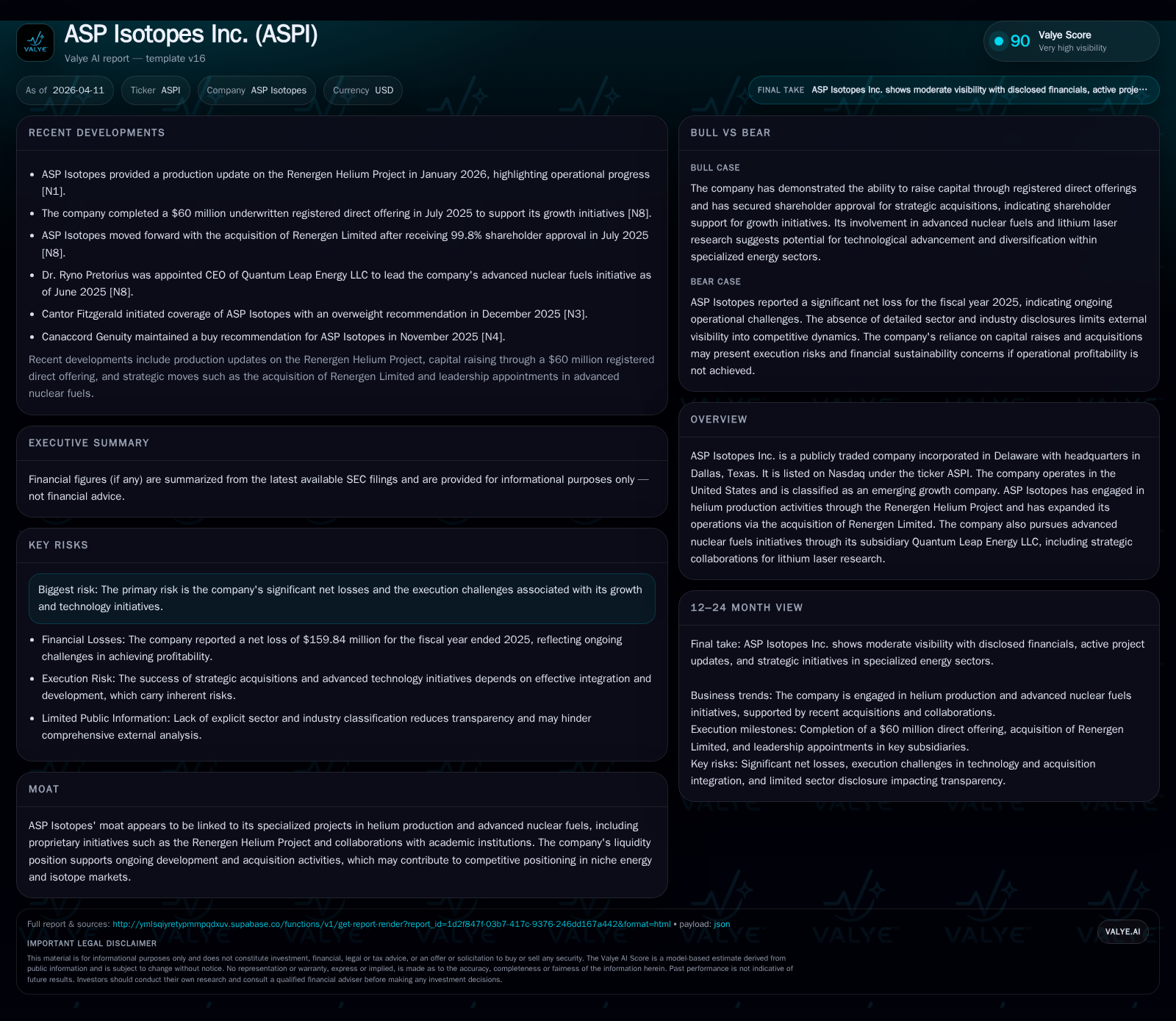

ASP Isotopes’ Transition from Innovation to Commercialization Challenges

ASP Isotopes is scaling proprietary isotope enrichment technologies toward initial commercial production while navigating capital and regulatory hurdles.

ASP Isotopes Inc. has rapidly evolved from a research-driven innovator in isotope enrichment to an emerging commercial producer, marked by a significant revenue increase to $23.8 million in 2025 alongside deepening operating losses. The company’s deployment of its proprietary Aerodynamic Separation Process and Quantum Enrichment technologies targets critical isotopes like C-14, Si-28, and Yb-176 for advanced medical, semiconductor, and quantum computing applications. While commercial shipments are set to commence mid-2026, growth remains contingent on regulatory approvals, scaling operational efficiency, and capital availability amid geopolitical risks linked especially to its South African operations. The sizable cash reserves support near-term expansion but do not eliminate the need for ongoing financing to sustain cash flow deficits.

From Pioneer to Producer: Reviewing ASP Isotopes’ Historical Growth

ASP Isotopes Inc., incorporated in Delaware with operational headquarters in Dallas but significant production facilities in Pretoria, South Africa, has been transitioning from an innovation-focused firm toward early-stage commercialization of advanced isotope enrichment technologies. The company’s fiscal 2025 results underscore a rapid expansion trajectory on the top line coupled with mounting operating losses typical of capital-intensive tech ventures entering production.

Revenue surged to $23.85 million in FY2025 from just $4.14 million a year earlier — approximately a 475% increase — signaling initial commercial sales primarily from the newly commissioned Aerodynamic Separation Process (ASP) plants able to enrich critical isotopes such as Carbon-14 (C-14) and Silicon-28 (Si-28) [F1]. Despite this promising revenue inflection, ASP's operating income deteriorated further into the red at -$59.9 million (versus -$26.4 million in FY2024), reflecting extensive costs associated with scaling manufacturing capacity and ongoing R&D investment [F1]. Net losses widened dramatically as well, reaching nearly -$159.8 million on a largely pre-commercial basis.

Operating cash flows continued negative trends at -$37.78 million as the company expended substantial capital outlays ($9.65 million in FY2025) focused on facility expansions and technology development initiatives that underpin its future pipeline [F1]. These figures paint a portrait of a company actively converting proprietary technology into production throughput while absorbing upfront scale-up expense burdens common among emerging advanced materials firms.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 24 | -160 | -38 | -60 | +475.5% | -393.0% |

| 2024 | 4 | -32 | -17 | -26 | +857.0% | -99.0% |

| 2023 | 0 | -16 | -5 | -16 | -229.5% | |

| 2022 | -5 | -3 | -5 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 0 | -47 | -78.3 |

| 2024 | 3 | -26 | -67.7 |

| 2023 | -8 | -100.0 | |

| 2022 | -7 | -50.4 |

Source: SEC companyfacts cache [F1].

The data illustrates a startup-phase enterprise where top-line scaling is nascent amid steep incremental costs.

Pathway to Market: Commercialization Timelines and Technology Focus

Central to ASP Isotopes' commercialization strategy are its two core enrichment technologies: the Aerodynamic Separation Process (ASP technology) and Quantum Enrichment (QE technology). Both are proprietary isotope separation platforms designed for producing highly enriched materials tailored to niche applications across nuclear medicine, semiconductor fabrication, quantum computing, and potentially nuclear energy sectors.

ASP’s first two operational plants located in Pretoria have begun commercial production during H1 2025—one focusing on lighter isotopes like C-14 used extensively in pharmaceutical tracer studies and agrochemical development; the second larger facility targeting kilogram-scale enrichment of heavier isotopes such as Si-28 important for next-generation semiconductor substrates and quantum device architectures [S1].

The QE platform employs laser-based enrichment techniques enabling extraction of ultra-high purity Ytterbium-176 (Yb-176), which bears potential utility in novel radiotherapeutics for oncology treatment modalities [S1]. The company targets first commercial shipments for these isotopes during mid-to-late calendar year 2026.

Longer term aspirations include expanding both ASP and QE technologies into additional isotope separations relevant for healthcare (e.g., Zinc-68), semiconductor materials (Germanium isotopes), nuclear medicine (Xenon isotopes), and even nuclear fuel cycles with Uranium-235 enrichment aimed at supporting next-gen small modular reactor designs fueled by high-assay low-enriched uranium (HALEU). Recent strategic collaborations underscore advancement efforts beyond pure isotope extraction [S1], [S14].

Critical Growth Drivers and Operational Constraints

ASP Isotopes’ growth hinges on successfully scaling its dual-use isotope separation processes that face complex regulatory scrutiny given their potential military applications if applied toward weapons-grade material production. Regulatory oversight governs export controls and disclosure limitations that could constrain business opportunities outside tightly controlled markets [S1].

Further operational risk stems from customer concentration: early revenues rely heavily on a limited set of large contracts within specialty pharma/agrochemical sectors or semiconductor manufacturers willing to adopt enriched substrates produced by new technologies involving aerodynamic separation steps that remain non-mainstream currently.

Geopolitical factors specifically tied to South African operations introduce additional complications related to local legislative uncertainty affecting exploration rights and industrial permits necessary for ongoing helium production via the acquired Renergen asset base — itself integral to providing natural gas and liquid helium supplies critical for certain industrial processes allied with isotope handling [S1]. Socio-political disruptions could negatively impact project timelines or cost structures.

Intellectual property protection is also not entirely based on patents; some proprietary processes lack patent coverage leaving technology susceptible to replication amidst competitive dynamics unless adequately guarded through trade secrets or contractual exclusivities.

Capital Structure, Liquidity Trends, and Funding Needs

The company maintains strong liquidity with approximately $285.6 million cash & equivalents at year-end FY2025 against current liabilities under $33 million yielding a robust current ratio surpassing 12x—a significant buffer for near-term obligations reflecting multiple financings designed explicitly to fund aggressive plant builds and R&D expansion efforts [F1], , .

Several consecutive SEC Form 8-K disclosures throughout early 2026 recounted capital structure updates emphasizing equity raises rather than debt issuance given the firm’s growth stage status as an emerging growth company preferring capital preservation while scale-up proceeds without immediate positive cash flow contributions , .

Notwithstanding these strengths in liquidity headroom today, sustained negative free cash flow exceeding $47 million per annum combined with no operational profitability necessitates vigilant monitoring of future financing access conditions.

Evaluating Profitability and Cash Flow Dynamics

ROE calculation derived from annual net loss relative to equity results in roughly -78%, characteristic of double-digit percentage net losses overshadowing shareholder equity accumulation via retained deficit carry forwards during rapid growth phases [F1]. There is clearly acute pressure on profitability metrics reflective of upstream R&D intensity coupled with downstream commercialization overheads.

Operating cash flow remained persistently negative (-$37.78M FY2025) underscoring ongoing heavy investment demands particularly linked with commissioning new plants along with personnel expansions required for technical process optimization functions inherent in aerodynamic separation setups or precise laser enrichment methodologies intrinsic to QE operations.

Free cash flow exhibits similar negative patterns after deducting capex (~$9.65M), emphasizing that positive earnings leverage has yet to be realized despite initial revenue inflows indicating overall business still resides predominantly “pre-profit” cycle stage typical among deep-tech material suppliers attempting market entry against incumbent isotope supply chains grounded historically on centrifuge or gaseous diffusion methods internationally.

Strategic Capital Allocation: Investments Without Payouts

Capital expenditures held steady near $9.65M across FY2024-FY2025 aimed primarily at plant buildouts rather than marginal upgrades illustrating commitment toward capacity scaling instead of maintenance spending alone; no share repurchases or dividend distributions occurred as management channels available capital almost exclusively into organic growth investments consistent with an emerging growth profile reinvesting all free resources back into novel isotope product launches or facility enhancements [F1].

This emphasis conforms with expectations given developmental nature but demands eventual transition toward disciplined capital allocation once free cash flow turns sustainably positive.

Risk Profile: Regulatory, Operational, and Litigation Considerations

Regulatory risk dominates given dual-use classification potentials affecting disclosure obligations or export control regimes applicable if any ASP/QE technologies facilitate military-grade material enrichment indirectly jeopardizing licensing frameworks or customer access internationally [S1]. Further registration clearance awaits for final marketing approval of isotopic products employed in pharmaceuticals or nuclear fuels prior commercialization discharge timelines bearing direct consequences on revenue ramp-up cadence.

South African political-economic instability presents potential interruptions when combined with evolving local mining legislation impacting Renergen assets newly folded into operations supportive mainly via helium extraction supporting industrial gas markets alongside LNG ventures limiting alternative capital deployments should disruptions occur unexpectedly.

Also noteworthy is pending securities class action litigation initiated end-2024 alleging material misstatements by company officers concerning business conditions which may draw legal expenses or distract leadership attention over medium term until resolution events occur judicially effectively scheduled through legal process milestones since mid-2025 including partial denial motions followed by certification rulings handled within federal courts jurisdictional norms potentially impacting share price volatility perceptions among public investors [S1].

Outlook: Milestones to Monitor and Potential Catalysts

Investors should observe key upcoming operational milestones comprising targeted initiation of first commercial shipments of enriched C-14 starting mid-2026 with sequential delivery buildup thereafter planned simultaneously from Si-28 product lines scheduled around Q2/Q3 calendar year timeframe complemented by Yb-176 laser-enriched deliveries slated through latest H2 timing window backed by confirmed commissioning completion status announced recently [S1], [S3].

Additional watchpoints include progress toward establishing new enrichment plants across Icelandic geothermal-linked industrial zones leveraging clean power availability plus projected expansions within US jurisdictions favorably legislated around upcoming nuclear fuel supply chain revitalization efforts benefiting QLE subsidiary’s uranium enrichment initiatives aligned with high-assay low-enriched uranium requirements targeting small modular reactors markets expected over near decade horizon incorporating government-supported programs pushing domestic HALEU capabilities development pathways underscored through MOUs signed lately with major US energy companies advancing sustainable fuel cycles application studies highlighted publicly earlier this year under forward-looking disclaimers yet carrying substantive strategic weight [S13], [S12], [S14].

Ultimately success will hinge on effective operational scaling execution amid layered regulatory approvals intersecting with customer adoption ramp timing nuances inherent within technologically complex market entry domains characterized by high barriers but commensurately elevated value propositions enabling advanced medicine breakthroughs plus quantum-enabled microelectronics revolution paths.

Disclaimer: This report synthesizes available public disclosures including SEC filings without offering investment advice or price forecasts; it should be used solely for informational purposes respecting data grounding constraints outlined herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments