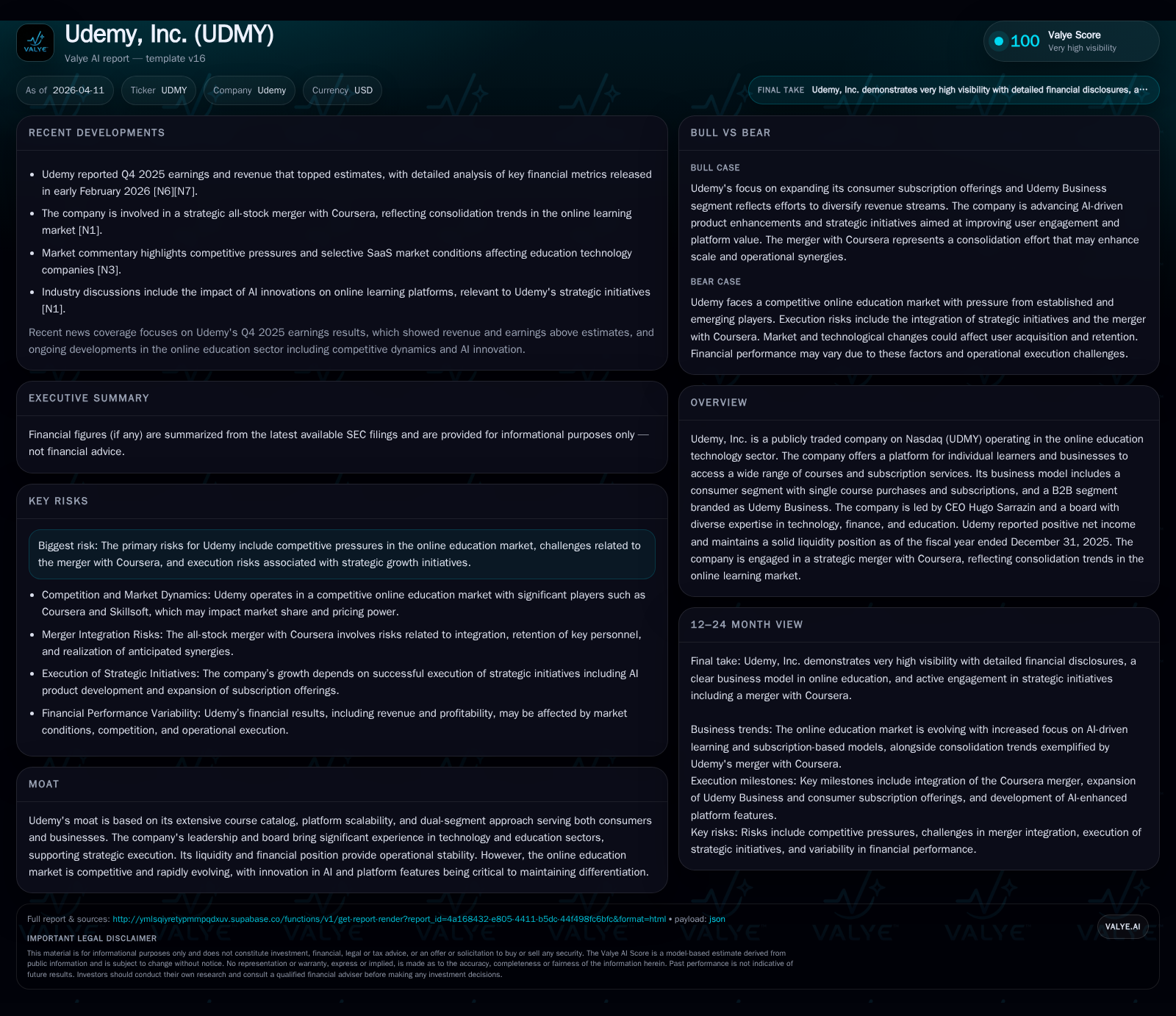

How Udemy’s Merger Strategy and Financial Recovery Set New Growth Milestones

Udemy has transitioned from steep operating losses to net profitability in 2025 while pursuing a transformative merger with Coursera.

Udemy’s fiscal year 2025 marked a pivotal financial turnaround, shifting from sustained operating losses to a positive net income aided by disciplined cash flow management and controlled capital spending. This recovery underpins the company's strategic merger with Coursera, aiming to consolidate market position amid intensifying online education competition. However, legal challenges and integration complexities pose substantial risks. Monitoring operational performance and synergy milestones post-merger will be critical to gauge sustained growth prospects.

Financial Recovery: Tracking Udemy's Shift from Losses to Profitability

Udemy entered the FY2025 period grappling with multi-year operating losses exceeding -$150 million in FY2022; however, by the end of 2025 these losses contracted dramatically to just -$4.16 million, representing a near 95.3% improvement year-over-year [F1]. More notably, the company achieved positive net income of $3.81 million in 2025, a reversal from net losses above -$85 million in the previous year — marking an absolute swing above 100% on net income [F1]. This reflects an operational discipline pivot encompassing tighter cost controls and improved revenue mix, which enhanced operating leverage.

Complementing profitability gains, Udemy’s operating cash flow surged to $87.7 million in FY2025 from $53 million in FY2024 (+65.3% YoY), underscoring stronger cash conversion efficiency amid expanding scale [F1]. Capital expenditure increased over 150% to $5.8 million — consistent with strategic investment in platform capabilities — while keeping free cash flow robust at approximately $81.9 million (CFO minus Capex) during the year [F1]. This combination signals a healthier liquidity profile supported by $231 million in cash and equivalents as of December 31, 2025 [F1], positioning Udemy well ahead of typical industry shortfalls.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 4 | 88 | -4 | 6 | +104.5% |

| 2024 | -85 | 53 | -89 | 2 | +20.5% |

| 2023 | -107 | -2 | -122 | 1 | +30.3% |

| 2022 | -154 | -61 | -151 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 51 | 82 | 1.8 |

| 2024 | 150 | 51 | -43.2 |

| 2023 | -3 | -30.1 | |

| 2022 | -63 | -45.3 |

Source: SEC companyfacts cache [F1].

Data sourced exclusively from audited SEC filings [F1]; percentage changes denote year-on-year improvements.

Business Model Dynamics: Consumer and B2B Segments Driving Change

Udemy operates on a dual-segment structure that combines an individual learner marketplace with a corporate-focused subscription product branded as Udemy Business [N1][S1]. The consumer side typically relies on transactional course purchases or access via mixed subscription offerings—key facets emblematic of the broader subscription economy that leverages platform scalability and content monetization efficiencies common in edtech.

The B2B segment diversifies revenue streams by targeting enterprise clients seeking scalable employee training solutions, thus reducing dependence on more volatile direct consumer spend patterns [N1]. This bifurcated approach enables operational flexibility; however, executing effective cross-segment synergies remains crucial especially as competitive pressures demand constant innovation both in user experience and course breadth.

Synergies and Challenges in the Coursera Merger

Entered into December 17, 2025, Udemy’s merger agreement with Coursera reflects an intent to consolidate two of the largest online learning platforms to enhance content libraries, expand global reach, and improve economies of scale [S3][S6]. Pro forma ownership post-merger is weighted approximately 43% toward Udemy shareholders, emphasizing their material equity stake within the combined entity [S8].

Yet this strategic move faces tangible headwinds: three lawsuits have been filed challenging disclosure completeness related to the merger prospectus—allegations that Udemy contests but has proactively addressed through supplemental disclosures to avoid protracted litigation delays [S7][S9]. Moreover, successful regulatory approvals remain conditional amidst scrutiny typical for sizable tech combinations.

The merger necessitates navigating integration complexity including uniting differing corporate governance frameworks; notably Coursera operates as a public benefit corporation and certified B Corp—an unusual status introducing unique operational obligations [S6][S9]. Achieving synergy realization timelines depends on alignment across cultures and technology stacks—a critical factor given sector demands for continuous innovation driven by AI-enhanced learning tools.

Capital Allocation: Buybacks, Cash Flows, and Return on Equity Analysis

In parallel with its turnaround story, Udemy executed meaningful capital return activities including share repurchases totaling approximately $51 million during FY2025—down from $150 million share buybacks executed the prior year yet indicative of sustained buyback program commitment amidst reinvestment priorities [F1][S10][S14].

Positive operating cash flows underpin this capital strategy; Udemy reported CFO exceeding $87 million alongside capex rising to nearly $6 million supporting platform evolution efforts [F1]. Equity base stood at approximately $210 million year-end 2025 yielding an implied return on equity metric near 1.8%, reflecting early-stage profitability momentum after years of losses [F1]. This modest ROE suggests room for improvement aligned with scaling margins post-merger.

Balancing share repurchases alongside significant investments serves a dual purpose: signaling confidence in long-term value creation while preserving financial flexibility amid integration phases.

Risks to Watch: Competitive Pressures, Litigation, and Integration Hurdles

Udemy navigates a crowded online education market where competitive dynamics intensify around AI-powered curriculum personalization, interactive features, and user retention strategies—a landscape demanding rapid innovation and agile product roadmaps [S4]. The pending Coursera merger exposes Udemy to execution risks encompassing integration delays or unknown costs compromising expected synergy gains.

Litigation challenging merger disclosures introduces potential cost burdens and distraction for management teams which could delay transaction close or impair stakeholder confidence if mishandled despite company assertions regarding meritless claims [S7][S9]. Regulatory approval processes themselves may introduce timing uncertainty or condition impositions altering deal economics.

Moreover, as both companies operate under high-touch enterprise sales models alongside self-service channels, disruption risks could emerge if client retention falters during transition periods—making personnel retention strategies especially critical per risk disclosures associated with combined company operations as public benefit entities mandated to balance profit with social purpose standards [S4][S6][S16].

Outlook Indicators: Guidance Signals and What They Mean for Investors

While explicit quarterly or annual earnings guidance was not prominent in recently filed reports through early April 2026 [S21], management commentary underscores emphasis on subscription revenue growth within both consumer and business channels as vital leading indicators.

Pipeline developments concerning enterprise contracts are flagged internally as performance milestones linked with synergy capture expectations post-merger close anticipated later in 2026 or early 2027 timeframe downstream from regulatory clearance [S28]. Market observers should therefore track updates around subscriber base expansion rates, client retention statistics on Udemy Business accounts, usage metrics enhanced by AI features integration—as these will gauge the merged platform’s competitive traction.

Analytically speaking, maintaining operational momentum while successfully integrating complementary assets will prove decisive for sustainable margin improvements beyond this inflection year.

Disclaimer: This analysis is based solely on publicly available data sourced primarily from recent SEC filings ([F1], [S#]) and corroborated news reports ([N#]). It does not constitute investment advice or recommendations but aims to provide an informed perspective on Udemy’s financial trajectory and strategic positioning amid its merger with Coursera.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments