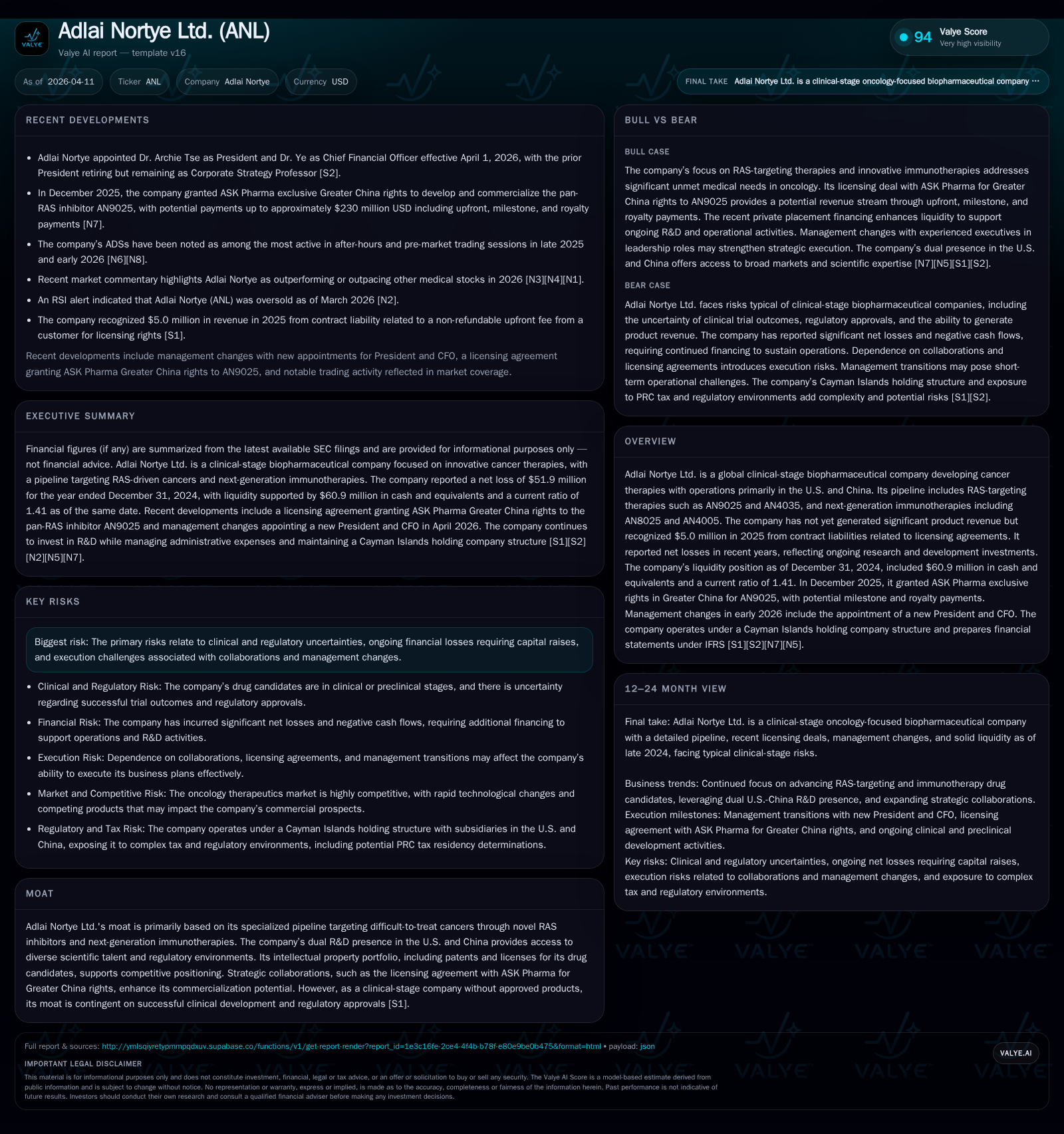

Adlai Nortye’s RAS Innovation and Strategic Shifts Reshape Clinical-Stage Trajectory

The company’s pioneering RAS-targeting pipeline combined with recent executive changes frames a critical juncture in development and financial sustainability.

Adlai Nortye Ltd., a clinical-stage biopharma focused on challenging cancer targets, has sharply reduced its losses alongside declining revenue tied to licensing shifts. Its novel drug candidates—an oral pan-RAS(ON) inhibitor, an antibody-drug conjugate targeting CEACAM5, and next-gen immunotherapies—are progressing with encouraging early clinical activity. Recent leadership appointments of industry veterans Dr. Tse and Dr. Ye signal increased operational rigor and strategic realignment. Despite meaningful cash burn from R&D investment, the firm maintains sufficient liquidity bolstered by recent collaborations and private placements. Upcoming trial readouts and partnership milestones will be pivotal against inherent clinical and regulatory risks.

From Losses to Leveraging Novel Oncology Therapies: Historical Financial Performance

Adlai Nortye Ltd. exhibits a financial trajectory emblematic of a clinical-stage biopharmaceutical company balancing innovation with capital intensity. Across the fiscal years ending December 31, historical data sourced from SEC filings ([F1], [S1], [S4], [S5]) illustrates dramatic shifts in revenue composition juxtaposed against improving profitability metrics.

Revenue plummeted by approximately 89.1% year-over-year from $45.7 million in 2023 to just $5.0 million in 2024, primarily due to discontinuation or completion of previous licensing agreements whose contract liabilities were recognized as revenue ([S1], [S10]). This sharp drop did not translate into exacerbated losses; rather, the net loss improved substantively—from a revised $109.2 million loss for FY2023 down to $51.9 million in FY2024, a roughly 50% reduction indicating tighter cost management amid strategic pivoting ([F1], [S7]).

Operating cash flow follows this pattern: cash used in operations decreased materially from $56.7 million in 2023 to $51.8 million in 2024, further easing to an estimated $33.5 million in 2025 ([S4]). This trend aligns with reduced research spend as certain programs transitioned into clinical development stages that entail different cost structures.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2024 | 5 | -52 | -89.1% | +50.5% |

| 2023 | 46 | -105 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2024 | -203.5 |

| 2023 | -132.1 |

Source: SEC companyfacts cache [F1].

Revenue reflects contract liability recognition principally; net losses show steady improvement.

Advancing the Science: Key Pipeline Assets and Development Progress

Distinctly anchored on tackling historically elusive oncogenic drivers, Adlai Nortye’s dual-pronged approach features innovative molecules targeting RAS-driven cancers alongside next-generation immunotherapies ([S1], [S3], [N3]).

- AN9025 is an oral pan-RAS(ON) inhibitor designed to inhibit active mutant RAS proteins implicated across multiple solid tumors observed with driver mutations such as KRAS G12C/V/A variants—a mechanistically pivotal step given oncogenic RAS's longstanding "undruggable" reputation.

- AN4035 utilizes antibody-drug conjugate (ADC) technology delivering potent pan-RAS inhibitors directly to tumors via CEACAM5 targeting—this approach harnesses tumor-specific surface antigens for improved payload delivery minimizing systemic toxicity.

- Immunotherapy candidates include AN8025, an αPD-L1 x CD86 variant x LAG3 variant tri-functional fusion protein aimed at enhancing T-cell activation through bispecific checkpoint pathways modulation; and AN4005, a first-in-class oral small molecule PD-L1 inhibitor designed for oral bioavailability unlike traditional monoclonal antibodies.

Milestones recently reported include successful global Phase 1 enrollment initiation for AN9025 targeting solid tumors harboring RAS mutations, signaling progression past preclinical hurdles toward human safety/efficacy evaluation ([S3], [N3]). The robust scientific foundation aims to leverage synergistic biology between pan-RAS inhibition and immune checkpoint engagement.

Management Changes Signal a Strategic Pivot in Leadership and Execution

Effective April 1, 2026, Adlai Nortye appointed Dr. Archie Tse as President while retaining his Head of Research & Development responsibilities ([S2]). Dr. Tse brings high-caliber expertise from prior senior roles at CStone Pharmaceuticals where he combined leadership over early clinical development initiatives and CMC activities, supplemented by senior roles within MSD’s global infrastructure.

Simultaneously, Dr. Ye ascended from Vice President Business Development & Commercialization Strategy to Chief Financial Officer status while maintaining focus on global commercial execution strategy ([S2]). His multidisciplinary background encompasses scientific training (Ph.D., MD Anderson Cancer Center), biotech operations leadership in Asia-Pacific markets including GenScript and Thermo Fisher Scientific subsidiaries.

These leadership changes mark a phase where scientific innovation intersects tightly with business acumen required for scaling late-stage trials, regulatory navigation, licensing partnerships, and eventual market entry—an operational maturation notable given previous relatively startup-oriented management profiles.

Capital Structure, Liquidity, and Expense Evolution Reflect Clinical Investment Priorities

Liquidity analysis reveals notable contraction in cash reserves—end-of-year cash and equivalents amounted to approximately $60.9 million at December 31, 2024, down from $91.5 million the prior year ([F1], [S4]). The current ratio stood at a healthy 1.41 indicative of near-term financial solvency supported by careful liability management.

Operating cash outflows shrank significantly consistent with trimmed R&D expenses from about $44.9 million in FY2024 down to roughly $32.8 million in FY2025 ([S5], [S9]). The decrease aligns with fewer resource-intensive late-stage clinical activities during transitioning phases; notably CRO service fees dropped concurrently along with staff compensation reflecting workforce optimization.

Capital expenditures remained conservative at approximately $0.2 million annually over the last three years reaffirming the company’s focus on preserving runways—primarily utilized for laboratory assets or IT systems required for ongoing development rather than major infrastructure expansion ([S4], [S10]).

Financially stringent governance is also evident through limited debt exposure offsetting risk but necessitating periodic equity raises supported most recently by a substantial Private Investment in Public Equity (PIPE) anticipated to generate around $140 million gross proceeds completed in early February 2026 ([S12], [S19]). Strategically these funds underpin trial expansions, infrastructure enhancement across the U.S., China and potentially Europe while cushioning operational burn ahead of potential product revenues.

Milestones on the Horizon: What to Watch in Upcoming Clinical Readouts and Regional Partnerships

Forward-looking developments center on several crucial junctures poised through 2026:

- Data readouts from ongoing Phase 1 trials of AN9025 will be vital for validating safety/tolerability profiles that historically challenge pan-RAS programs.

- Expansion or initiation of additional clinical testing under collaboration frameworks such as ASK Pharma’s exclusive Greater China license for AN9025 may trigger milestone payments up to roughly RMB1.6 billion (

US$230 million), incorporating upfronts already partially received ($8.7 million) plus royalties ([S1], [S6]). - Navigating diverse regulatory environments between U.S./FDA pathways versus China NMPA approvals dictates differentiated strategy layers complicating timing but enabling simultaneous global footprint advantages.

Note: As no explicit upcoming timelines are mandated beyond disclosures no guaranteed dates exist; monitoring announcements will be critical.

Risks Embedded in Clinical Trials, Regulatory Pathways, and Funding Requirements

Adlai Nortye confronts typical but acute risks characterizing clinical-stage oncology developers:

- Clinical trial failures or unexpected safety signals are central threats given historical attrition rates especially among novel drug classes like pan-RAS inhibitors.

- Regulatory approval uncertainties intensify due to variable standards across jurisdictions compounded by evolving policies around biomarker-driven oncology approvals.

- Persistent negative earnings compel recurrent capital raises exposing dilution risk despite PIPE success; failure to secure sufficient funding threatens project continuity ([S1], [S17]).

- Governance risks include limited shareholder protections stemming from Cayman Islands jurisdictional norms inconsistent with Nasdaq listing standards imposing less stringent independence/compliance requirements affecting oversight ([S1]).

These risks collectively underscore fragility inherent in translating promising early science into commercially viable oncology therapeutics.

Evaluating Capital Allocation: Returns, Cash Flow Trends, and Shareholder Value Implications

Reflective of its clinical develop-and-prove model without approved therapies yet commercialized, Adlai Nortye’s capital discipline prioritizes funding pipeline progression over immediate shareholder returns.

ROE remains deeply negative around -203%, derived from net income of roughly -$51.9 million against an equity base shrinking markedly post-loss absorption ($25.5 million as of end 2024) ([F1]). Absence of dividends or share repurchases is consistent with early-stage industry norms—cash flow focuses predominantly on operational expenditure including substantial share-based compensation costs impacting profit metrics ([S11], [S20], [S21]).

Analytically this financial stewardship balances between sustaining long-duration value creation bets embedded within complex oncology modalities while maintaining survival runway enabled partially through sizeable equity injections including public offerings completed since IPO inception in late-2023 ([S19]).

Disclaimer: This analysis is intended solely for informational purposes based on publicly available data as of the report date without offering investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments