American Woodmark’s Earnings Retreat Tests Strategic Merger Outlook

American Woodmark Corp's fiscal 2025 financial contraction compounds uncertainties around its pending MasterBrand merger.

American Woodmark reported a 7.5% revenue decline and operating income contraction in FY2025, with operating cash flow halving year-over-year, illustrating margin pressures amid volatile supply chain dynamics. These headwinds exacerbate risks related to the strategic merger with MasterBrand, which faces regulatory scrutiny and integration challenges. Capital allocation remains disciplined with notable share repurchases despite softer cash flows, while industry structural pressures in home furnishings weigh on growth visibility.

Revenue and Profit Trajectory Through FY2025

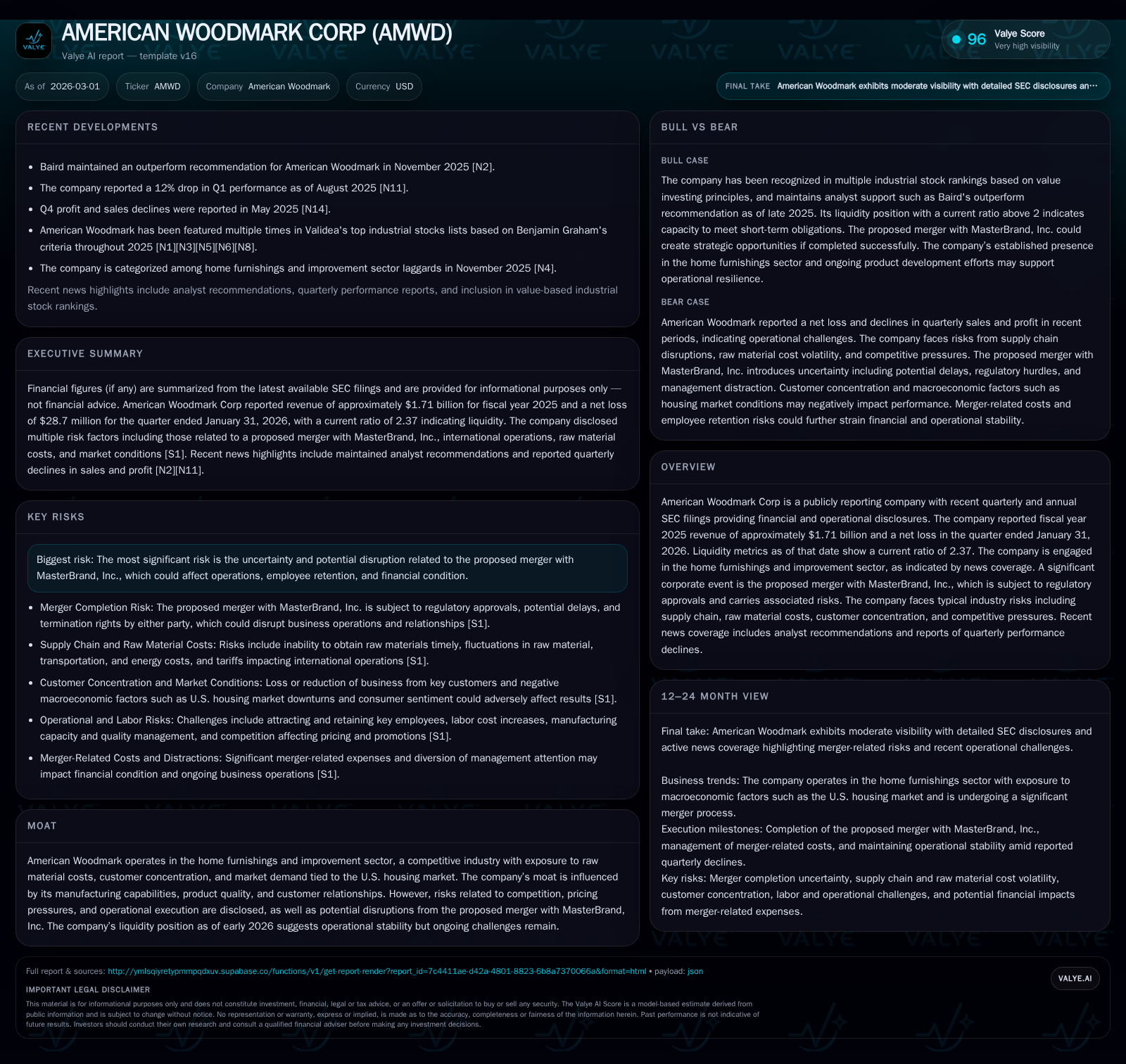

American Woodmark reported fiscal year 2025 revenue of approximately $1.71 billion, reflecting a decline of 7.5% from $1.85 billion in FY2024 [F1]. Operating income fell by 13.1% to about $140 million while net income dropped 14.4% to roughly $99 million over the same period [F1]. This marks a reversal from prior years where revenue peaked at $2.07 billion in FY2023 before the downturn.

Operating cash flow displayed acute pressure, contracting by over half (-53%) year-over-year to $108 million in FY2025 compared to $231 million previously [F1]. Capital expenditures were likewise curtailed sharply (-56%), falling to $39.7 million [F1], indicating restraint amid tightening internal liquidity.

Despite these declines, the company maintained a robust current ratio of 2.37 as of January 31, 2026, signaling adequate short-term asset coverage against liabilities [F1]. The equity base expanded gradually consistent with retained earnings accumulation [F1], supporting an approximate return on equity near 10.9% on trailing net income versus shareholders' equity.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 1.7 | 99 | 108 | 140 | -7.5% | -14.4% |

| 2024 | 1.8 | 116 | 231 | 161 | -10.6% | +24.0% |

| 2023 | 2.1 | 94 | 199 | 136 | +11.3% | +415.3% |

| 2022 | 1.9 | -30 | 24 | 36 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 97 | 69 | 10.9 |

| 2024 | 88 | 140 | 12.8 |

| 2023 | 0 | 156 | 10.7 |

| 2022 | 25 | -20 | -3.8 |

Source: SEC companyfacts cache [F1].

Table: Historical Financial Performance Summary FY2022-FY2025 [F1]

Unpacking Margin Compression Drivers in a Volatile Supply Chain

The ongoing margin deterioration stems primarily from cost push inflation affecting raw materials and energy inputs vital to cabinetry manufacturing [S2], [S6]. American Woodmark’s substantial Mexican operations introduce exposure to tariffs and fluctuating trade policies that have led to uncertain duty impositions and increased transportation costs [S2], [S4]. Such cross-border sourcing complexity compounds challenges around capacity alignment and supply chain timing.

Price promotion pressure amid heightened competition constrains pass-through pricing ability while heightened labor costs inflate operational expenses [S7]. The company cites risks associated with maintaining product quality under these conditions given intensified manufacturing alignment demands [S4], emphasizing the sensitivity inherent in value engineering within the home furnishings sector.

The MasterBrand Merger: A Catalyst or a Disruption?

The August 5, 2025 agreement for MasterBrand’s acquisition of American Woodmark stands as a pivotal strategic inflection point but also a source of acute uncertainty [S2], [S3]. Antitrust scrutiny via the FTC's Hart-Scott-Rodino second request has extended regulatory timelines, with closing expected early in calendar year 2026 contingent on approval [S16].

The pending merger poses integration risks notably around key employee retention disruptions as roles within the combined entity remain unclear during transition phases [S10], [S11]. Customer relationships risk potential erosion due to perceived instability or contract renegotiations triggered by merger proceedings [S7]. Management resources have been diverted towards negotiation efforts and compliance expenditure, detracting focus from organic growth initiatives across both firms [S12], [S13].

Litigation initiated by shareholders challenging disclosure adequacy further clouds certainty, threatening costly delays or injunctions that could alter transaction timelines or even termination prospects [S15]. Should the deal falter, protracted managerial distractions and sunk transaction costs would likely weigh negatively on operational momentum [S14].

Risks Shaping Operational and Regulatory Landscapes

Amid the domestic U.S housing market’s softening—which correlates directly with cabinetry demand—American Woodmark confronts notable customer concentration risks that magnify top-line volatility when large buyers alter purchasing cadence or negotiating leverage increases substantially [S4], [S7]. Labor cost inflation fuels margin pinch points compounded by evolving digital transformation initiatives whose execution risk threatens efficiency gains promised by platform modernization programs [S5].

Environmental regulatory compliance particularly around health & safety standards presents incremental cost burdens alongside potential reputational risk from noncompliance [S4], consistent with industry-wide trends where sustainability mandates increasingly shape capital expenditure prioritization.

Forecasting the Next Chapter: What Analysts Expect

February’s upgrade by Zelman & Associates reflects tempered optimism hinging upon successful merger closeout and stabilization post-integration disruption risks offsetting near-term earnings softness tied to macroeconomic factors such as mortgage rates impacting consumer remodeling activity [N1]. Management guidance per latest SEC filings underscores continued caution citing ongoing cost inflation pressures but anticipates gradual synergies realization conditional on timely FTC clearance [S2].

Key performance indicators moving forward will encompass monitoring merger milestone achievements including antitrust approval progress alongside volatility in housing market activity—given its outsized influence on cabinet sales volume and backlog development.

Capital Deployment: Cash Flow, Buybacks, and Dividend Considerations

American Woodmark’s ROE approximated at about 10.9% during FY2025 reflects reasonable profitability amidst sales contraction paired with controlled capital structure employing equity levels just above $915 million [F1]. Free cash flow generation remains positive but tempered at roughly $68.7 million after subdued capital expenditure outlays consistent with capex restraint taking precedence over growth investments amid cautious outlooks [F1].

Remarkably, share repurchases accelerated to nearly $96.7 million in the latest year after minimal buyback activity in prior years, signaling an emphasis on returning capital via stock retirements rather than dividend distributions which have been inactive for over a decade now according to historical data up to FY2014 [F1]. This approach suggests management prioritizes enhancing shareholder value through EPS accretion amid current earnings challenges.

Strategic Positioning in Home Furnishings Amid Industry Headwinds

American Woodmark’s moat is anchored by integrated manufacturing capabilities allowing tight quality control and customization flexibility that underpins long-standing customer partnerships—key differentiators in a commoditized cabinetry market sensitive to channel mix dynamics involving big-box retailers versus specialized contractors.

That said, rising price elasticity due to intensified competition both domestically sourced and foreign manufactured limits pricing power exacerbated by increasing customer buying clout requiring tactical value engineering adaptations without eroding brand perception further squeezing margins.

Operational execution excellence during this turbulent period will be tested heavily as maintaining capacity alignment amidst unpredictable input costs becomes paramount alongside digital platform upgrades aimed at bolstering order fulfillment responsiveness.

Conclusion: Balancing Growth Ambitions with Tactical Prudence

American Woodmark enters fiscal year 2026 grappling with tangible earnings retreat driven by multifaceted margin compression exacerbated by macroeconomic housing softness—a confluence that intensifies scrutiny on the transformative MasterBrand merger’s strategic rationale and execution viability.

The success or failure of this merger holds disproportionate sway over the company's medium-term trajectory given potential synergies but also material integration risks that threaten near-term operational continuity.

Prudent stakeholders will closely follow regulatory progressions, integration management effectiveness, and sector-specific demand signals derived from U.S housing metrics while assessing how capital deployment priorities balance growth investments versus shareholder returns amid this crescendo of transitional uncertainty.

This analysis synthesizes publicly reported financial data alongside SEC disclosures and recent news without providing investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments