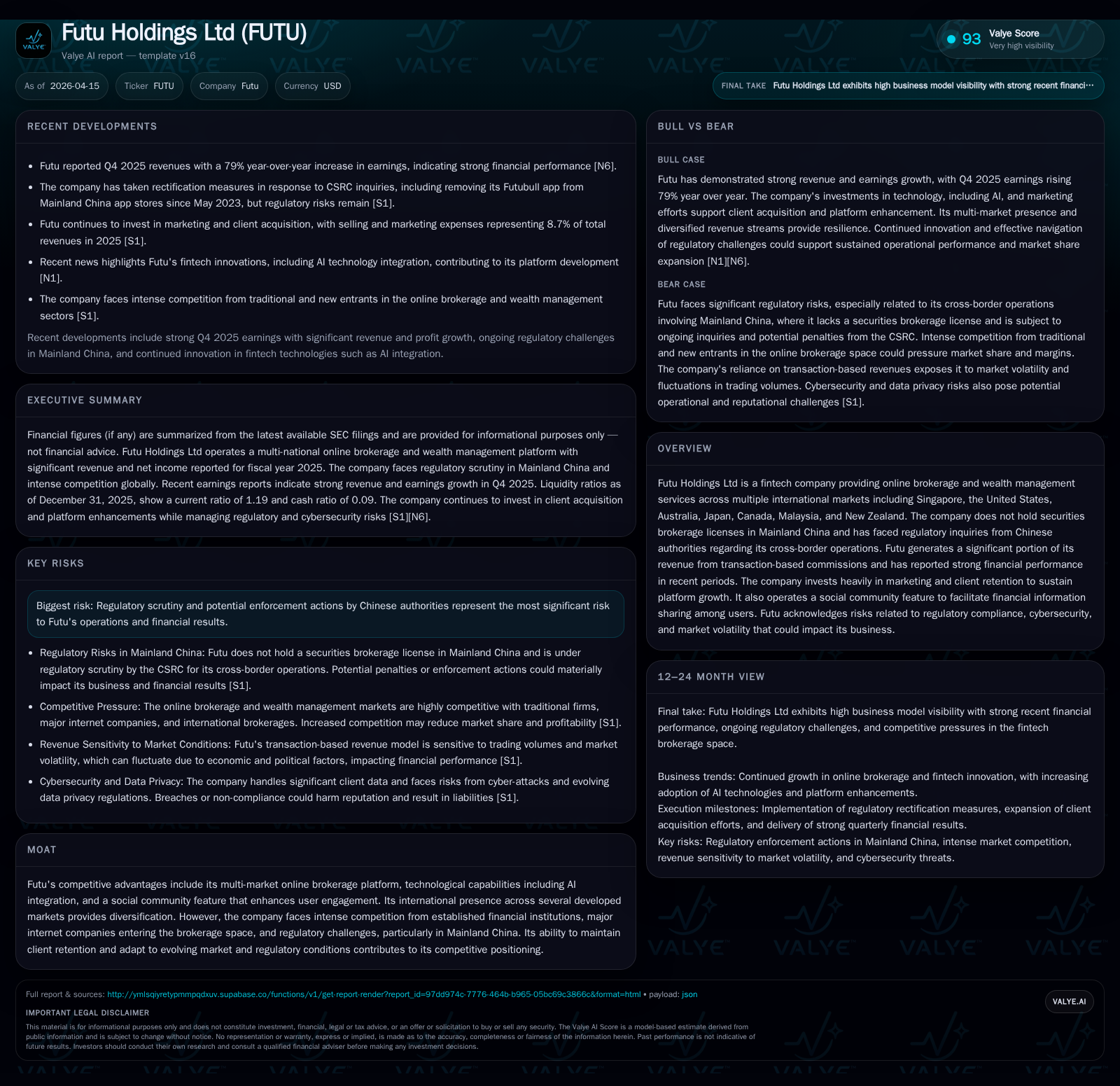

Futu Holdings’ Surging Revenue and Earnings Confront Regulatory and Competitive Hurdles

Futu delivered robust growth in 2025 backed by expanded client assets and trading volume, but regulatory risks in China and intensifying competition cloud its outlook.

Futu Holdings Ltd expanded its footprint across multiple international markets, leveraging its technology-driven brokerage platform to drive a significant increase in revenues and profits in 2025. Key growth drivers included higher client asset balances, increased trading volumes, and platform enhancements integrating AI tools and social features. Despite strong financial performance, the firm faces regulatory uncertainties from Chinese authorities related to its Mainland China operations, including rectification demands and potential sanctions. Additionally, competitive pressures from global brokers and tech giants entering the online brokerage space could constrain future growth. Capital allocation priorities emphasize product development, selective share repurchases under a new $800 million program, and maintaining liquidity to support expansion.

Historical Growth and Performance

Futu Holdings Ltd demonstrated remarkable top-line expansion over recent years supported by broad market adoption of its multi-jurisdictional online brokerage platform. Revenue rose sharply from $975.97 million in 2022 to $2.94 billion in 2025, representing a CAGR exceeding 40% during this period [F1]. This explosive growth was underpinned mainly by increased trading volumes—securities and options brokerage turnover escalated from HK$4.23 trillion in 2023 to HK$14.68 trillion in 2025—reflecting both higher client asset accumulation and improved market conditions [S1]. Futures contracts traded also grew steadily, signaling diverse product engagement.

Operating income mirrored this trajectory due to scalable technology investments allowing better operating leverage, more than doubling to $1.81 billion by end-2025 [F1][S5]. Net income likewise surged past $1.45 billion with margin improvement though some margin compression occurred as selling and marketing expenses near doubled year-over-year due to aggressive customer acquisition efforts across geographies [F1][S14]. Operating cash flow (CFO) turned strongly positive at $5.24 billion for 2025 after a negative swing in 2023, indicating improving working capital management alongside organic business growth [F1].

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($bn) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 2.9 | 1457 | 5.2 | 1809 | +67.8% | +107.9% |

| 2024 | 1.7 | 701 | 4.0 | 852 | +36.5% | +27.8% |

| 2023 | 1.3 | 548 | -0.8 | 641 | +31.3% | +46.1% |

| 2022 | 1.0 | 375 | 0.4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($bn) | ROE% |

|---|---|---|---|

| 2025 | 5.2 | 28.3 | |

| 2024 | 4.0 | 19.4 | |

| 2023 | 112 | -0.8 | 17.4 |

| 2022 | 403 | 0.4 | 14.0 |

Source: SEC companyfacts cache [F1].

Revenue YoY calculated where applicable; operating income began series only from FY23.

Drivers of Growth

Key drivers include strong client acquisition—funded accounts climbed over one-third year-over-year through end-2024—with further increases expected given ongoing platform enhancements and geographic expansion into regions such as the US, Singapore, Australia, Japan, Canada, Malaysia, and New Zealand via the Moomoo app variant [S16][S24]. Enhanced user engagement stems from Futu’s AI-powered investment tools (e.g., CashAI v5.5), integrated social community features facilitating knowledge sharing among investors, and broadened product offerings including margin financing and securities lending [N4][S7][S16].

Increased client asset balances have also played a pivotal role; these balances fuel higher trading volumes which directly impact commission revenues that comprise a large share of Futu’s total top line [S1]. Furthermore, expansion into wealth management product distribution is becoming a more substantial revenue contributor alongside core brokerage activities [S7]. Aggressive marketing spending supports scaled customer outreach while advancements in proprietary algorithms improve order execution efficiency promoting stickiness.

Future Prospects & Constraints

Growth is poised to continue but not without meaningful headwinds:

- Regulatory Environment: The most pronounced risk resides in the ongoing scrutiny by China’s CSRC concerning cross-border securities services provided domestically without licenses—most notably highlighted by the removal of the Futubull app from mainland Chinese stores since mid-2023 [S1][S12][S17]. While Futu undertakes rectification measures, any adverse regulatory actions including fines or operational suspensions could severely impair revenue streams derived from Chinese clients absent licenses.

- Competitive Dynamics: The online retail brokerage sector is attracting intensified competition worldwide from entrenched financial institutions as well as major internet platforms leveraging their ecosystems for brokerage offerings—pressuring commission rates and customer retention efforts [S16][S21]. Continued innovation will be necessary to maintain leadership.

- Market Volatility: As trading volumes are highly sensitive to market sentiment shifts and macroeconomic turbulence (including geopolitical events impacting global finance), variability can constrain revenue predictability despite diversified geographies offering some risk mitigation [S1].

The company pursues strategies around expanding product breadth beyond transactional commissions toward wealth management services with higher margins as well as deeper penetration into international markets supported by its technological backbone—which integrates AI-driven insights for customers—to offset potential limitations imposed by regulatory actions or competitive incursions [N4][S7].

Forecasts & Milestones to Watch

While explicit forward-looking guidance is limited publicly at this stage given regulatory uncertainties, key metrics to monitor include:

- Progression of regulatory compliance outcomes or imposed sanctions particularly by CSRC regarding mainland China operations.

- Client account growth trajectory across overseas markets given their increasing weight.

- Expansion velocity of margin financing balances and securities lending book which supports interest income growth.

- New product rollouts or platform innovations tied to AI capabilities enhancing user engagement metrics.

- Cost control effectiveness amid elevated investments in R&D and marketing.

The company’s next quarterly disclosures will shed light on whether momentum sustains post Q4 earnings beat reported in early March citing a near-80% earnings jump versus prior year, indicative of ongoing operational scaling success despite external challenges [N1][N2].

Returns & Capital Allocation

Futu's approximate return on equity stands near an impressive ~28% based on trailing twelve months net income relative to average equity indicating disciplined profit generation relative to shareholder capital deployed [F1]. Operating cash flow showed solid conversion into free cash flow after minimal capital expenditures of around $7 million for infrastructure upgrades primarily computer hardware — consistent with Futu's digital-first business model requiring modest physical capital compared with traditional finance firms [F1][S5].

Previously active buyback programs paused through end-2025 but recently reinstated with an authorization up to $800 million through late-2027 indicate commitment toward returning value while preserving flexibility amid uncertain environment [S4][S10][S11]. Dividends have been infrequent with policy favoring reinvestment into technology platform enlargement rather than distributions at this stage [S4]. Liquidity remains strong with cash reserves exceeding $1.3 billion across currencies emphasizing balance sheet strength critical for navigating rapid operational scaling alongside volatile credit exposures inherent in margin loan portfolios totaling approx $8.3 billion as of year-end per latest disclosures [F1][S6][S8][S20].

Sector Context & Strategic Positioning (Analysis)

In online brokerage sectors worldwide, there is increasing convergence between fintech innovation demands such as real-time data analytics powered by artificial intelligence and regulatory complexity encompassing KYC/AML compliance plus local licensing hurdles —all within intensely competitive environments fueled by digital disruption from large tech platforms extending vertically into financial services for their user bases.

Futu’s multi-market reach enables regional diversification rare among peers focused domestically, granting it resilience against isolated market shocks or restrictions while fostering network effects via social trading communities amplifying retention rates—analogous to models seen at Robinhood or Interactive Brokers but uniquely tailored for Asian investor preferences blended with Western compliance standards.

However, balance will be delicate due to China's tightening supervision on offshore securities activities potentially placing Futu's Mainland China-derived revenues under continuous pressure requiring agile relocation or re-imagined service architectures compliant with evolving regimes.

Conclusion

Futu Holdings displayed exceptional financial momentum through end-2025 driven by technology-enabled brokerage service expansion across seven international markets complemented by innovative product offerings that resonated well with retail investors seeking cutting-edge tools coupled with community interaction.

Yet sustainability faces challenges stemming predominantly from unpredictable regulatory developments emanating from Chinese authorities combined with an increasingly crowded field of competitors mobilizing extensive resources globally which may compress margins or slow user base growth unless offset through continuous technological advancement.

Investors should monitor forthcoming regulatory disclosures closely while assessing the company's execution on strategic initiatives aimed at broadening service lines beyond transactional commissions alongside prudent capital deployment balancing organic investment against shareholder returns.

Disclaimer: This analysis is intended solely for informational purposes based on available public disclosures as of April 15, 2026; it does not constitute investment advice or recommendations regarding Futu Holdings Ltd or any other securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments