Aterian’s Profitability Struggles Intensify Under Tariffs and Operational Dependencies

Aterian operates consumer brands primarily on Amazon, facing mounting cost pressures and strategic uncertainty amid persistent losses.

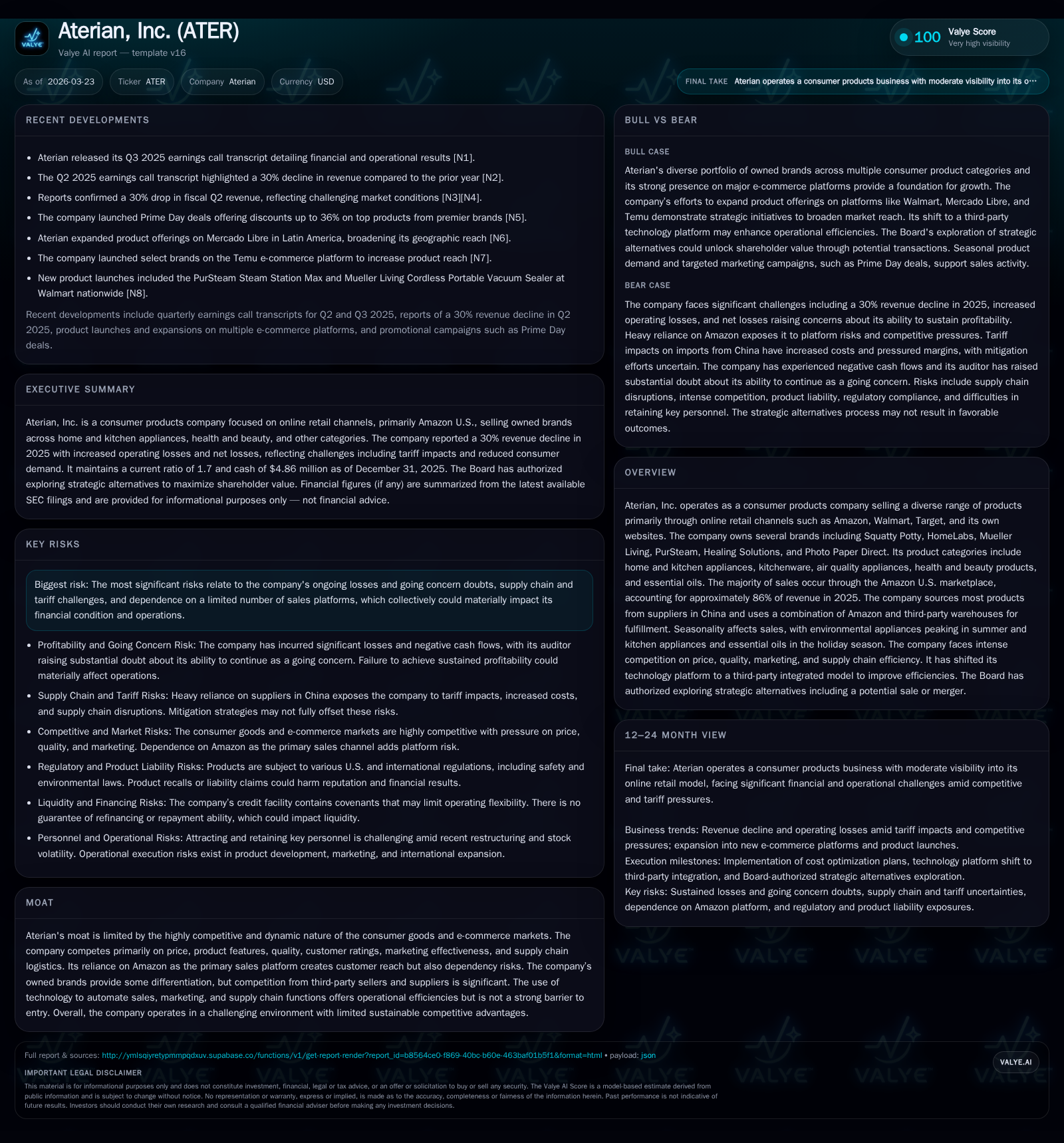

Aterian, Inc. revenues rely heavily on Amazon U.S. marketplace sales, with its portfolio of consumer product brands exposed to seasonal fluctuations and intense competitive pressure. The company continues to struggle with significant losses and negative cash flow, exacerbated by rising U.S. tariffs on imports from China where most of its products are sourced. Despite mitigation efforts including price increases, cost control initiatives, and supply diversification, Aterian’s financial position remains strained with material doubts about its going concern status raised by auditors. The credit facility covenant amendments and recent workforce reductions underscore ongoing liquidity challenges while a strategic review process signals potential corporate changes ahead.

Business Overview

Aterian, Inc. is a consumer products company focused primarily on online retail channels such as Amazon U.S., Walmart.com, Target.com, and direct-to-consumer websites. Its portfolio includes owned brands like Squatty Potty, HomeLabs, Mueller Living, PurSteam, Healing Solutions, and Photo Paper Direct spanning categories from home and kitchen appliances to health and beauty products.[S1][S16] Revenue generation depends heavily on Amazon.com — comprising about 86% of total sales in 2025 — establishing significant platform dependency risk.[S1] Despite a geographically distributed supply chain presence including offices in New Jersey (headquarters), China, the Philippines, and the UK, most finished goods inventory is sourced from approximately 33 suppliers located predominantly in China.[S16]

Historical Performance

Financially, Aterian exhibits persistent operational challenges. The latest full fiscal year ended December 31, 2025 shows:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -19 | -11 | -18 | 51000 | -60.0% |

| 2024 | -12 | 2 | -12 | 42000 | +84.1% |

| 2023 | -75 | -13 | -76 | 119000 | +62.0% |

| 2022 | -196 | -17 | -178 | 595000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -11 | -124.8 |

| 2024 | 2 | -39.5 |

| 2023 | -14 | -206.9 |

| 2022 | -18 | -192.5 |

Source: SEC companyfacts cache [F1].

Net losses widened roughly 60% year-over-year while operating income declined approximately 52%. Operating cash flows turned sharply negative after positive inflows in the prior year.[F1] Capital expenditures remain minimal relative to operations.

The cumulative deficit stood at about $730 million as of end-2025.[F1] Return on Equity is deeply negative at about -125%, reflecting sustained unprofitability against dwindling equity bases ($15.21 million at end-2025 vs $30 million prior year).[F1]

Tariffs and Supply Chain Impact

The imposition and expansion of U.S. tariffs on imports from China during calendar year 2025 materially increased Aterian's cost base for goods sold.[S1][S23] To offset these costs, targeted pricing strategies were implemented which negatively affected consumer demand leading to declining unit volumes.[S18] The company actively mitigated tariff impact through supplier negotiations, reengineering products to reduce exposure, diversifying sourcing away from China where feasible, and selective price increases; however substantial uncertainty remains regarding efficacy.[S15][S18]

Further complexity stems from varying tariff regimes: In late 2025 a new one-year agreement lowered certain tariffs on Chinese goods by ten percentage points but maintained reciprocal baseline tariffs around 10%. Early in 2026 the U.S. Supreme Court invalidated certain tariff statutes retroactively impacting duties paid by Aterian but left open timing and realization of refunds.[S25] Concurrently a new temporary global tariff came into effect in February 2026 introducing fresh cost considerations.

Aterian's supply chain relies heavily on Chinese manufacturers covered under export credit insurance from Sinosure (a state-owned enterprise). Payment delays previously resulted in reduced insurance availability causing operational risk concerns.[S10][S16]

Seasonality & Product Mix Effects

Sales performance exhibits strong seasonality influenced by product categories: environmental air quality appliances experience peak sales during summer months while small kitchen appliances and essential oils see holiday season spikes notably in Q4 (Thanksgiving-December).[S1][S19]

This cyclicality affects working capital needs due to fluctuating inventory levels and storage costs across quarters.

Competitive Environment & Moat

Aterian operates within highly dynamic consumer goods e-commerce markets characterized by intense competition from branded suppliers as well as third-party sellers across marketplaces.[S1][S20]

Competitive edges derive mainly from pricing strategies, product design/features innovation, maintaining quality standards to support positive customer reviews/ratings, effective digital marketing spend allocation (primarily via Amazon affiliates), visibility within crowded platforms, logistical efficiencies including fulfillment certifications (FBM One Day & Two Day Prime certification achieved), and rapid delivery capabilities leveraging mixed warehouse networks.[S20][S19]

However these factors grant limited sustainable differentiation or barrier to entry given ease for multiple sellers to compete directly online.

Liquidity & Capital Structure

As of December 31, 2025 Aterian reported $4.9 million cash equivalents with total current assets around $24 million compared against current liabilities near $14 million yielding a current ratio of approximately 1.7x — moderate liquidity coverage but amidst ongoing cash burn.[F1]

The company maintains a senior secured revolving credit facility with MidCap Funding IV Trust originated December 22, 2021 initially sized at up to $40 million subject to borrowing bases tied primarily to inventory & receivables.[S6][S12] Amendments between February 2024 and March 2026 repeatedly relaxed financial covenants particularly minimum liquidity requirements:

- From peak $15 million down to a staged reduction ending currently at $3.5 million minimum liquidity requirement subject to weekly extension options through May 9, 2026.[S4][S7][S26]

- Share repurchase programs authorized up to $3 million but temporarily suspended as of May 2, 2025 due to liquidity constraints.[S26]

- Long-term maturity extended through December 2026 with variable interest linked primarily to SOFR plus margin spreads totaling about ~5.6% plus fees.[S6]

Despite repeated covenant relief measures the company discloses material uncertainty regarding its ability to maintain compliance absent improved cash flows or external capital raising which is not guaranteed.[S9][S14][S21][F1]

Restructuring Initiatives & Cost Controls

In response to financial pressures management announced fixed cost reduction plans:

- May 14, 2025 workforce reduction eliminating approximately 20 employees completed by year-end with associated restructuring charges near $1.9 million recognized mainly in sales/distribution and G&A expenses involving severance payouts extending into Q2-2026.

- January 2026 additional workforce cuts removing about sixteen employees/contractors anticipated completed by Q1-2026 tracking restructuring costs around $0.3 million expected in same quarter.[S25]

Alongside SKU rationalization efforts focusing future sales on core visually differentiated or profitable products aim at improving gross margins and contribution margins over time.[S9][S25]

Strategic Initiatives & Outlook

In December 2025 Aterian’s Board authorized exploration of strategic alternatives including sale or merger transactions intending to maximize shareholder value though timing remains undefined and outcomes uncertain.[S1]

The company's long-term success hinges critically on developing new product iterations across categories successfully scaling sales internationally beyond established domestic reliance largely on Amazon U.S., achieving meaningful margin improvements amid cost headwinds including tariffs plus inflationary pressures plus judicious management of cash burn levels given elevated debt leverage requires maintaining covenant compliance.

Monitoring points going forward include quarterly revenue trends reflecting demand resilience post pricing adjustments amid macroeconomic consumer discretionary spending shifts; progress toward supplier diversification reducing burden from China exposures; fulfillment efficiency gains especially balancing FBM versus FBA models impacting per unit shipping costs; legal resolutions surrounding recent voluntary recall related litigation affecting PurSteam products; as well as any further amendments or refinancing activities addressing liquidity needs beyond maturity horizon.

Risk Considerations Summary

Key risks outlined confirm substantial operational fragility:

- Persistent net losses erode equity base risking solvency concerns flagged explicitly by independent auditors questioning going concern assumptions.[S2][F1]

- Sensitive exposure to trade policy swings due tariff regimes notably vis-à-vis China where product sourcing concentrates raising input cost volatility.

- Critical dependency on Amazon marketplace constraining channel diversification with revenue concentration risk exceeding peer benchmarks common in e-commerce retail models but still notable vulnerability.

- Potential liabilities from product safety complaints/recalls/litigation adding unpredictable financial strain.

- Tight liquidity position underscored by minimal unrestricted cash buffers coupled with covenant dependent credit facility requiring ongoing renegotiations/waivers.

Summary

Aterian operates an e-commerce centric consumer brand business heavily anchored via Amazon U.S., offering diverse household staples under proprietary brands but plagued by chronic unprofitability exacerbated recently by external trade duty shocks inflating costs during an already challenging macro backdrop for discretionary retail consumption. Continuous losses aggregate steeply placing heavy reliance upon mitigating actions ranging from tariff counter strategies through workforce optimization paired with capital structure adjustments narrowing breathing room. The initiation of a strategic alternatives review signals recognition at the Board level that organic recovery alone may be insufficient without transformative transaction(s). Financial discipline balancing growth aspirations against rigorous expense control will define near-term trajectory as investor patience faces tests amid market uncertainties surrounding margins sustainability alongside entering cycles whereby operational scale gains remain elusive thus far. Ultimately Aterian stands as a cautionary illustration of mid-cap digital-first consumer products enterprises contending with intensifying margin compression caused by geopolitical tariff upheavals combined with platform concentration paradoxes common among fast scaling e-commerce retail ventures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments