Childrens Place Faces Margin Pressures and Leverage Challenges With Omni-Channel Pivot

This report analyzes Childrens Place’s recent financial losses and debt pressures alongside its brand-driven omni-channel growth potential.

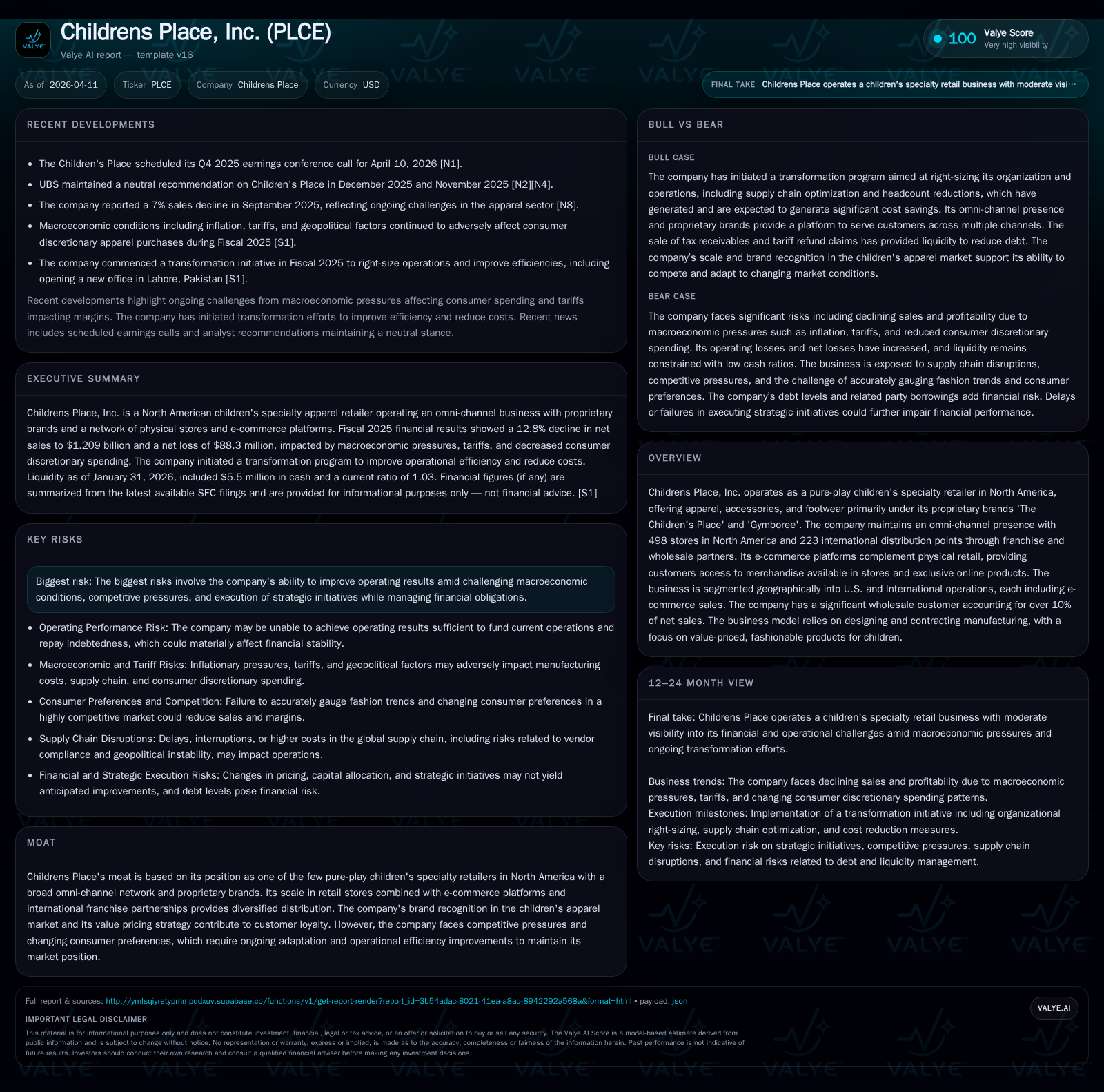

Childrens Place has experienced steep declines in profitability, culminating in an operating loss of $57.2 million in FY2025, driven by margin pressures and competitive headwinds. Despite these challenges, its omni-channel footprint—comprising nearly 500 North American stores, a growing e-commerce presence, and international franchise partnerships—supports avenues for recovery. The company’s leverage remains elevated, with $131 million outstanding on its asset-based revolving loan and a recently added $100 million term loan, constraining capital returns despite improved operating cash flow. Watching execution on inventory management, margin expansion, and debt compliance will be critical to assessing turnaround progress.

Financial Trajectory: Revenue and Profit Dynamics Over Recent Years

Childrens Place’s financial performance trended downward notably over the past several years culminating in its most recent fiscal year (FY2025). Revenue declined by 11.2% year-over-year to $321.6 million as top-line contraction weighed on profitability [F1]. Operating losses widened precipitously from a negative $13.7 million in FY2024 to a deficit exceeding $57.2 million in FY2025—a deterioration exceeding 300% that underscores substantial margin pressure facing the company [F1]. Net income mirrored this decline with losses deepening to $88.3 million, marking a roughly 53% downturn year-over-year [F1].

Operating cash flow displayed a more favorable trend rebounding from a negative cash outflow of nearly $118 million in FY2024 to a positive inflow of $8.1 million in FY2025, indicating improving operational cash generation amid leaner working capital management [F1]. However, capital expenditures rose modestly from $15.8 million to approximately $17.4 million during this period, resulting in continued negative free cash flow that reflects ongoing investment needs despite strained margins [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | -88 | 8 | -57 | -52.7% | ||

| 2024 | -58 | -118 | -14 | |||

| 2023 | 322 | -11.2% | ||||

| 2022 | 362 | -1 | -8 | -2 | -35.1% | -100.6% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | -9 | 162.9 |

| 2024 | 1 | -133 | 97.3 |

| 2023 | |||

| 2022 | 95 | -54 | -0.7 |

Source: SEC companyfacts cache [F1].

Table: Historical Financial Performance Summary; latest revenue data lags operating income/net income figures for fiscal alignment.

Gross margin pressures have been intensified by higher tariffs (+140 bps), markdowns (+70 bps), and elevated input costs partially offset by targeted cost savings measures impacting overall profitability negatively through Fiscal 2025 [S25]. This dynamic reflects typical scale challenges for specialty apparel retailers grappling with fixed cost absorption amidst reduced sales volumes.

Evolving Consumer Preferences and Omni-Channel Execution

Childrens Place distinguishes itself as one of North America's few pure-play children's specialty apparel retailers, blending physical retail with digital channels under its proprietary "The Children's Place" and "Gymboree" brands [S4][N1]. Its omni-channel footprint comprises 498 North American stores coupled with e-commerce platforms www.childrensplace.com and www.gymboree.com which offer both store merchandise and online exclusives.

On the international front, the company leverages partnerships with nine franchisees supporting distribution at 223 points across 12 countries—providing diversified revenue streams beyond domestic markets [S4]. These channels collectively support customer access but require precise inventory allocation strategies including SKU rationalization and merchandising agility to swiftly respond to shifting consumer preferences evident in children's fashion cycles and discretionary spending patterns influenced by inflationary headwinds [N1][S9].

Operational adjustments undertaken include right-sizing offices globally—for example opening an efficiency center in Lahore, Pakistan—and enhancing cross-functional collaboration intended to streamline design to distribution lifecycles while optimizing assortment breadth for balanced fashion-basic mixes responsive to demand fluctuations [S9][N1]. Digital merchandising efforts aim to boost average unit retail (AUR) through curated online collections without accumulating excessive working capital burdens.

Balancing Growth Ambitions With Operational Constraints

Management highlights macroeconomic challenges including persistent inflation impacting discretionary purchases alongside ongoing supply chain vulnerabilities stemming from offshore manufacturing reliance predominantly concentrated outside stable political regions [S1][N1]. These externalities pose execution risks for simultaneously maintaining competitive price-value propositions while pursuing operational cost efficiencies.

Strategic initiatives introduced during Fiscal 2025 focus on sales uplift through enhanced product appeal supported by continuous improvements in sourcing efficiency and supply chain reliability including supplier diversification and value engineering practices tailored to mitigate tariff impact without sacrificing quality [S25][N1]. Implementation cadence remains crucial given the delicate balance between markdown rates necessary for inventory turnover versus gross margin preservation.

Debt Profile, Covenant Nuances, and Liquidity Considerations

The company's capital structure features a principal asset-based revolving loan facility (ABL Credit Facility) sized at $350 million under Wells Fargo administration complemented by a newly established SLR Term Loan totaling $100 million initiated December 16, 2025 aimed at refinancing prior borrowings [S5][S6][S24]. As of January 31, 2026, outstanding borrowings under the ABL stood at $131 million down substantially from prior year usage of $246 million reflecting deleveraging progress albeit from elevated levels [F1][S5]. The SLR Term Loan similarly bears an effective interest rate near 8.9%, incrementally raising financing costs relative to historical averages [S6].

Total liquidity was about $89.9 million comprising approximately $44.4 million available capacity under ABL terms plus unused availability on Mithaq Credit Facility alongside cash reserves close to $5.5 million providing moderate cushion for working capital needs amidst restructuring efforts [S12][F1]. Covenant restrictions tied to excess availability thresholds—set at no less than $35 million—restrict discretionary actions such as share repurchases or dividend payments unless stringent conditions are met—a factor complicating shareholder return strategies until leverage normalizes further [S8][S10].[ note: absence of dividends or repurchases reflects covenant limitations ]

Shareholder Returns: Dividends, Buybacks, and Return on Equity Trends

Dividends were nominally resumed only in FY2024 ($1.69 million paid) after a multiyear hiatus but were absent again in FY2025 corresponding with elevated losses limiting capital return ability from underlying operations [F1][S17]. Share repurchases have been minimal—less than half a million dollars executed mainly via stock award tax withholding mechanisms rather than open market buys signaling prudence under capital constraints [F1][S27].

Equity turned negative as of January 31, 2026 (-$54.2 million), driven by cumulative net losses significantly eroding shareholder value over recent years making conventional return metrics like ROE difficult to interpret reliably though an equated figure exceeds +160% numerically due to denominator effects (/) which is misleading amid distress dynamics [F1]. This scenario echoes broad sector cyclicality observed among lifestyle specialty retailers contending with volatile consumer sentiment amidst economic uncertainty.

Key Milestones to Monitor in Strategic Turnaround

Critical near-term milestones include quarterly earnings releases such as the Q4 FY25 conference call held April 10, 2026 where management will likely provide updated commentary on comparable store sales trajectories reflecting core retail health alongside incremental details around margin improvement initiatives underway [N1][S3]. Monitoring inventory turnover rates post-SKU rationalization efforts will indicate effectiveness of assortment optimization measures. Other focal points comprise status updates surrounding international expansion via franchise partners which can accelerate top-line diversification if executed efficiently without diluting margins further given cost structures overseas [S2][S4]. Progress on debt reduction metrics including maintenance of excess borrowing availability above covenant floors will signal sustained liquidity stability needed for operational flexibility.

Investing in Design, Sourcing Efficiency, and Supply Chain Resilience

Product design coupled with contract manufacturing remains central competency supporting Childrens Place's value-priced focus balanced against fashion relevance critical for customer retention within competitive children’s apparel markets [S25]. Investments approximating $17M annually underpin enhancements not only in physical production capabilities but also IT infrastructure supporting digital commerce should further elevate merchandising precision leveraging data analytics.

Value engineering terminology manifests internally aligning with industry practices aimed at mitigating raw material cost escalation impacts while preserving quality standards—a prudent approach given tariff-induced cost volatility noted during fiscal periods analyzed where tariff-related margin erosion exceeded +140 basis points necessitating offsetting measures [S25]. Long-term resilience will depend on retaining nimble sourcing networks diversified geographically without compromising timeliness or ethical manufacturing oversight.

This analysis is based solely on publicly disclosed financial statements and regulatory filings up to April 2026 supplemented by recent earnings call transcripts; it does not offer investment advice or forecasts beyond documented guidance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments