ALT5 Sigma Corp’s Bold Shift to Institutional Crypto Services Challenges Market Norms

ALT5 Sigma’s pivot from legacy operations to tailored B2B crypto fintech solutions unfolds amid steep financial headwinds and regulatory complexities.

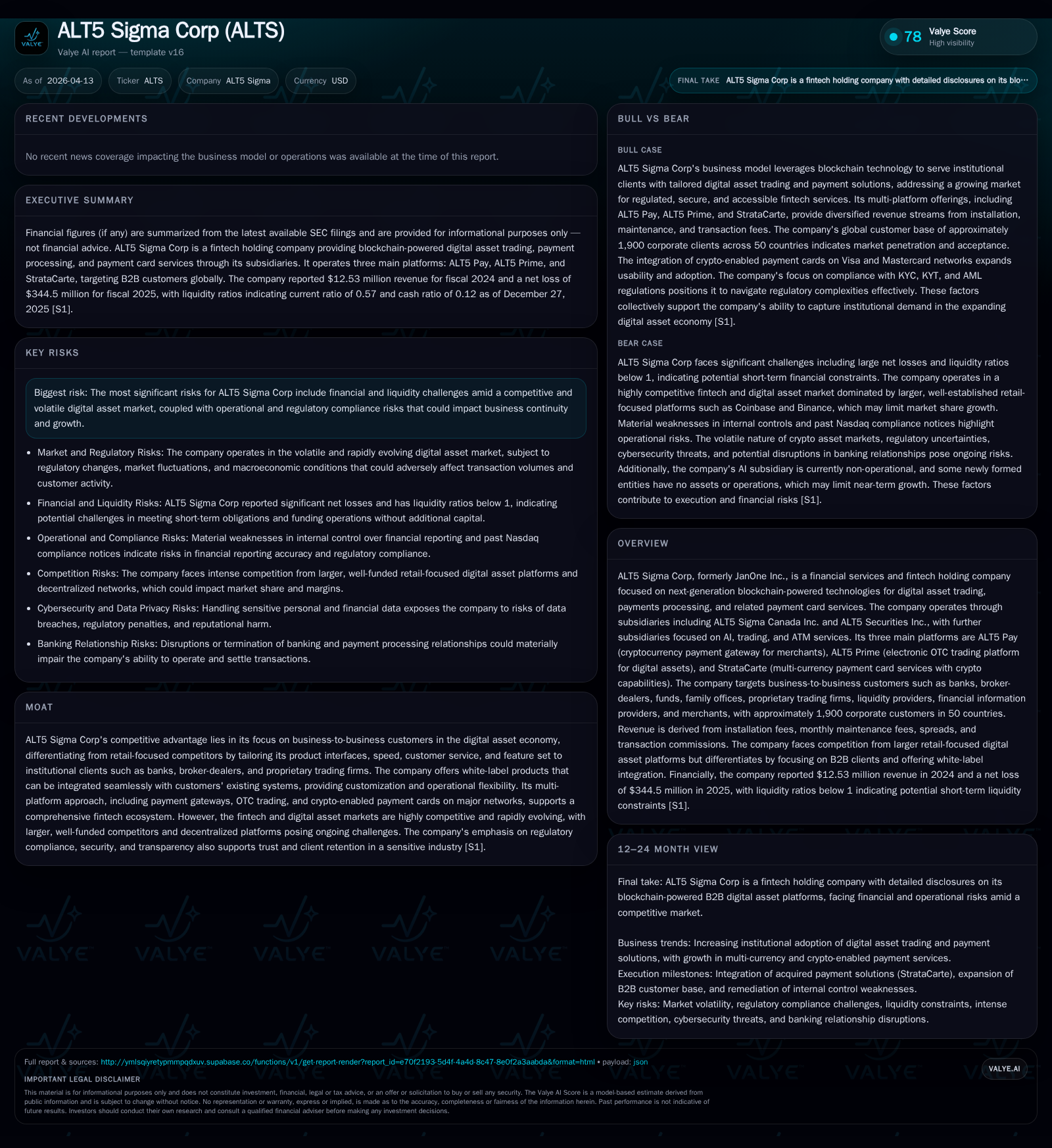

ALT5 Sigma Corp has radically transformed its business model, exiting recycled appliance operations to focus on blockchain-powered B2B trading and payment platforms. Its revenue streams have drastically contracted over recent years, compounded by soaring losses and cash flow deficits as it invests in institutional-grade fintech services like ALT5 Prime and StrataCarte. Despite serving approximately 1,900 corporate customers across 50 countries with white-label products optimized for banks and broker-dealers, the company faces significant operational control weaknesses and regulatory uncertainties in a fast-evolving digital asset landscape. Liquidity constraints and the need for rigorous compliance will shape its near-term trajectory.

From Legacy Recycling to Blockchain: ALT5 Sigma’s Transformation Journey

Until early 2023, ALT5 Sigma Corp operated legacy recycling businesses under the former JanOne Inc. banner, primarily involved in appliance recycling through subsidiaries such as ARCA Recycling and ARCA Canada [S1][S27]. This segment was divested in March 2023 via a stock purchase agreement with VM7 Corporation [S1]. The strategic pivot accelerated in mid-2024 when JanOne acquired ALT5 Sigma Inc., a fintech holding entity specializing in blockchain-driven digital asset services, prompting a corporate rebrand to ALT5 Sigma Corporation that July [S1]. Further reinforcing its fintech strategy, the company acquired Fortress II Holdings Ltd., known for Mswipe—a next-generation provider of multi-currency fiat and crypto-enabled payment card services—in May 2025 [S1][S27].

ALT5 operates through multiple subsidiaries including ALT5 Sigma Canada Inc. and ALT5 Securities Inc., along with three key subsidiary platforms: ALT5 Pay (cryptocurrency payment gateway), ALT5 Prime (electronic OTC trading platform), and StrataCarte (crypto-capable multi-currency payment cards endorsed by Visa® and Mastercard®) [S1][S5][S25]. This structure caters exclusively to business-to-business clients rather than retail consumers.

Financial Performance Review: Revenue Decline and Mounting Losses

The company’s historical top-line shows significant contraction associated with its strategic overhaul. Revenue declined sharply from $103.6 million in FY2016 down to $12.5 million reported in FY2024—a drop exceeding 85% over eight years [F1]. Operating income turned positive briefly in FY2022 but plunged into large operating losses of -$7.56 million (FY2024) and further -$22.85 million projected for FY2025 [F1]. Net income reflects extraordinary charges expanding losses to -$344.51 million for FY2025 [F1], indicative of substantial write-downs or restructuring tied to the shift away from discontinued operations or fintech investments.

Operating cash flow mirrored this stress pattern: positive but modest inflows around $1.77 million in FY2024 collapsed into outflows approximating -$7.16 million by FY2025 alongside sharply curtailed capital expenditures ($11K in FY2025 vs $808K two years prior) reflecting austerity or shift toward software-centric innovation versus physical asset investment [F1]. Liquidity is constrained with a current ratio below unity at 0.57 due to current liabilities exceeding current assets [F1]. Equity surged nominally likely due to equity financings related to acquisitions but remains outpaced by net losses creating substantial shareholder value erosion [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -345 | -7 | -23 | 11000 | -5416.5% |

| 2024 | -6 | 2 | -8 | +20.1% | |

| 2023 | -8 | 1 | -20 | -171.1% | |

| 2022 | 11 | -3 | 5 | 808000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -7 | -29.9 |

| 2024 | -29.9 | |

| 2023 | 236.2 | |

| 2022 | -4 | 476.5 |

Source: SEC companyfacts cache [F1].

Figures encompass continuing operations; revenue YoY refers principally to latest periods available[F1].

Client Base & Product Ecosystem: Serving Institutions with ALT5 Prime, ALT5 Pay, and StrataCarte

ALT5’s business model targets institutional entities such as banks, FINRA-registered broker-dealers (~3,200 nationwide), funds, family offices, proprietary trading firms, liquidity providers among others — comprising approximately 1,900 corporate customers spanning roughly 50 countries [S5][S7][S16]. This contrasts sharply with dominant retail-focused crypto exchanges like Coinbase or Binance.

The suite comprises:

- ALT5 Prime: An OTC electronic trading platform enabling approved clients to transact major digital assets paired against fiat currencies including USD, CAD, EUR, GBP via browser or mobile app (ALT5 Pro). Integration supports FIX API connectivity and access through Broadridge’s NYFIX gateway facilitating seamless order routing essential for institutional trade execution workflows [S16][S6].

- ALT5 Pay: A cryptocurrency payment gateway offering merchants cryptopayment acceptance either converted immediately into fiat or retained as digital assets; integration capabilities include WooCommerce plugins and custom APIs suited for B2B merchant ecosystems [S21].

- StrataCarte: Multi-currency physical and virtual payment cards hosted on Visa® / Mastercard® networks designed for fiat plus crypto spending capability globally; bolstered by Mswipe acquisition synergies emphasizing seamless spend flexibility across traditional/crypto denominations [S27][S25].

Customization via white-labeling enables clients to embed these fintech solutions within existing infrastructure while maintaining compliance rigor essential for regulated entities [S16][S25]. Such tailoring creates niche differentiation focused on interface speed (low latency), advanced charting tools including Elliott formations forecasting, extensive APIs supporting institutional processes such as KYC documentation audit trails embedded directly into systems [S6][S21].

Operational Challenges: Internal Controls and Regulatory Compliance Risks

ALT5 acknowledges material weaknesses regarding internal controls over financial reporting impacting Sarbanes-Oxley Section 404 compliance efforts [S1]. These include inadequate segregation of duties related to contract negotiations/invoice approvals without proper oversight; insufficient controls on accrued expenses cutoff; deficient contract recordkeeping; ineffective invoice reconciliation procedures—all risks that may cause inaccuracies or delays in timely financial disclosures [S1]. Remediation plans are underway aiming at more stringent review protocols during accrual booking cycles.

Regulatory complexity extends beyond controls into AML/KYC enforcement within multiple jurisdictions where ALT5 operates entities subject to varied money transmitter licenses and data privacy laws such as GDPR or CCPA frameworks [S8][S14][S26]. Moreover:

- Crypto assets potentially classified as securities under SEC scrutiny could trigger registration obligations or enforcement actions constraining product offerings.

- Evolving US federal/state laws encompassing anti-money laundering laws increase compliance costs requiring continuous refinement of monitoring technology/supervision structures.

- Sanctions exposure exists given blockchain anonymity challenges complicating pre-clearance identification of counterparties risking inadvertent dealings with Specially Designated Nationals lists [S9].

These regulatory pressures impose legal risks that may also affect reputation while limiting scalable product expansion unless effectively managed through capital deployment towards technology upgrades plus skilled compliance personnel retention [S12][S26].

Competitive Moat Grounded in Tailored B2B Solutions for the Crypto Economy

ALT5 stands apart from consumer-centric crypto platforms emphasizing retail volumes by focusing exclusively on institutional segments where bespoke product features matter deeply—such as FIX API access preferred by professional traders requiring deterministic latency performance—and fine-grained user permission controls critical for regulated brokerages or custodianship firms [S7][S16]. The firm’s white-label strategy enables clients to deploy solutions under their brands maintaining continuity within their risk/compliance frameworks unlike conventional exchanges which present opaque black-box exposure.

However competitive pressure intensifies from established incumbents boasting deep liquidity pools plus decentralized exchange protocols gaining traction despite lack of regulatory clearance—an industry dynamic posing constant threat requiring innovation investment paired with regulatory agility efforts directed at sustained licensing renewal efficacy [S12][S16].

Liquidity, Capital Structure, and Capital Allocation Review

ALT5’s liquidity profile reveals constraints: current assets stood at $29.47 million against current liabilities of $51.40 million at fiscal year-end 2025 yielding a current ratio near 0.57 symptomatic of marginal near-term solvency challenges absent fresh capital input or turnover acceleration [F1][S10][S21]. Cash equivalents totaled approximately $6.22 million supporting operations alongside credit facilities including a secured $15 million loan agreement collateralized by WLFI tokens drawn down early in calendar year 2026 introducing additional leverage considerations though no direct origination or prepayment fees apply [S24].

Capital expenditures shrank dramatically suggesting shifting emphasis away from physical hardware investments towards software platform development but accompanying operating cash flows deteriorated into negative territory (-$7.16 million) pointing at heavy burn rate coinciding with revenue decline compounded by expense escalation linked possibly to integration costs relating Fortress II / MSwipe acquisition effects [F1][S18]. Equity appeared inflated likely driven by prior equity financing rounds offsetting accumulated losses contributing to deeply negative return on equity estimated around -30% derived from net loss relative to shareholder equity despite nominal balance sheet strength evolving last fiscal year-end figures ($1.15 billion equity predominantly intangible assets could explain magnitude)[F1].

Capital allocation measures such as dividends or share repurchases remain unreported indicating retention focus toward reinvestment prioritized on rebuilding technological infrastructure required for scalable institutional platform service delivery consistent with stated priorities on regulations and transparency principles internally espoused by management[S25].

Future Outlook: Growth Opportunities Tempered by Market and Regulatory Constraints (Analysis)

Growing institutional interest combined with demand for compliant blockchain-enabled trading/payment systems paints a potentially expansive market opportunity canvas especially within regulated environments where retail-first exchanges cannot operate safely without structural adjustments[S4][S7]. Traditional finance institutions exploring tokenization partnerships or fiat-to-crypto settlement enhancements position products like ALT5 Pay’s merchant gateways alongside OTC execution offered via ALT5 Prime as uniquely relevant.

Nevertheless, navigating intensifying regulatory scrutiny—particularly under SEC initiatives clarifying digital asset securities classification—and ensuring fraud prevention plus sanctions compliance impose burdensome costs that could limit rapid scaling absent significant capital infusion[S11][S26]. Competitive dynamics featuring better-known incumbents with deeper pockets remain formidable while decentralized exchange growth theoretically undermines centralized OTC trading profitability models compelling differentiation through premium service quality focused exclusively on institutional customization requirements.[S12][S26]

Key Milestones to Monitor and Potential Catalysts for Change (Analysis)

Investors should watch how effectively ALT5 can remediate material internal control deficiencies impacting financial accounting transparency per Sarbanes-Oxley expectations since failure may hamper Nasdaq listing status continuity[S1][S26]. Additionally, government regulator investigation outcomes including licensing renewals particularly related to money transmitter permissions across jurisdictions bear heavily on operational freedom[S4][S26]. Client base growth momentum tracked through new contract wins within banking/proprietary trading channel penetration—and licensing expansions permitting broader cross-border fintech deployment represents another critical barometer[S3][S27]. Quarterly earnings patterns providing insight into stabilization or further deterioration of cash flows offer real-time health diagnostics ahead of any strategic capital raises or restructuring moves necessary given ongoing net losses.

This analysis is based solely on historical financial data from SEC filings and disclosed corporate documents without any forecasted projections provided directly by the company.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments