E-Smart Corp. Revenue Soars Yet Operating and Net Losses Deepen Sharply

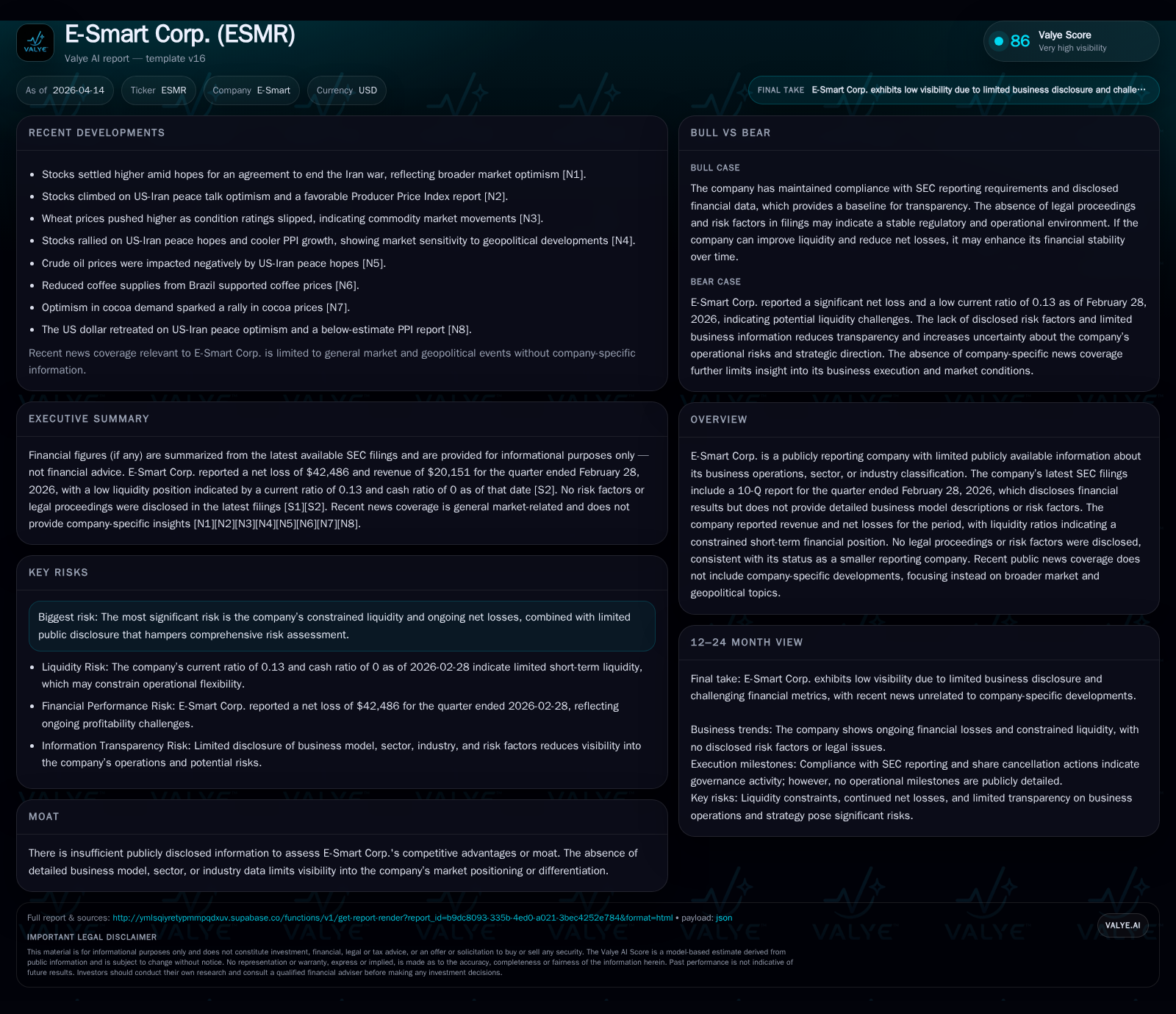

E-Smart Corp. exhibits a striking disconnect between rapid revenue growth and escalating financial losses, accentuating liquidity challenges and strategic shifts.

E-Smart Corp.'s fiscal years 2024 to 2025 reveal an explosive revenue increase of over 145%, yet operating and net losses have deteriorated markedly, underscoring significant margin pressures or rising expenditure. The company's liquidity position is critically strained, with a current ratio of just 0.13, highlighting acute short-term solvency concerns. Governance changes featuring new independent directors signal efforts toward strategic recalibration amid ongoing capital allocation stress characterized by a voluntary cancellation of two million shares. Forward-looking visibility is limited given scant company disclosures, necessitating vigilant monitoring of operational and financial metrics.

Historical Financial Trajectory: Rapid Revenue Growth Against Widening Losses

Between fiscal years 2024 and 2025, E-Smart Corp.’s financial profile presents a paradox wherein top-line expansion starkly contrasts with bottom-line declines. Revenue more than doubled from $11,935 to $29,289 representing an outsized year-over-year growth rate of +145.4% [F1]. Such robust topline growth would typically signal improving operational momentum; however, the company’s operating income tells a contrary story.

Operating loss deepened markedly to -$58,141 from -$34,363 (-69.2% worsening), reflecting accelerated cost absorption relative to sales gains [F1]. Net income deteriorated even more steeply: from a positive $41,236 in FY2024 it swung to a negative -$68,034 in FY2025 (a -265% change), underpinning acute profit margin compression or extraordinary non-operating expenses [F1].

Operating cash flows compounded concerns, plunging nearly threefold from -$10,973 in FY2024 to -$43,452 in FY2025 (a -296% decline) indicating intensified cash burn perhaps driven by working capital demands or investment spending exceeding operational receipts [F1]. This scenario—expanding revenue met with disproportionate rising losses—often signals impaired operating leverage utilization or an inability to sufficiently control variable costs amid rapid scaling.

Equity itself fell deeper into negative territory over this period ($-30,810 to $-59,708), reflecting accumulated deficit growth consistent with sustained losses [F1]. This erosion presents challenges for the balance sheet’s resilience going forward.

Historical performance (annual)

| FY | Rev ($) | Net ($) | CFO ($) | OpInc ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 29289 | -68034 | -43452 | -58141 | +145.4% | -265.0% |

| 2024 | 11935 | 41236 | -10973 | -34363 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 113.9 |

| 2024 | -133.8 |

Source: SEC companyfacts cache [F1].

Table summarizes key financial metrics evidencing rapid growth accompanied by deepening losses and cash flow deterioration.

Liquidity Constraints and Their Impact on Operational Flexibility

A critical dimension compounding E-Smart’s challenges is its severely impaired liquidity position as reflected on its February 28, 2026 balance sheet: cash & equivalents stand at only $1,138 against overwhelming current liabilities totaling $247,822—a disparity producing a perilously low current ratio of just 0.13 [F1][S12][S13].

Such working capital deficiency implies that current obligations exceed readily available liquid assets by nearly eightfold—a scenario typically indicative of acute short-term solvency risk absent external financing or operational turnaround.[F1]

This liquidity crunch raises red flags around the company’s ability to settle payables punctually or fund day-to-day operations without resorting to emergency measures or dilutive capital raises.

Moreover, tight liquidity curtails flexibility to invest in growth initiatives or weather unexpected shocks—factors particularly critical for emerging companies with narrow financial buffers.

The absence of disclosed debt maturities or covenant waivers in filings limits insight into external repayment pressures but underscores requisite scrutiny on receivables management and inventory turnover efficiency given this fragile balance sheet context.

Corporate Governance Updates and Their Strategic Signals

In January 2026, notable governance developments occurred with E-Smart’s appointment of two independent directors: Lukas Diaz and Manuel Martinez Garcia [S3][S11][S14]. Both bring expertise aligned with digital platform strategies—Mr. Diaz focusing on scalable online marketplace solutions within creative industries; Mr. Martinez Garcia specializing in advisory services around digital commerce and technology-enabled business transformations.

These board additions represent a strategic refresh aimed at injecting external oversight combined with sector-relevant acumen during a period of heightened operational stress.

From a governance standpoint, their independent status reinforces regulatory compliance and may fortify alignment on implementing digital transformation initiatives inferred from their professional backgrounds.

However, no compensatory arrangements had been formalized at appointment time; nor was there any indication these moves altered executive control—a pattern consistent with small-cap companies seeking board expertise enhancements without diluting existing management authority.

Capital Allocation: Share Cancellations Amid Cash Flow Challenges

A remarkable capital structure maneuver took place concurrently: on January 28th, the company effected voluntary cancellation of two million common shares previously held by director Diana Vasylenko without consideration [S11][S14].

This action reduced total outstanding shares from approximately 5.8 million to about 3.8 million; restricted shares decreased similarly while freely tradable shares remained unchanged at roughly 1.3 million.

Unlike conventional buybacks involving repurchasing shares using cash reserves aimed at enhancing value per share or redistributing excess capital, E-Smart’s cancellation was a non-cash surrender by an insider designed possibly for governance optimization or signaling confidence absent direct liquidity outflow.

Nonetheless, given the company’s precarious cash position and persistent operating deficits ([F1]), this decision highlights stressed capital allocation conditions where share count reduction substitutes for conventional repurchase programs constrained by limited free cash flow.

No dividends have been declared historically or contemporaneously ([F1],[S11]). Negative operating cash flows coupled with constrained liquidity preclude feasible capital returns through distributions presently.

Profitability Prospects: Risks and Opportunities Ahead

The future profitability outlook for E-Smart remains opaque due to sparse company-specific guidance disclosures; recent quarterly filings notably omit explicit forecasts or detailed risk factor descriptions indicating continued uncertainty ([S2],[S7]).

Absent sector classification or business model granularity further clouds assessment prospects.

Recent public news coverage emphasizes generalized macroeconomic themes without company-level operational updates ([N1],[N2]) restricting forward visibility further.

Nonetheless, escalating net losses juxtaposed against soaring revenues suggest persistent margin pressure either via increasing cost bases outpacing sales efficiencies or investment-heavy expansion phases eroding near-term earnings stability.

Success hinges on whether newly appointed board members can steer effective digital platform deployment optimizing monetization and controlling variable costs amidst liquidity constraints outlined earlier.

Emerging growth companies often confront such volatile profit trajectories; hence disciplined financial management combined with strategic realignment are prerequisites for restoring sustainable operating leverage.

Key Metrics to Monitor Moving Forward

Given limited transparent disclosure but observable performance dynamics documented herein investors and observers should closely track:

- Topline trajectory consistency beyond FY2025’s pronounced surge,

- Trends in gross margin improvement reflecting cost structure rationalization,

- Quarterly progression in operating losses signaling either stabilization or exacerbation,

- Cash burn rates vis-à-vis operating cash flow generation improvements,

- Movement in the current ratio as an early warning indicator for solvency improvement,

- Board strategic communications elaborating corporate direction especially related to digital initiatives,

- Any subsequent capital structure alterations including equity raises or debt modifications impacting financial flexibility.

Monitoring these metrics will yield practical insights into whether E-Smart can reconcile its revenue growth aspirations with imperative profitability restoration under existing liquidity pressures.

This analysis synthesizes all available public financial data and SEC disclosures as of April 14th, 2026 without speculative extrapolation beyond verified information sources. It neither constitutes investment advice nor reflects endorsement but serves as an informed internal review recognizing gaps in public transparency characteristic of smaller reporting firms.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments