion the prior year reflecting equity raises exceeding BRL10 billion completed late-2025 along with improved operating cash flows [F1][S6][S13].

- Total consolidated gross debt was managed around BRL64 billion excluding lease liabilities, slightly reduced from prior periods due to proactive redemptions including early-2026 senior note repurchases originally maturing through mid-decade horizons [S5][S11][S13].

- Interest rates on borrowings include inflation-indexed bonds paying IPCA-based yields over double-digit percentages amid Brazil's elevated benchmark rates near mid-teens annual levels plus CDI-linked loans bearing single-digit spreads over interbank rates reflecting monetary policy conditions [S5][S8].

Ongoing deleveraging reduces refinancing risk though foreign currency exposure remains a consideration given approximately one-third of debt denominated in USD.

Capital Allocation: Dividends & Shareholder Returns

Cosan’s dividend policy requires distributing at least 25% of adjusted net income, subject to board discretion especially if solvency concerns or accumulated losses prevail limiting payments under Brazilian law ([S7]). Adjusted net income excludes non-recurring impairments or unrealized FX impacts focusing on recurring profitability.

Historically dividends paid have been consistent near BRL1.24 billion annually during positive earnings years with reductions aligned to permissible adjustments during loss periods such as post-2024 results release intervals [F1][S12]. No material share repurchase activity is documented recently.

This approach balances shareholder returns against capital preservation needs amid leverage reduction efforts.

Governance Enhancements & Portfolio Simplification Initiatives

During early-to-mid-2026 management undertook organizational simplification aimed at reducing complexity while enhancing transparency targeting strategic investors aligned with long-term governance standards per Novo Mercado listing requirements ([S3]). These reforms include expanded board independence improving oversight critical for navigating regulatory environments across energy concessions and rail franchises.

New strategic shareholder entries through capital injections support credit profile stabilization while enabling potential asset sales or spin-offs focused on higher-margin businesses enhancing shareholder value.

Key Risks & Regulatory Challenges

Major risks include:

- Execution uncertainty regarding Raízen’s restructuring plan which could affect future dividend streams recognized under equity method accounting ([N2]).

- Tax litigation primarily involving Rumo related to ICMS tax credits disputes and fines linked to REPORTO program application impacting contingent liabilities assessed mainly as possible losses requiring active defense ([S10]).

- Environmental criminal investigations across multiple states targeting various subsidiaries for alleged pollution or contamination offenses posing reputational risk though penalties remain uncertain ([S10]).

Proactive legal strategies remain essential for safeguarding concession rights crucial for stable revenues.

What To Watch In Coming Periods

Key metrics shaping Cosan’s trajectory include:

- Progress toward court ratification of Raízen’s out-of-court restructuring plan within mandated timelines defining consolidated earnings impact realization schedules [N2].

- EBITDA recovery trends particularly at Compass benefiting from tariff adjustments and customer mix shifts stabilizing margins ([N1],[S14]).

- Resolution progress on Rumo’s administrative concession proceedings alongside volume stability tied to agricultural export cycles providing insights into asset productivity ([S10]).

- Success of additional capital raises such as Compass secondary offering supporting further leverage reduction initiatives ([N2],[S2]). Monitoring technical stock indicators may complement fundamental analysis but should be weighed cautiously against core financial performance developments ([N1]).

This analysis synthesizes information from SEC filings and public disclosures without speculative forecasts beyond cited sources.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments