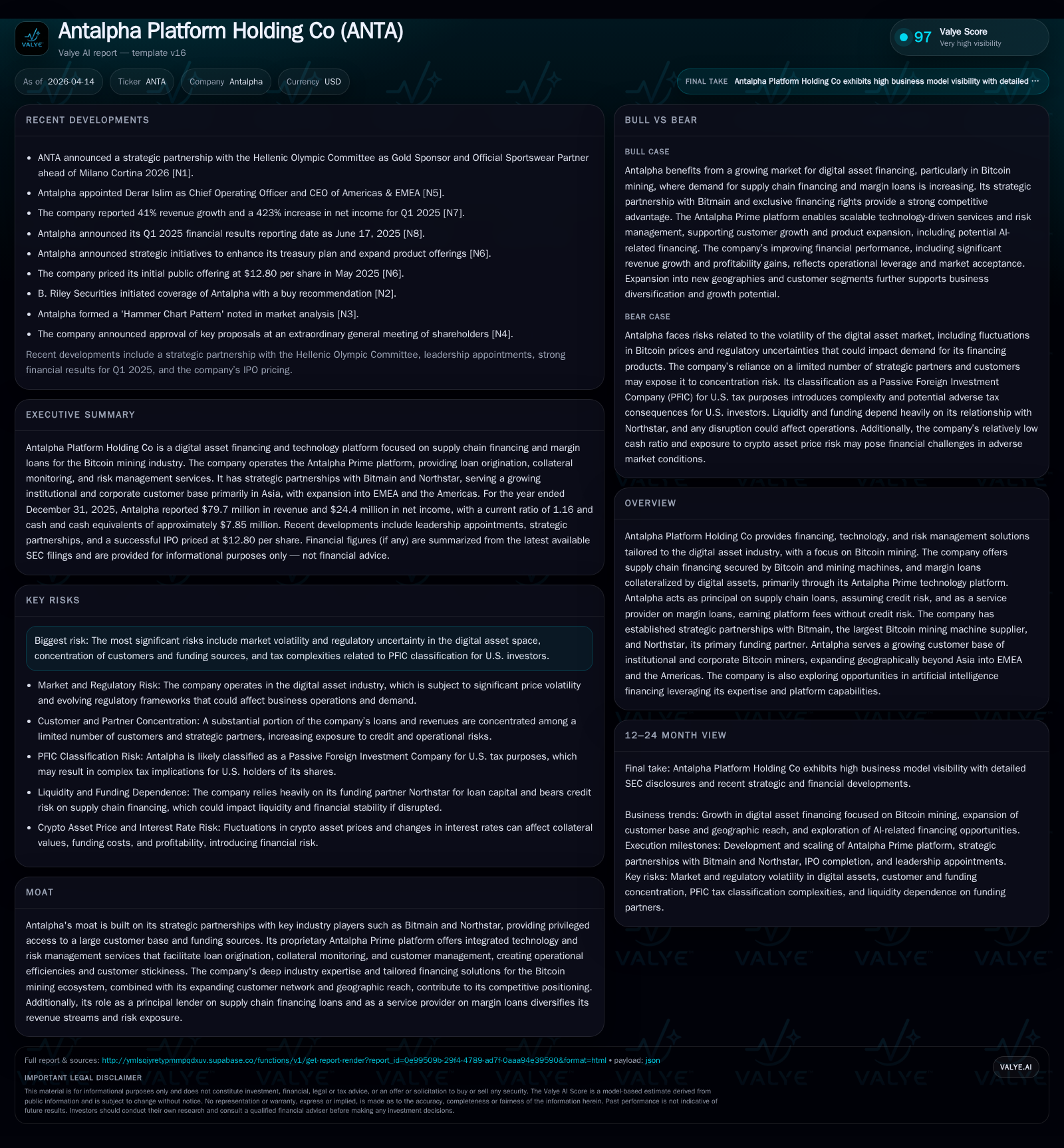

Antalpha Platform Holding Co's Growth Fueled by Strategic Partnerships and Bitcoin Mining Financing

Antalpha leverages relationships and technology to dominate supply chain financing in Bitcoin mining with expanding geographic reach.

Antalpha Platform Holding Co has rapidly grown by providing tailored financing, technology, and risk management solutions to the Bitcoin mining industry, primarily through its proprietary Antalpha Prime platform. Historical growth has been driven by strong strategic partnerships with Bitmain and Northstar, enabling access to a growing customer base and funding capacity. The company’s future growth depends on market demand for Bitcoin mining equipment and digital assets, expansion beyond Asia, and innovation in new financing applications such as GPU-based AI computing. While capital-efficient with a solid liquidity position, Antalpha faces risks related to volatile crypto markets and evolving regulatory frameworks.

Company Overview

Antalpha Platform Holding Co specializes in providing integrated financing, technology, and risk management solutions specifically for the digital asset industry with an emphasis on Bitcoin mining. The company operates primarily through its proprietary Antalpha Prime platform which facilitates supply chain financing secured by Bitcoin mining machines and margin loans collateralized with digital assets.

Historical Performance

Since inception, Antalpha has exhibited rapid revenue growth coupled with improving profitability metrics. Revenue advanced from lower single-digit millions to approximately $79.7 million at the end of 2025 [F1]. Net income turned positive after initial losses reflecting operational scale and better cost absorption. Adjusted EBITDA trends underscore this operational improvement: from a loss of $7.4 million in 2023 it transformed into a strong profit of $33.2 million by year-end 2025 [S1].

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

*Operating cash flow less capital expenditure approximated from available data showing net negative free cash flow despite net income growth [F1][S9].

Revenue Drivers

Antalpha earns revenues mainly from two streams: technology financing fees associated with supply chain loans for Bitcoin mining machines, and technology platform fees from servicing margin loans facilitated via its partner Northstar [S10]. Historically the weighted average technology financing fee decreased slightly from 8.9% in 2023 to 7.8% in 2025 whereas platform fees increased consistent with service feature enhancements [S16].

A key catalyst for past revenue growth has been expanding loan originations supported by larger numbers of customers—rising from 41 in 2023 to over 80 by the end of 2025—with sector expansion beyond Asia into EMEA and Americas contributing to geographic diversification [S16][S22].

Business Model Nuances and Market Positioning

The company acts as principal lender for supply chain loans—typically USD or USDT-denominated disbursed directly to vendors like Bitmain for machine purchases or data centers for hosting services—entailing full credit risk exposure on these loans secured by held collateral including newly mined Bitcoins or mining equipment [S10][S17]. Conversely, Antalpha provides margin loan servicing via its platform without bearing credit risk; these loans are funded and held by Northstar who assumes defaults risk while Antalpha earns platform fees [S17][S22]. This dual role balances revenue streams against risk exposures.

Strategic partnerships underpin the company's moat:

- Bitmain refers customers seeking financing and grants rights of first refusal ensuring steady origination volume.

- Northstar provides committed funding facilities up to $1 billion annually (with accordion feature), supporting an asset-light model via rehypothecation of pledged collateral mainly Bitcoin [S14][S17].

Collateral value management is sophisticated utilizing near real-time monitoring within Antalpha Prime to maintain overcollateralization minimizing credit losses historically immaterial due to rigorous underwriting standards including AML/KYC/KYT compliance protocols [S10][S21].

Future Growth Prospects

Growth potential lies primarily in scaling the existing core business complemented by incremental product innovation:

- Continued expansion of the customer base internationally given increasingly global Bitcoin mining activity.

- Developing lending products tailored towards emerging computing environments such as GPUs for AI workloads indicates early-stage diversification opportunities leveraging the firm’s technological infrastructure [S1].

- Enhancing fee structures by increasing platform utility may mitigate expected fee compression as competition intensifies.

- Maintaining close alignment with key partners Bitmain and Northstar helps secure preferential access amidst an evolving competitive landscape.

However, growth pacing may be capped or complicated by factors like regulatory shifts imposing new licensing requirements or compliance costs especially related to consumer/commercial lending definitions under U.S. laws impacting cross-border operations [S20]. Market volatility affecting the price of Bitcoin can also materially influence loan demand and collateral valuations directly affecting earnings stability.

Capital Structure & Liquidity

Antalpha maintains robust liquidity supported by:

- $7.9 million cash & equivalents at year-end 2025.

- Substantial crypto assets holdings used as collateral underpinning borrowings.

- A revolving credit facility agreement with Northstar allowing drawdowns up to $1 billion annually at floating rate (federal funds rate plus spread), featuring fixed minimum one-year tenors modifiable without penalty enhancing financial flexibility [F1][S14].

During calendar year 2025, the company drew down approximately $1.18 billion under this facility repaying $563 million subsequently leaving $1.03 billion outstanding demonstrating active usage aligned with loan origination volumes; funding cost sensitivity analysis shows material impacts on operating income if federal funds rate shifts significantly highlighting interest rate risk exposure [S3][S15][S19].

Free cash flow was negative roughly $4.2 million in 2025 as investments into platform development and working capital needs outpaced net income conversion into cash flows illustrating ongoing reinvestment imperative despite strong profitability metrics [F1][S9].

Returns & Capital Allocation

Based on reported net income relative to equity base approximations, Antalpha generated an approximate ROE of around 20% for fiscal year ending December 31, 2025 reflecting efficient equity utilization given its asset-light structure relying heavily on debt funding through related parties rather than extensive fixed assets investment [F1].

There is no explicit mention of dividends or share repurchase programs within recent reporting periods signaling retained earnings reinvestment focus.

Risks Highlighted

Key risks emphasized relate chiefly to:

- Regulatory uncertainty: Licensing regime changes could impose constraints or require significant compliance investment especially if activities qualify as consumer/commercial lending under U.S./other jurisdictions potentially restricting operations or increasing operational costs [S20].

- Market volatility: Fluctuations in Bitcoin price impact collateral values directly influencing allowable loan advance rates which could force additional capital raising or constrain loan volume growth.

- Customer concentration: Despite expanding customer counts, a limited number represent significant portions of outstanding loans exposing Antalpha to default or performance risks upon borrower distress.

- Legal/Compliance: Exposure to anti-money laundering enforcement actions requires strict KYC/KYT procedures given international operations subjecting company to multiple jurisdictional laws potentially increasing legal risks or reputational harm [S20][S21].

- Tax complexity: U.S.-based investors face Passive Foreign Investment Company (PFIC) classification complications which might affect shareholder appeal although not corporate financials directly.

What To Watch / Analysis Forward-Looking Factors

Currently Antalpha has not provided explicit quantitative guidance or detailed milestones beyond general aims described around market expansion and technological development investments [N#]/[S#] absent here. Observers should track:

- Loan origination volume trends especially outside Asia as geographic expansion unfolds.

- Fee rate developments amid industry maturation potentially pressuring margins.

- Funding cost trajectory tied closely to central bank interest rate policy shifts affecting net interest spreads.

- Regulatory developments affecting digital asset lending frameworks across key jurisdictions where customers operate.

- Progress on extension into AI-related computing environments lending which could emerge as new revenue sources.

The company's business model built upon carefully structured partnerships plus proprietary tech platform creates barriers for peers lacking similar ecosystem integration — an important moat but one that must be actively defended as institutional traditional finance gradually enters crypto lending space presenting comparative pricing pressures.

Summary Table: Key Financial Highlights (in millions USD)

| Fiscal Year Ended Dec 31 | Revenue | Operating Income | Net Income | Cash & Equivalents |

|---|---|---|---|---|

| 2023 | (6.6) | 0.4 | ||

| 2024 | 4.4 | 5.9 | ||

| 2025 | 79.7 | 15.0 | 24.4 | 7.9 |

| Note: Operating income not separately reported for years prior to FY25; net income turned positive reflecting operational scaling. |

Conclusion

Antalpha Platform Holding Co reflects a compelling example of focused specialization within digital asset finance—leveraging fintech integration with niche expertise serving institutional Bitcoin miners through credit products backed by innovative tech platforms like Antalpha Prime. Their historical performance signals solid organizational execution underpinned by strategic partners Bitmain and Northstar facilitating access both upstream (machines) and downstream (capital). The path forward presents promising growth opportunities but hinges heavily on navigating evolving regulatory landscapes, maintaining competitive fee structures amid maturing lending markets, managing macroeconomic-driven funding costs, and executing global expansion successfully without diluting underwriting discipline. This nuanced business model demands continuous innovation while balancing complex operational risk factors inherent in digital asset ecosystems.

Disclaimer: This report is based solely on public SEC filings as of April 14, 2026 ([F1], [S1]-[S28]) without any forward-looking statements or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments