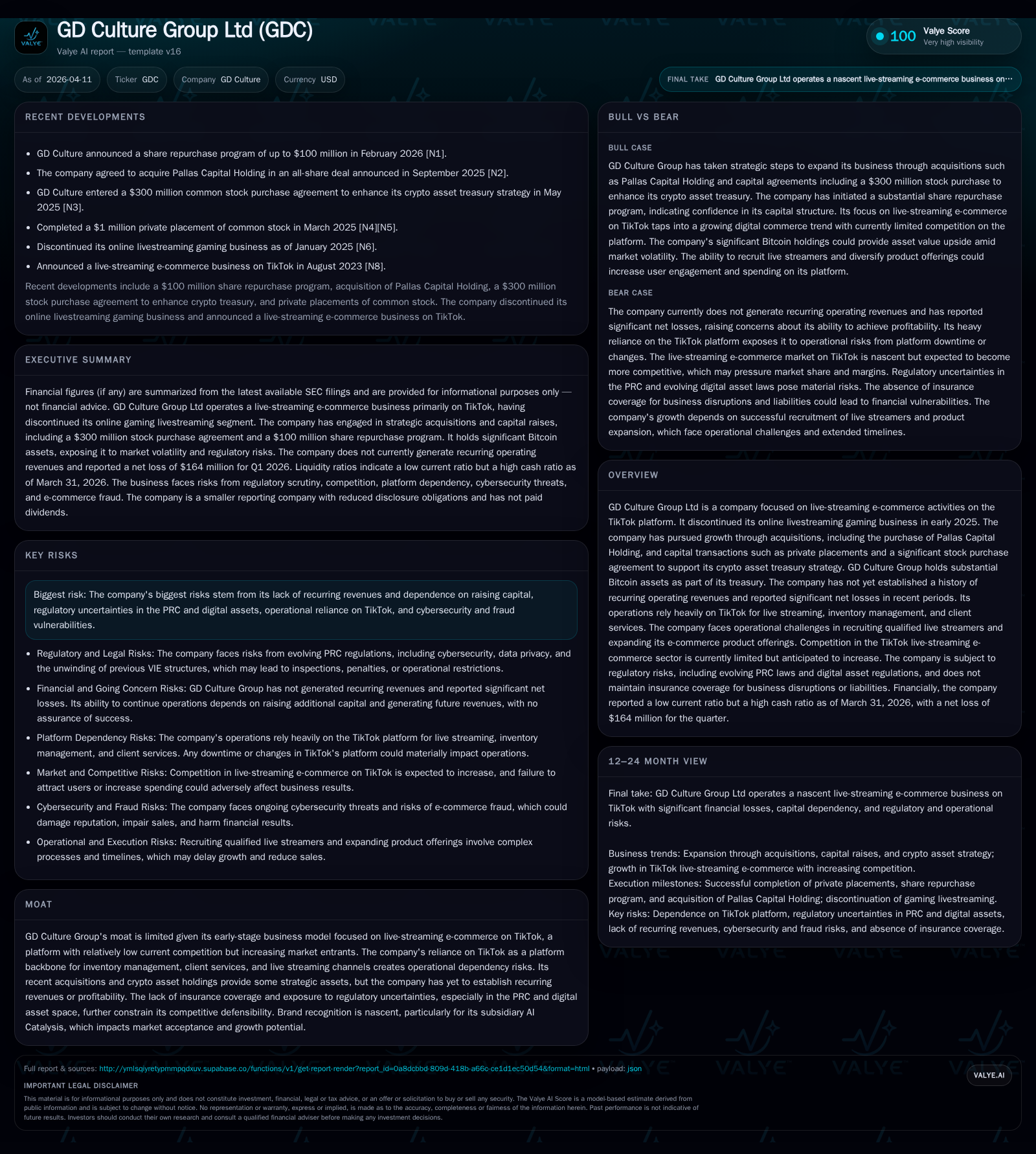

GD Culture Group’s Financial Decline and Strategic Focus on TikTok Livestream E-Commerce

An in-depth review of GD Culture Group’s financial challenges, operational pivots to TikTok-based livestream commerce, and capital structure dynamics.

GD Culture Group Ltd has experienced a steep decline in revenues and escalating losses following its strategic exit from the livestream gaming business. The company’s current model centers on TikTok live-streaming e-commerce, emphasizing collaborations with key opinion leaders (KOLs) to drive sales. Growth initiatives include acquisitions like Pallas Capital Holding and expanding crypto treasury holdings, though liquidity remains constrained with a very low current ratio and persistent negative cash flows. Regulatory complexities related to PRC operations and evolving digital asset policies add to operational risks.

Historical Financial Performance

GD Culture Group Ltd’s financial data from fiscal years 2019 through 2025 shows a sharp decline in revenue and worsening profitability. Revenue peaked at approximately $25 million in FY2021 before collapsing by 99.4% year-over-year to $153,304 in FY2022 [F1]. Operating income trends similarly deteriorated, with losses increasing from $423K in FY2022 to $8.46 million by FY2025 [F1]. Net losses expanded dramatically, reaching over $186 million in FY2025, underscoring substantial equity erosion [F1]. Operating cash flow remained negative throughout this period, totaling nearly -$6.8 million in FY2025 [F1]. Capital expenditures fell sharply after FY2021 levels of about $309K, dropping more than 95% by FY2024 [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -187 | -7 | -8 | -1250.6% |

| 2024 | -14 | -6 | -14 | -10.5% |

| 2023 | -13 | -13 | -12 | +59.4% |

| 2022 | -31 | -1 | 0 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -28.0 |

| 2024 | 4911.5 |

| 2023 | -150.0 |

| 2022 | -889.0 |

Source: SEC companyfacts cache [F1].

Note: Revenue YoY % shown only where available; later years omit revenue due to lack of disclosure [F1].

Business Model Pivot: TikTok Livestream E-Commerce

After discontinuing its livestream gaming segment early in 2025 [S3], GD Culture Group redirected efforts toward TikTok-based live-streaming e-commerce. This model leverages influencer-driven sales via Key Opinion Leaders (KOLs), who engage audiences through frequent streaming sessions to promote products directly.

Operations are deeply integrated within TikTok’s platform ecosystem for inventory management and client services—offering streamlined fulfillment but also creating reliance on platform stability [S18]. The company aims to expand its product catalog to increase average order values and user engagement metrics; however brand recognition challenges persist particularly for subsidiaries like AI Catalysis [S15].

Growth Strategy: Acquisitions and Capital Raises

Recent acquisitions such as Pallas Capital Holding aim to bolster scale and capabilities within GDC’s ecommerce livestream framework [S3]. While these moves support growth ambitions, they also introduce integration risks and may amplify near-term financial pressures given existing operating losses.

Capital raises through private placements underpin operational funding needs and investment strategies but must be balanced against liquidity constraints detailed below [S6][S8].

Treasury Management: Cryptocurrency Exposure

GDC holds notable Bitcoin assets acquired via private placements as part of its treasury diversification strategy [S6][S19]. While this provides potential upside exposure outside traditional assets, it subjects the company to significant price volatility and regulatory uncertainty—particularly under evolving PRC digital asset policies which could restrict monetization or transferability.

No explicit gains or losses on cryptocurrency holdings are disclosed; however the associated balance sheet volatility risk is material given the company’s capital position.

Operational Challenges: Live Streamer Recruitment

Recruiting qualified live streamers is an ongoing challenge amid intense competition within the TikTok ecosystem [S18]. Top-tier streamers command premium compensation while mid-tier talent development remains difficult yet critical for maintaining content cadence and viewer engagement—a core driver of ecommerce conversion rates.

Regulatory Environment and Platform Risk

GDC operates under complex regulatory regimes involving PRC cybersecurity laws and foreign listing regulations such as the HFCAA that affect auditing access and listing compliance [S4][S5][S7][S13]. The removal of prior VIE structures increases direct exposure to PRC legal frameworks governing outbound dividends and capital flows [S11][S16]. Mandatory statutory reserves further limit dividend distributions from PRC subsidiaries [S1].

Heavy dependence on TikTok’s platform for core functions creates operational concentration risk; any disruptions or policy changes by TikTok could materially impact business continuity [S18].

Liquidity Profile and Capital Allocation

As of Q1 2026, GDC's liquidity is severely constrained with current assets of approximately $206K against current liabilities near $1.9 million—yielding a current ratio around 0.11 [F1]. Cash & equivalents stood at roughly $16.8K.

Persistent negative free cash flow results primarily from operating cash flow deficits exceeding $6 million annually net of minimal capital expenditures [F1]. No dividends or share repurchases have been declared given limited distributable earnings or free cash flow availability [F1][S6].

Funding relies heavily on external equity raises via private placements or stock purchase agreements necessary for operational continuity and investment pursuits including cryptocurrency holdings [S6].

Outlook Considerations

While explicit forward guidance is not provided in filings or public disclosures, key performance indicators warrant monitoring:

- Expansion of product catalog breadth,

- Increased livestream frequency with enhanced KOL collaboration,

- User engagement metrics such as retention rates,

- Stabilization of recurring revenues,

- Improvements in cash flow generation,

- Potential monetization or refinancing of cryptocurrency assets.

Progress along these dimensions will be critical for GDC’s transition from early-stage experimentation toward sustainable operations.

Key Risks Summary

Regulatory unpredictability remains significant including cybersecurity reviews by PRC authorities that could disrupt operations or restrict capital flows [S4][S7][S16]. Market competition intensifies with stronger entrants challenging GDC’s emerging brand presence especially around AI Catalysis [S15][S18]. Cybersecurity threats pose ongoing risks given reliance on cloud infrastructure vulnerable to intrusion attempts with potential legal liabilities and reputational damage [S4][S22][S23][S24][S25]. Employee misconduct risks related to marketing practices may also expose the company to litigation or reputational harm [S20].

Disclaimer:

This analysis synthesizes publicly available information up to April 2026 without providing investment advice or recommendations. Readers should conduct comprehensive due diligence including monitoring developments beyond those discussed herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments