Chunghwa Telecom’s Mature Growth and High Dividend Strategy in Taiwan’s Telecom Landscape

A leading Taiwanese telecom operator balancing steady revenues with significant capital expenditures and elevated dividend payouts.

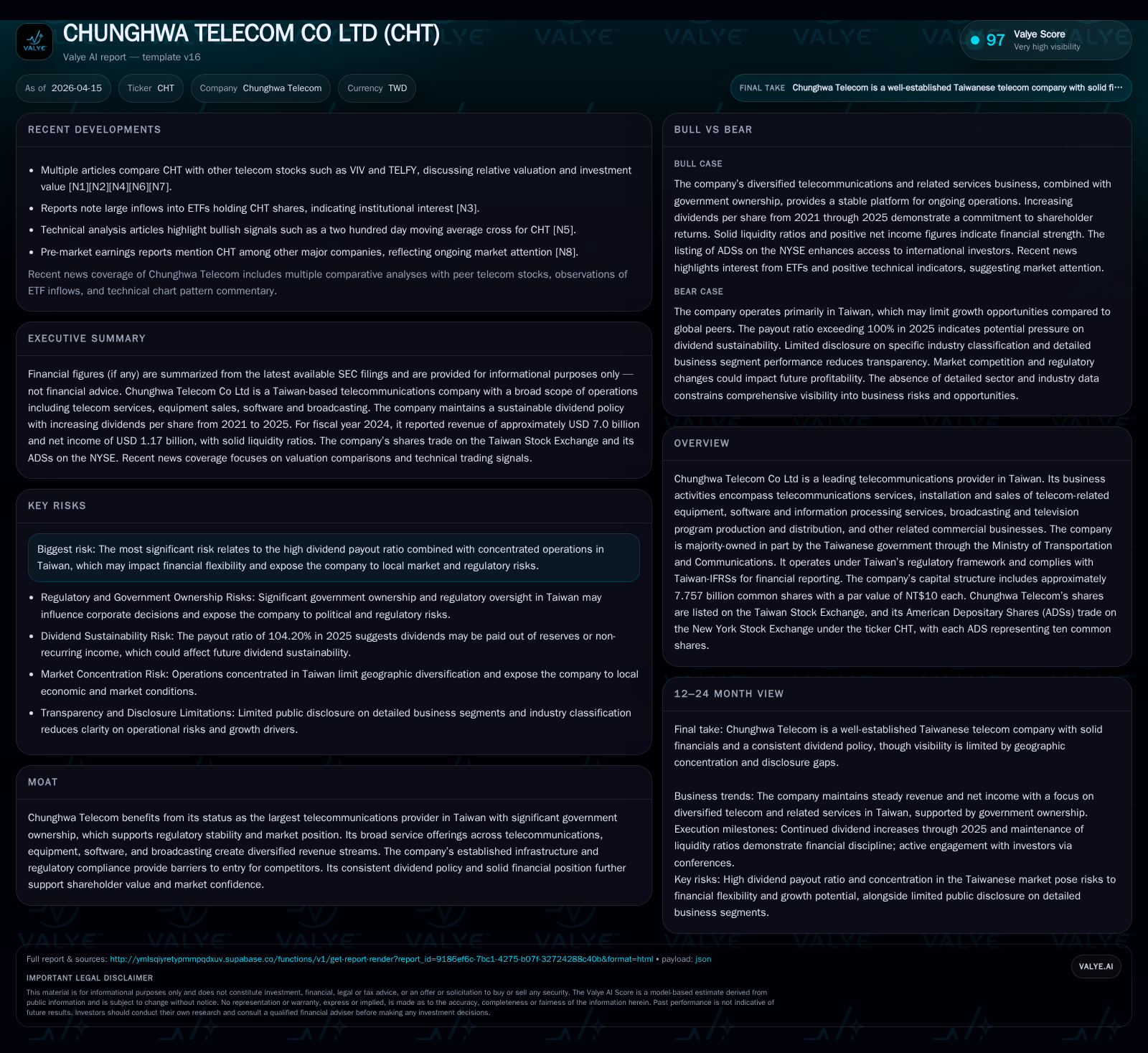

Chunghwa Telecom Co Ltd remains Taiwan’s largest telecommunications provider, supported by substantial government ownership and regulatory stability. Its revenue showed a modest decline in 2024 following years of steady performance, with a net income decrease reflecting ongoing capital investments and operating cost pressures. The company’s diversified services, including consumer, enterprise, international, and broadcasting operations, sustain revenue streams but also expose it to regulatory and market risks concentrated in Taiwan. Chunghwa Telecom maintains a high dividend payout ratio above 100%, which signals shareholder return priority but may limit financial flexibility for future investments. Planned capital expenditures in 2026 focus heavily on infrastructure upgrades tied to 5G, cloud AI data centers, and international submarine cables.

Company Overview and Market Position

Chunghwa Telecom Co Ltd stands as the dominant telecommunications player in Taiwan, operating under significant government influence through the Ministry of Transportation and Communications. The company's statutory structure includes roughly 7.757 billion common shares with listing both on the Taiwan Stock Exchange and as American Depositary Shares (ADSs) on the NYSE [S1][S4]. Its expansive service portfolio ranges from traditional telecom services—mobile and fixed line—to ICT services such as cloud computing, big data, cybersecurity solutions, broadcasting operations, and telecom equipment sales [S14][S18]. This diversification across multiple communications verticals provides resilience against market fluctuations.

Historical Financial Performance

Using consolidated figures converted at prevailing exchange rates at year-end, Chunghwa Telecom reported annual revenues of approximately $7.29 billion in FY2023 dropping slightly to $7.01 billion in FY2024—a decline aligning with modest contractions in voice service revenues offset partially by broadband growth [F1][S17]. Net income trended downward from $1.24 billion to $1.17 billion over the same period. Despite this dip in profitability, the company's overall equity base remained robust at approximately $12.9 billion mid-2023 before declining marginally to $12.1 billion by end-2024 [F1].

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2024 | 7.0 | 1174 | -3.8% | -5.6% |

| 2023 | 7.3 | 1243 | +3.3% | +0.9% |

| 2022 | 7.1 | 1232 | -7.1% | -7.8% |

| 2021 | 7.6 | 1336 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($bn) | ROE% |

|---|---|---|

| 2024 | 36.9 | 9.7 |

| 2023 | 36.5 | 9.7 |

| 2022 | 35.7 | 9.7 |

| 2021 | 33.4 | 9.5 |

Source: SEC companyfacts cache [F1].

All amounts in USD except dividends which are NT dollars

Revenue composition sees approx. 60% from consumer business mainly mobile services; enterprise segment accounts for ~33%, supported by ICT offerings including Internet Data Centers (IDC) and cloud security solutions; international business contributes about ~4%; while other subsidiaries including broadcasting make up roughly ~2% of total revenue [S17][S20].

Drivers Behind Historical Performance

Revenue fluctuations stem primarily from declines in legacy local and long-distance voice services as adoption shifts toward broadband and mobile data usage — consistent with regional telecom trends [S17][S22]. Growth in ICT-related enterprise services partially offset this erosion but wasn't sufficient to fully neutralize overall declines. Personnel expenses increased due to benefit adjustments affecting wages and bonuses while ICT project costs rose aligned with expanding digital transformation initiatives [S22]. Incremental utilities costs following electricity price hikes further pressured margins.

Future Growth Prospects

Chunghwa Telecom is investing substantially into next-generation infrastructure: planned capital expenditures for FY2026 are estimated at NT$31.9 billion (~US$1 billion), continuing the shift toward mobile broadband technologies (5G/5G-Advanced), submarine cable networks critical for international data transmission, multi-orbit satellite networking for enhanced connectivity, as well as investment in AI-powered cloud computing platforms [S15][S18]. These moves aim to capture emerging growth opportunities within advanced communication services despite an overall steady-to-slightly declining telecom market.

Furthermore, the company extends research into AIoT applications (e.g., smart traffic management), metaverse content delivery, cybersecurity enhancements including post-quantum cryptography deployment, reinforcing its foothold beyond basic connectivity toward intelligent service ecosystems [S18].

However, growth remains constrained by high penetration rates within Taiwanese markets limiting subscriber expansion potential, intense competition applying tariff pressure particularly on voice/interconnection charges mandated by regulators through gradual rate cuts scheduled through late-2026 [S23]. The heavy reliance on the Taiwanese market also concentrates geographic risk.

Outlook Indicators & Milestones

Explicit guidance details beyond capital expenditure plans are sparse; however, investors should monitor quarterly updates regarding:

- Progress on new infrastructure deployment milestones including submarine cables and satellite networks.

- Revenue mix evolution especially shifts between legacy voice services and digital transformation ICT revenues.

- Regulatory changes impacting interconnection fees or spectrum licensing that might influence margins.

- Dividend declarations around May shareholder meetings given their historically consistent timing.

The company's commitment to sustainable dividends within capital budgeting constraints will likely remain a key variable influencing free cash flow availability.

Returns & Capital Allocation Strategy

Chunghwa Telecom maintains a historically generous dividend policy reflecting its mature industry status: dividends distributed increased steadily from NT$33.4 billion in FY2021 to NT$36.9 billion in FY2024 with further rises approved for FY2025 totaling NT$40.3 billion [F1][S12]. The payout ratio recorded was notably high at over 100% (104.2% in FY2025)—implying dividends exceed net income derived under Taiwan IFRSs—underscoring emphasis on shareholder returns but raising questions about retention capacity for reinvestment without increasing leverage or asset sales [S12].

The company predominantly finances capital expenditures through operational cash flows supplemented occasionally by bond issuances at favorable interest rates ranging mostly below 2% [S7][S8]. As of end-2025 it held cash equivalents near NT$36.9 billion (US$1.2 billion) providing liquidity buffers [S1][S7].

Return on equity approximated just under 10% (9.7%) for recent fiscal periods highlighting stable profit generation relative to equity [F1]. However, shrinking net income juxtaposed against elevated dividend outflows hints at strained internal funding flexibility.

The company adheres to regulations restricting share repurchases yet has provisions allowing modest buybacks primarily for employee share plans or conversion mechanisms but must sell treasury shares within six months post-purchase if acquired [S5].

Risks & Regulatory Environment

As the largest incumbent with government ties, Chunghwa benefits from regulatory predictability yet confronts sector-specific risks:

- Monopoly-related regulations tightly control pricing practices preventing abuse of dominant positioning; deviations could attract substantial fines or corrective orders from Taiwanese Fair Trade Commission (FTC) [S6][S19].

- Competition scrutiny limits anti-competitive behavior including price fixing or exclusionary practices under the Fair Trade Act leading to potential penalties reaching up to NT$100 million or more plus sanctions against responsible persons including imprisonment if unremedied [S6][S19].

- Geographic concentration exposes the firm heavily to Taiwan's economic cycles, political developments, natural disaster risks (earthquakes etc.), and technological shifts altering demand dynamics [S6].

- High dividend payout ratios potentially restrict flexibility for opportunistic investments or absorbing shocks from unforeseen events.

- Currency fluctuations impact telecom equipment procurements internationally though mitigated via forward contracts expiring mainly within first quarter following balance sheet dates; interest rate risks remain limited given conservative fixed income asset holdings without derivative hedging [S1][S11].

Conclusion

Chunghwa Telecom embodies a mature telecommunications operator leveraging its dominant domestic position supported by governmental ownership to generate steady albeit slightly declining revenues amidst fundamental industry transitions away from legacy voice towards converged ICT platforms and digital services. Its aggressive dividend policy delivers consistent cash returns yet places limits on flexibility for large-scale expansions without external financing or asset reallocations. Focused infrastructure investments signal an intent to maintain competitiveness amid rising demands for fast broadband connectivity and integrated smart services energized by AI innovations. Stakeholders should track how Chunghwa balances renewing capex-driven growth levers against disciplined capital allocation amidst evolving regulatory frameworks concentrated within Taiwan’s telecommunications environment.

This report synthesizes publicly available filings submitted by Chunghwa Telecom Co Ltd as of April 15, 2026 combined with industry context; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments