Quince Therapeutics’ Post-Failure Strategy and Liquidity Challenges Signal High-Risk Outlook

After the failed NEAT trial, Quince faces escalating financial pressures and must pursue strategic alternatives amidst delisting risks.

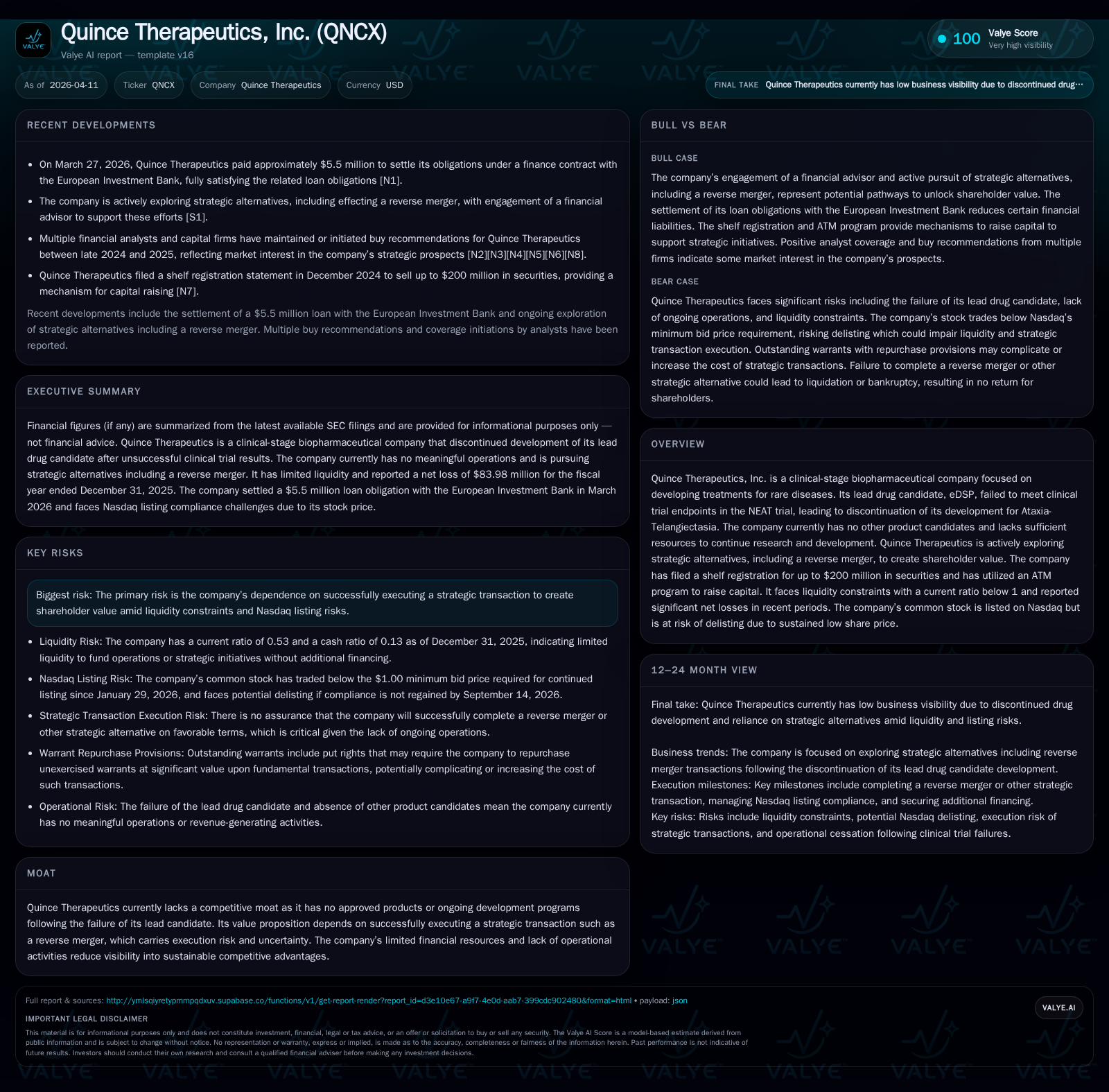

Quince Therapeutics’ clinical setback with its lead candidate eDSP terminated its development pipeline and R&D activity, severely constraining future growth prospects. The company has incurred accelerating net losses and operating cash flow deficits through 2025 while facing liquidity pressures reflected in a current ratio below 0.6. With no active product candidates, Quince is exploring strategic alternatives including a reverse merger to preserve shareholder value but execution uncertainty remains significant. Meanwhile, Nasdaq listing risks due to persistent low share price and dilution from equity raises and warrants add layers of investor risk.

Clinical Trial Setback That Altered Quince’s Trajectory

Quince Therapeutics anchored its clinical-stage promise on eDSP, a therapeutic aimed at treating Ataxia-Telangiectasia, a rare neurodegenerative disorder. The failure of eDSP to meet primary endpoints in the pivotal NEAT trial marked a watershed event. This outcome resulted not only in halting eDSP's development but also forced the cessation of broader research efforts across the pipeline. With no other product candidates advancing, the company's clinical ambitions effectively stopped.

This defeat sharply truncated Quince's historical growth trajectory, which until then depended largely on anticipated clinical milestones and eventual commercialization of its lead asset [N1][F1]. The trial failure extinguished near-term catalysts, driving down prospective value realization for shareholders.

Financial Performance Trends Highlight Deteriorating Operating Results

Examining financials from fiscal years 2022 through 2025 reveals intensifying operating losses. Operating income declined from -$52M in 2022 to -$58M in 2025, representing a modest Year-over-Year deterioration of approximately 1.4% [F1]. However, net income saw a sharper drop from a loss of -$51.7M in 2022 to -$83.9M by end-2025 — a near 48% YoY worsening driven primarily by one-time charges including restructuring and impairment related to the pipeline discontinuation.

Operating cash flow mirrored this downward trend, shrinking nearly 30% year-over-year from -$31.9M in 2024 to -$41.4M in 2025 [F1]. The consistent negative CFO reflects ongoing expenditure commitments despite the cessation of new R&D projects. Capital expenditures remain marginal (circa $350K), indicating limited reinvestment or capacity expansion.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -84 | -41 | -58 | 352000 | -47.8% |

| 2024 | -57 | -32 | -57 | 257000 | -81.1% |

| 2023 | -31 | -18 | -35 | 160000 | +39.2% |

| 2022 | -52 | -44 | -52 | 133000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -42 | 235.1 |

| 2024 | -32 | -188.5 |

| 2023 | -18 | -36.9 |

| 2022 | -44 | -51.4 |

Source: SEC companyfacts cache [F1].

Note: Negative equity in FY2025 reflects accumulated deficits surpassing book value.

Liquidity Struggles and Capital Raises: Funding the Company’s Next Moves

Liquidity metrics underscore growing operational strain: as of December 31, 2025 current assets totaled $22.9 million versus current liabilities of $43.2 million yielding a current ratio of approximately 0.53 [F1]. Such sub-1 ratios signal potential near-term funding gaps absent new capital infusion.

To bridge cash needs amid depleted internal sources post-clinical halt, Quince resorted to equity raises via an ATM program under a $200 million shelf registration filed previously [S2]. The company raised net proceeds totaling roughly $6.3 million in late 2025 via ATM issuances of common stock [N1][S2]. However, these ongoing sales imply considerable dilution — typical for clinical-stage biopharma facing setbacks — impacting shareholder equity further.

Additionally noted was an April 2026 settlement payment of $5.5 million related to loan obligations [N1], signaling attempts to reduce debt burdens which otherwise might constrain flexibility.

Strategic Alternatives: Exploring Reverse Merger and Value-Creation Paths

With dwindling resources and no active pipeline candidates post-eDSP failure, Quince announced active exploration of strategic alternatives aimed at sustaining enterprise value [N1]. A leading option is pursuing a reverse merger which could bring new control interests and fresh capital or assets into the company.

Reverse mergers can accelerate public listing liquidity but involve execution risks — including integration complexity and valuation uncertainties from a buy-side perspective. Success hinges on identifying counterparties willing to accept Quince’s distressed equity status while structuring deals that mitigate severe dilution or governance upheavals.

The approved reverse stock split (1-for-10 ratio) addresses Nasdaq minimum bid price requirements [S3], preserving listing status critical to any transaction viability.

Risks from Nasdaq Listing Status and Dilutive Financing

Nasdaq listing rule breaches remain imminent risks tied directly to low trading prices necessitating corporate actions like reverse splits [S3]. These measures preserve exchange eligibility yet may depress market enthusiasm due to perceived distress signals.

Further compounding risk is outstanding warrant overhang; exercisability threatens incremental share supply expansion if holders convert amid financing needs or opportunistic gains [S2]. Combined with ongoing equity sales under shelf registration this creates sustained dilution pressure.

Investor risk perceptions toward Quince likely incorporate these layered threats correlated with dwindling operational viability without near-term restructuring success.

Outlook: What Investors Should Monitor for Potential Milestones

Although explicit company guidance remains absent given suspended development status [N1], several key indicators warrant close attention:

- Successful closing of strategic transactions such as reverse mergers injecting capital or assets,

- Material capital infusions beyond ongoing ATM raises signaling extended operational runway,

- Announcements revisiting R&D pipelines or licensing opportunities that could revive clinical programs,

- Regulatory updates regarding Nasdaq compliance related to share price trends post-reverse split,

- Changes in leverage or debt profile following loan settlements improving financial flexibility.

Lack of progress may signal continued contraction or possible delisting.

Balance Sheet Overview and Capital Allocation Review

The balance sheet shows erosion culminating in negative book equity around -$35.7 million by end-2025 [F1], reflecting cumulative losses outpacing invested capital rather than value creation typical for mature enterprises.

Operating cash flows have been deeply negative (-$41 million in FY25) with minimal capex spend highlighting a freeze on growth investments [F1]. No dividends or buybacks are present; capital allocation focuses on sustaining corporate continuity within constrained resources.

Approximate Return on Equity calculations are skewed due to negative equity base but reflect accounting artifacts arising from massive accumulated deficits overshadowing invested capital (+235%) rather than profitability.

This indicates no returns on capital; preservation is the guiding principle pending strategic reconfiguration.

Disclaimer: This analysis is informational only and does not constitute investment advice or an endorsement of securities discussed herein. Data and disclosures are sourced solely from referenced SEC filings and credible news outlets as cited.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments