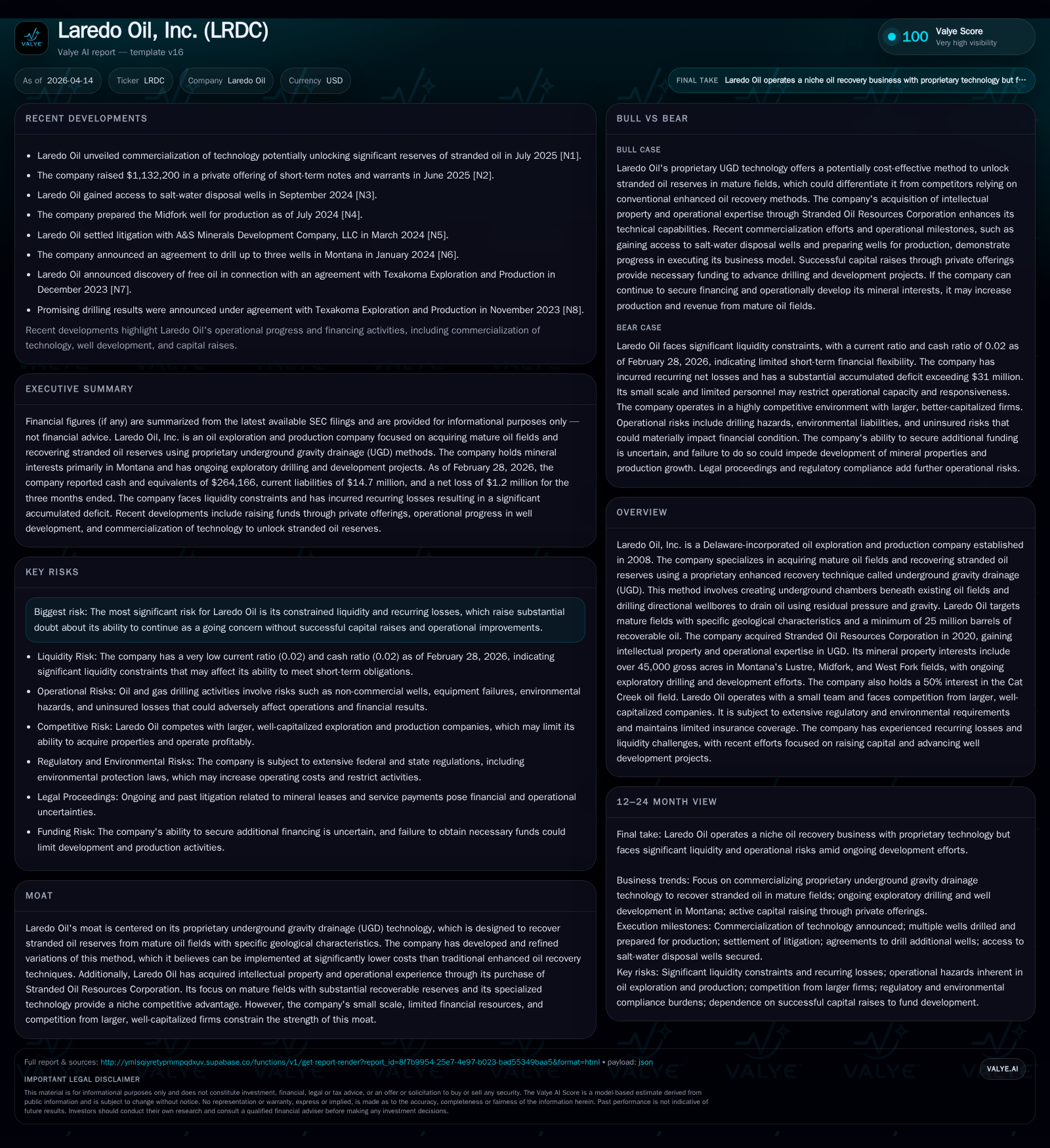

Laredo Oil's Struggle to Monetize Mature Fields with Underground Gravity Drainage

The company’s unique underground gravity drainage technology contends with severe liquidity constraints and steep revenue declines.

Laredo Oil, Inc. focuses on extracting stranded oil from mature fields using its proprietary underground gravity drainage (UGD) method, which promises lower costs compared to traditional enhanced oil recovery techniques. Despite this niche technological edge, the company faces a sharp plunge in revenue—down over 74% year-over-year—as it grapples with persistent operating losses and negative cash flow. A heavy debt load and near-impossible current ratio underline critical liquidity risks, casting doubt on the firm’s viability without successful capital raises. Future growth hinges on securing financing to expand UGD operations in key Montana fields, while investors should monitor drilling success and debt refinancing developments closely.

From Modest Revenue to Major Losses: Historical Financial Trajectory

Laredo Oil's financial history reveals a stark descent from modest operational revenue toward deepening losses despite its specialized recovery approach. The firm's revenue peaked modestly at $36,482 in FY2024 before plummeting 74.2% to just $9,423 in FY2025 ([F1]). This decline contrasts with operating losses that remain substantial yet relatively stable around -$3.3 million annually, reflecting ongoing high fixed costs despite contracting sales. Net income followed a similar pattern of persistent loss, recording -$3.18 million for FY2025 with an 11% worsening year-over-year.

Operating cash flow has been consistently negative for several years (-$1.65 million in FY2025), illustrating cash burn outpacing actual revenue generation ([F1]). Meanwhile, capital expenditures have been nearly minimal recently (only $303 in FY2023), indicative of constrained funding for new drilling or development projects. Equity has shrunk substantially into negative territory (-$12.57 million at FY2025), underscoring accumulated deficits driving shareholder equity below zero.

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 9423 | -3 | -1649834 | -3 | -74.2% | -11.0% |

| 2024 | 36482 | -3 | -632542 | -3 | +7.9% | |

| 2023 | 0 | -3 | -1640372 | -3 | ||

| 2022 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 25.3 |

| 2024 | 25.6 |

| 2023 | 61.2 |

| 2022 |

Source: SEC companyfacts cache [F1].

Financial results reveal sharp top-line contraction with persistent operational deficits limiting internal resource rebuilding.

UGD Technology: Commercial Promise Meets Practical Limits

Laredo Oil's moat revolves around the proprietary underground gravity drainage (UGD) technique acquired through its purchase of Stranded Oil Resources Corporation (SORC) in 2020 ([S1]). UGD entails mining chambers beneath mature oil reservoirs and then drilling directional wellbores that exploit residual radial pressure and gravity to mobilize trapped oil without reliance on costly thermal or chemical EOR injections.

The firm targets mature fields where at least 25 million barrels remain recoverable but where traditional methods leave behind stranded reserves due to economics or geology ([S1]). While this is an innovative niche approach hypothesized to lower extraction costs materially relative to other EOR methods such as steam flooding or CO2 injection, its application is geographically and geologically constrained.

Operationally, Laredo strategically caps conventional wells once developing the UGD chamber below is feasible to transition production smoothly without significant field disruption ([S1]). However, field-level execution complexities tied to specific lithology and reservoir characteristics inevitably limit scalability. The technology’s commercial viability thus resides primarily in select mature fields within the United States — notably the Montana Lustre, Midfork and West Fork fields — reflecting careful play selection rather than broad industry applicability.

Current Capital Structure: Debt Burden and Cash Scarcity

Liquidity metrics paint a concerning picture for Laredo Oil’s short-term financial health. As of February 28, 2026, current liabilities stood sharply elevated at approximately $14.7 million compared with current assets around $352 thousand ([F1]), yielding an ultra-low current ratio of roughly 0.02 — an acute red flag signaling near-term funding distress ([F1]).

The company relies heavily on multiple short-term bridge notes and promissory notes issued throughout fiscal year 2025 bearing interest rates around 12%, many convertible into common stock at substantial discounts (~35%) upon default or investor option [S3][S6][S8].

Together with legacy secured promissory notes tied to their acquisition of SORC assets ([S4]), these liabilities impose recurring onerous interest burdens as well as dilution risks through warrant issuances accompanying debt placements ([S17][S19]). Additionally noted are related-party loans including those from principal owners investing directly into well development ventures ([S20][S22]).

Such a complex mosaic of debt instruments reflects necessary but costly bridging financings that strain operational flexibility while the company seeks sustainable cash flow generation from its oil production.[^analysis]

[^analysis]: High issuance cost debt with embedded equity conversion features typifies nascent E&P plays struggling for stability without larger institutional backing.

Evaluating Future Growth Prospects Under Financial Constraints

The firm has identified numerous potential acquisitions and expansion prospects predicated heavily on raising capital sufficient to deploy UGD technology more broadly ([S1]). However, the vast majority of their drilling efforts remain exploratory or developmental within their existing Montana acreage — including the Lustre and Midfork fields — where results have so far been impeded by practical challenges like excess water intrusion and economics ([S14][S25]).

Without a marked improvement in liquidity or successful external fundraising efforts beyond recent private placements totaling roughly $1 million combined over fiscal quarters ending early 2026 ([S12]), any material scaling remains infeasible.

Competitive pressures from larger players employing established EOR methods further constrain Laredo's addressable market size given limited CAPEX capacity and small operational scale ([S1]). Thus growth prospects remain contingent on navigating these financial headwinds while proving technical feasibility consistently.

What Investors Should Watch: Upcoming Catalysts and Milestones

Key indicators monitoring Laredo Oil's trajectory include:

- Resolution status and impact of existing legal settlements related to mineral lease disputes in Montana following Lustre Oil Company lawsuits ([S1]).

- Scheduled repayments/refinancing outcomes for expensive bridge notes coming due between late 2025 through early 2026 ([S3][S6]), especially given cash scarcity.

- Operational progress reports regarding development wells within Lustre/Midfork fields driven by UGD implementations; specifically whether drilling results overcome prior uneconomical water issues ([S14][S25]).

- Any announcements around new capital infusion rounds ideally reducing reliance on convertible debt instruments that dilute equity value.

- Updates on exploration activities linked with newly formed subsidiaries such as Laredo Mex LLC for international expansion though currently dormant ([S25]).

Considering absence of official future guidance or forecast disclosures from management filings or press releases as of Q3 FY26 end ([N/A]), these constitute practical milestones rather than explicit targets.

Capital Allocation Decisions: Dividends, Buybacks, and Return Metrics

No dividends or share repurchase programs have been recorded amidst sustained losses throughout fiscal years examined ([F1][S10][S12]). The priority remains preserving liquidity amid ongoing cash burn compounded by high financing costs.

Interestingly calculated return on equity ratios approach positive levels (~25%) when dividing net loss figures by deeply negative book equity balances; however this is an accounting artifact rather than economically meaningful profitability signal due to substantial accumulated deficit carried on balance sheet ([F1]). This highlights that reported equity erosion stems from historical operating losses rather than capital returns.

Free cash flow remains negative (-$1.65 million estimated) combining operating cash outflow with near-zero capital expenditures reflecting paused development during funding droughts ([F1]). This underscores that no excess cash exists for discretionary shareholder remuneration.

Summary: Viability Outlook Amid Commercial and Financial Challenges

Laredo Oil operates at a complex crossroads merging specialized technical expertise via its underground gravity drainage technology with acute financial fragility marked by minimal revenues against heavy indebtedness. Its proprietary approach potentially unlocks overlooked stranded reserves with lower expenditure requirements compared to traditional enhanced oil recovery methods—addressing a valuable niche within mature U.S. producing fields particularly across Montana's basins.

Nevertheless, sustained cash deficits coupled with a crippling current ratio near zero severely jeopardize operational continuity absent successful recapitalization efforts detailed in recent SEC filings ([S8]). This liquidity bottleneck dampens ability to expand drilling programs needed for commercial validation while exposing shareholders to dilution risk through convertible securities issuance pathways.

In sum, Laredo Oil exemplifies a micro-cap energy explorer balancing promising innovation against stark capital constraints—a scenario warranting close scrutiny of near-term financing developments alongside measured progress on technical execution within targeted oil plays.

Disclaimer: This analysis is based solely on publicly available regulatory filings and documented corporate disclosures as cited; it does not constitute investment advice nor predict future stock performance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments