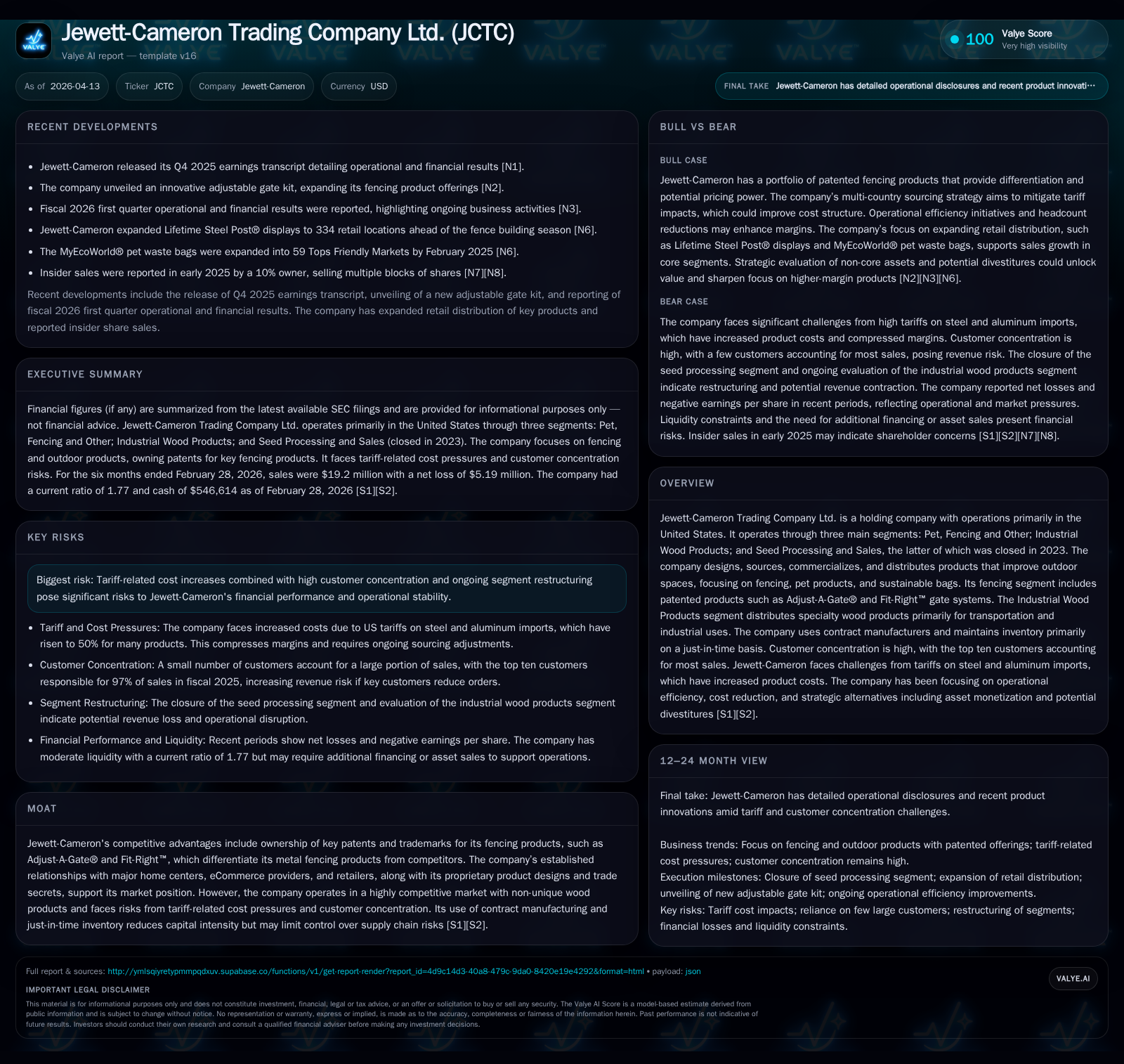

Jewett-Cameron Trading Co: Strategic Refocus amid Tariff Pressures and Operational Challenges

Jewett-Cameron confronts shrinking revenues and mounting losses by focusing on its patented fencing products and managing liquidity risks.

Jewett-Cameron Trading Co Ltd. has faced significant headwinds over recent years, with revenue declining from $62.9M in FY2022 to $41.3M in FY2025 accompanied by deepening losses and negative cash flows. The company closed its seed processing division in 2023 and has shifted strategic emphasis toward its differentiated fencing segment leveraging patented products such as Adjust-A-Gate®. Persistent US tariff increases on imported metals have inflated costs, pressuring margins and liquidity. Jewett-Cameron’s high customer concentration and reliance on contract manufacturing add complexity to its recovery path. Management is executing cost control efforts, inventory rationalization, and real estate disposals while exploring financing alternatives to bolster cash resources.

Overview

Jewett-Cameron Trading Company Ltd. is a holding entity operating chiefly within the United States across three main segments: Pet, Fencing & Other; Industrial Wood Products; and formerly Seed Processing and Sales, which was discontinued in 2023 due to declining quantities and rising costs rendering the operation uneconomical [S1][S14]. The company specializes in designing, sourcing, and distributing outdoor improvement products including fencing solutions that feature proprietary patented components like Adjust-A-Gate® and Fit-Right™ gate systems that differentiate their offerings from generic competitors [S16][N2].

Jewett-Cameron's operations are highly dependent on contract manufacturers largely situated outside the US, complemented by just-in-time inventory management practices aimed at reducing capital demands but potentially exposing supply chain vulnerabilities [S1][S16]. The firm maintains a concentrated customer base, with the top ten clients representing nearly all sales volume—an arrangement that magnifies revenue risks arising from customer attrition or pricing pressure [S5][S11].

Historical Performance

Over the last four years ending FY2025, Jewett-Cameron registered a progressive contraction in both revenue and profitability (see Table). Revenue slipped from $62.9 million in FY2022 down to approximately $41.3 million by FY2025—a decline of roughly 34% over that period primarily reflecting tariff disruptions, inventory write-downs, and segment restructuring including Seed division closure [F1][S16].

Operating income reversals intensified from a modest profit of $2.0 million reported in FY2022 to an operating loss exceeding $3.7 million in FY2025, signaling escalating margin pressure mainly driven by increased input costs (notably steel tariffs), less favorable sales mix, and consignment program effects on fencing lumber sales [F1][S13][S18]. Net income mirrored this deterioration with a swing from positive territory ($1.16 million net income in 2022) into substantial net losses (-$4.13 million in FY2025) linked to operating challenges compounded by credit-related expenses [F1].

Operating cash flows declined sharply into negative territory ($-6.6 million in FY2025), partially due to excess inventory buildup during uncertain demand cycles followed by discounting actions taken to offload surplus cedar fencing inventory after a key customer's consignment termination impacted working capital dynamics [F1][S22]. Capital expenditures remained modest relative to revenue but have risen slightly recently as management cautiously invests in operational support assets during transition phases [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 41 | -4 | -7 | -4 | -12.4% | -672.2% |

| 2024 | 47 | 1 | 6 | -2 | -13.2% | +3599.2% |

| 2023 | 54 | 0 | 6 | 0 | -13.7% | -101.8% |

| 2022 | 63 | 1 | -3 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -7 | -19.9 |

| 2024 | 6 | 2.9 |

| 2023 | 5 | -0.1 |

| 2022 | -5 | 4.8 |

Source: SEC companyfacts cache [F1].

The strategic decision to shutter the seed segment by August 31, 2023 eliminated a declining business line but also reduced diversification benefits for Jewett-Cameron going forward [S14]. Corresponding asset write-offs and related restructuring contributed notably to downward earnings impact during this transition.

Growth Prospects

Jewett-Cameron's future growth hinges on bolstering its fencing segment—a unique domain strengthened by several patented technologies like Adjust-A-Gate® gate kits offering measurement accuracy, durability, and ease-of-installation appealing both DIY consumers and professional contractors alike [N2][S16]. The recent product innovation launch of an adjustable gate kit reflects an ongoing commitment to expanding market share within this space by raising product differentiation against commoditized competitors [N2].

However, the company's ability to achieve meaningful volume growth is tempered by external constraints including elevated tariff rates targeting steel imports—principally affecting products sourced from China where rates have escalated up to 85% since early 2025—and general raw material cost inflation across global supply chains [S12][S16][S18]. Although Jewett-Cameron mitigated some tariff impact via supplier diversification into Bangladesh and Vietnam starting late fiscal 2024/early fiscal 2025 seasons, residual tariff burdens persistently erode margins.

Moreover, persistent reliance on a small group of customers concentrating roughly three quarters of sales constrains pricing power and heightens vulnerability should any large account reduce orders or shift to alternative vendors amid cost pressures or market disruption [S11][S29]. This client concentration risk remains a critical factor limiting upside growth potential absent customer acquisition or diversification initiatives.

Management continues to evaluate possibilities for divesting non-core assets—such as underutilized real estate facilities—and streamlining operations while focusing investment toward product innovation within fencing lines most aligned with long-term competitive advantage afforded by intellectual property ownership [S14][S21]. These moves are intended both to enhance operational efficiency and unlock capital for reinvestment purposes.

Expectations & Milestones

While no formal public guidance was provided for upcoming quarters beyond Q4 2025 results as per the latest earnings transcript, key metrics watchers should monitor at minimum:

- Progress on credit line renegotiations with Northrim Bank toward increased borrowing capacity supporting liquidity needs ahead of peak Spring selling season;

- Inventory levels normalized post-excess cedar sell-off reported during H1 fiscal year 2026;

- Revenue trends within the fencing segment amid continued tariff environment volatility;

- New product sales contribution following scheduled commercialization initiatives like adjustable gate kits;

- Cash flow improvements stemming from operational cost reductions and any realized gains on asset dispositions.

Management highlights efforts focused specifically on strengthening liquidity through multiple channels including potential equity or debt financing options alongside asset monetizations underscoring the severity of cash flow concerns exacerbated by operating losses and working capital draws during fiscal year transitions [S1][S23][N1].

Returns & Capital Allocation

Jewett-Cameron's return metrics reflect its ongoing challenges with profitability setbacks contributing to negative return on equity estimated near -20% for FY2025 (calculated using net loss divided by average equity) [F1]. Capital allocation has been restrained given financial constraints; capital expenditures remain low relative to revenue while historic share repurchases ceased years ago reflecting preservation priorities under current stress conditions.

Operating cash flow deficits approaching $6.6 million coupled with minor capex (~$115k) result in materially negative free cash flow for FY2025 of approximately -$6.7 million indicating significant capital outflows that must presently be financed externally or through working capital adjustments [F1]. Efforts around inventory reduction have been crucial not only for margin preservation but also unlocking stranded capital essential given near-maxed-out credit facilities with Northrim Bank ($4.3m out of $6m limit borrowed as of late fiscal year) [S23].

Dividend distributions have not been declared since fiscal deterioration began; no recent announcements signal resumption absent stabilized cash flows or profitable turnaround execution benchmarks.

Competitive Position & Risks

Intellectual property ownership via patents covering core fencing components underpins Jewett-Cameron’s chief moat distinguishing it within a competitive landscape marked otherwise by commodity wood products readily available elsewhere at competing prices or quality levels [S25].[Footnote: Company owns seven US patents plus foreign equivalents related specifically to Adjust-A-Gate® type hardware enhanced installers’ accuracy and longevity.] However intellectual property enforcement costs could arise should infringement disputes occur threatening resource diversion.

Tariff shocks remain an outsized risk factor casting uncertainty over supply costs unpredictably affecting planning horizon estimates while high customer concentration intensifies vulnerability if lost accounts cannot be replaced promptly causing immediate substantial volume decreases with cascading margin impacts [S12][S25].[Footnote: Top two customers alone represent ~74% total sales posing clear dependency risk.] Supply chain dependencies on overseas contract manufacturers introduce risks related to geopolitical tensions or logistical interruptions beyond company control.

Liquidity risks loom large highlighted repeatedly by management acknowledging need for additional funding beyond current credit arrangements—failure here could endanger operational continuity especially around critical selling periods requiring inventory procurement upfront for seasonal demand spikes like Spring/Summer home improvement cycle typical of fencing markets [S1][N1].[Footnote: Management strategy includes potential asset sales including North Plains Oregon real estate listing at ~$7M adjusted price.]

Analysis Summary

Jewett-Cameron Trading Company Ltd faces fundamental pressures reshaping its operating landscape since FY2022 including slumping revenues compounded by tariff-driven cost escalations clobbering margins resulting in steep net losses paired with severely negative operating cash flows underscoring liquidity constraints. A strategically focused pivot towards its proprietary fencing product portfolio aims at leveraging patented differentiation coupled with aggressive management efforts around cost containment, asset monetiation, inventory rationalization, supplier diversification plus financing alternatives represents pragmatic steps attempting stabilization.

Nonetheless considerable execution risk persists given continued dependence on a concentrated customer base susceptible to pricing pressures amidst broader macroeconomic uncertainties defined largely by evolving trade policies impacting key commodity inputs. How effectively Jewett-Cameron navigates these pressures will shape its trajectory through fiscal 2026 — success requires simultaneous progress on commercial growth initiatives alongside securing adequate liquidity buffer sufficient for normal course operations without distress-driven divestitures.

Disclaimer: This report is for informational purposes only based on publicly available information including regulatory filings and news disclosures as of April 13, 2026. It does not constitute investment advice nor a recommendation to buy or sell securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments