Vertical Aerospace Accelerates Prototype Testing Amid Capital Constraints and Competitive Pressures

The UK-based eVTOL pioneer advances aircraft certification steps while managing liquidity risks and evolving partnerships.

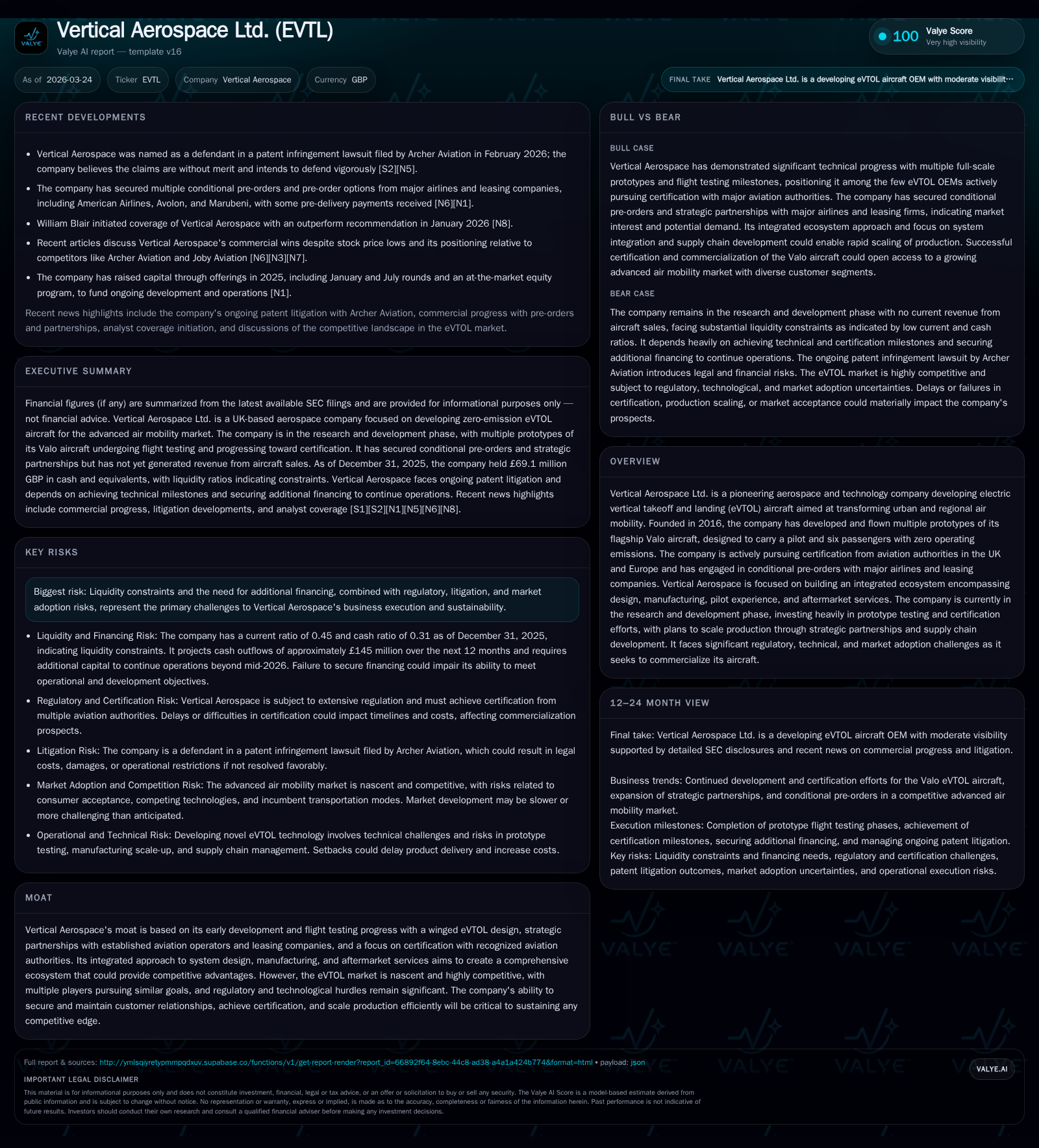

Vertical Aerospace Ltd. remains a front-runner in electric vertical takeoff and landing (eVTOL) innovation, pushing forward with multiple prototype flight tests of its Valo aircraft while targeting safety certifications with UK and European authorities. Despite not yet generating revenue, the company has secured conditional pre-orders from major airlines and leasing firms, underpinning future commercialization ambitions. However, significant capital expenditures, rising R&D expenses, and litigation pressures highlight risks to its financial runway. Close monitoring of certification milestones, financing access, and regulatory progress will be essential to gauge the trajectory of this emerging aerospace player.

Company Background and Strategic Vision

Founded in 2016, Vertical Aerospace Ltd. is positioned at the forefront of the nascent electric vertical takeoff and landing (eVTOL) aircraft sector. The company's flagship product, Valo, aims to revolutionize urban and regional air mobility by providing pilot-driven zero-emission transport for a pilot plus six passengers. Vertical Aerospace's strategic differentiation lies in its winged eVTOL design—a hybrid between helicopter agility and fixed-wing efficiency—and its active pursuit of simultaneous certification with both the UK Civil Aviation Authority (CAA) and European Union Aviation Safety Agency (EASA) [S1].

The company emphasizes an end-to-end ecosystem approach encompassing not only aircraft design and manufacturing but also pilot experience, aftermarket services, and integration with established aviation operators. This comprehensive stance seeks to lower entry barriers for customers and establish long-term client relationships within the advanced air mobility (AAM) market segment [S6][S21].

Historical Performance and Operating Results

Vertical Aerospace remains pre-commercial with no reported revenues from sales or operations as of December 31, 2025. The reported revenue figure of £132k reflects negligible activity for FY2021 through FY2023 without material changes thereafter [F1][S7]. Consequently, all operating expenses have been associated with research and development (R&D) activities—covering staff costs, engineering consultants, testing consumables—and administrative overheads supporting increasing organizational scale.

The company’s net income trajectory reflects an improving but still challenging path: a record net loss of -£781 million was recorded in FY 2024 before improving sharply to a reported net income of £233 million in FY 2025 [F1]. This positive bottom line is likely influenced by non-operational gains such as changes in fair value accounting on convertible notes or one-time contract settlements (e.g., termination payment from Rolls-Royce totaling $34 million recognized in prior periods) rather than cash-positive operational performance [S10][S11][S12][S26]. Equity remains in deficit territory at -£121.4 million as of year-end 2025 reflecting accumulated losses weighted against capital raises [F1].

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|

| 2025 | 233 | +129.8% | ||

| 2024 | -781 | -1203.2% | ||

| 2023 | 132000 | -60 | 0.0% | +36.5% |

| 2022 | 132000 | -94 | 0.0% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -191.8 |

| 2024 | 156.5 |

| 2023 | 120.4 |

| 2022 | -1289.6 |

Source: SEC companyfacts cache [F1].

Net cash used in operating activities more than doubled from £46.3 million in 2024 to £82.8 million in 2025 driven predominantly by ramped-up R&D spend on prototype development and testing along with administrative growth due to scaling operations. Financing activities provided sustained support through significant equity offerings totaling over £197 million across January and July 2025 rounds plus ongoing ATM sales agreements ensuring sufficient near-term liquidity [F1][S13][S16].

Research & Development Progress

Flight tests of Valo prototypes have proceeded steadily since late 2022 reaching critical technical milestones including piloted thrustborne maneuvers by January 2025 and wingborne flight tests commencing May 2025. To accelerate knowledge acquisition and refinement, assembly of an identical third prototype was completed at end-2025 enabling parallel testing streams designed to compress certification timelines projected around 2028 [S1][S15].

Vertical Aerospace invests heavily in proprietary technology development such as custom battery systems and propeller designs while leveraging select partnerships for core components. The strategic alliance established with Evolito Ltd., which holds a Design Organisation Approval critical for CAA certification eligibility, strengthens propulsion system development where Evolito provides electric propulsion units targeting redundant architectures capable of satisfying stringent airliner-grade safety requirements [S3].

The company retains a robust Design Organisation Approval (DOA) encompassing expanding technical domains like avionics and electrical systems approved by the CAA followed by concurrent validation efforts via EASA; reinforcing regulatory alignment between UK and EU aviation bodies post-Brexit [S1]. This regulatory positioning could facilitate accelerated global acceptance including by FAA (US), ANAC (Brazil), JCAB (Japan) among others.

Commercial Outlook & Market Engagement

Though not yet generating sales revenue, Vertical Aerospace has secured conditional pre-orders representing several hundred aircraft placements from major airlines (e.g., American Airlines), leasing companies like Avolon, helicopter operators such as Bristow Group, Japanese industrial trader Marubeni Corp., alongside tourism operators and mobility platforms globally [S6][S15][N6].

These arrangements typically involve conditional commitments pending final purchase agreements alongside refundable pre-delivery payments that afford some visibility into future demand while mitigating risk exposure should certification timelines or product performance deviate materially from plans. The ability to convert these orders into legally binding contracts with upstream payments will be pivotal for project financing through production scale-up phases.

Simultaneously Vertical Aerospace pursues market expansion beyond traditional helicopter replacements into cargo/logistics sectors where hybrid-electric variants announced in mid-2025 seek to triple payloads up to over one ton over extended ranges exceeding one thousand miles — potentially opening defense logistics or emergency medical transport avenues that conventional battery-limited eVTOLs cannot serve effectively today [S1].

Industry Competition & Risk Factors

The advanced air mobility sector is busy with multiple well-funded competitors including Joby Aviation, Archer Aviation (involved currently in litigation against Vertical Aerospace alleging patent infringements), Lilium GmbH among others vying for early commercial footholds globally [N2][N3][N4][N5][N6].[S18] Vertical faces substantial challenges not only technological but also regulatory given the novelty of eVTOL certification frameworks—these can induce costly delays or extended timelines impacting market entry.

Financially, the company must judiciously manage capital given high burn rates on R&D coupled with contingent contracts that require upfront investment while revenue streams remain elusive.[F1] The Convertible Senior Secured Notes impose covenants requiring minimum cash thresholds which may be compromised absent further fundraises scheduled possibly through equity issuance programs totaling $100 million under ATM arrangements.[S14][S16][S19]

Capital Allocation & Financial Positioning

Vertical Aerospace’s capital allocation reflects heavy prioritization towards R&D accelerating prototype maturation evidenced by a roughly 20% increase in related expenses year-over-year reaching approximately £72M for fiscal year ending December 31, 2025; administrative costs rose commensurately due to personnel scaling and compliance overheads tied to regulatory requirements.[S12][S26]

Financing strategies have leveraged public equity markets extensively during FY25 raising over $150 million across two major offers backed partially by Mudrick Capital commitments.[S11][S13] While no dividends or share buybacks are planned consistent with developmental stage status there is an emphasis on maintaining sufficient liquidity buffers amid macroeconomic uncertainty.[F1]

Despite reported net income improvement in FY25 highly influenced by noncash factors actual operational cash flow remains negative indicating ongoing reliance on external capital to sustain operations until commercial production becomes viable.[F1]

What To Watch Next: Analysis Perspective

Key near-term indicators include flight test program progression benchmarks especially successful operating envelope expansions signifying reduced risk towards target certifications scheduled post-2027.[S15]

Monitoring balance sheet metrics—principally cash balances versus covenant obligations—to assess liquidity stress points will be essential as the potential breach mid-2026 could trigger acceleration clauses affecting debt servicing capacity.[S16][S19]

Legal developments regarding ongoing patent litigation initiated by Archer may influence cost structures or distract management focus impacting delivery timelines.[N2]

Further expansions or contractions in pre-order pipelines reflective of growing customer confidence or market hesitation amid elevated valuations could signal underlying commercial viability trends.[N6]

Finally broader regulatory environment shifts such as FAA acceptance of UK/EASA certifications or infrastructure advancements tied to vertiport rollouts across metropolitan areas will influence overall demand dynamics.

Conclusion

Vertical Aerospace exemplifies the pioneering spirit defining the burgeoning eVTOL industry rooted in advanced aerospace expertise and substantial governmental collaboration focused on ultra-safe zero-emission air travel solutions. Having achieved notable technical milestones advancing multiple prototypes into piloted wingborne flight phases paired with establishing critical supplier partnerships lends credibility to their commercialization roadmap targeting certificate attainment circa 2028.

Nonetheless significant execution risks persist with high capital intensity operating purely within development cycles without recurring revenues compounded by regulatory complexity alongside competitive encroachment within this accelerating space.[F1][N2] Investor focus logically revolves around flight test outcomes validated by independent certifying bodies alongside sustainable capital access facilitating uninterrupted developmental momentum.

This report draws exclusively on publicly available information from SEC filings dated March 24, 2026 ([F1],[S#]), recent news articles ([N#]), and established industry knowledge as distinct from any model-based forecasts or subjective investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments