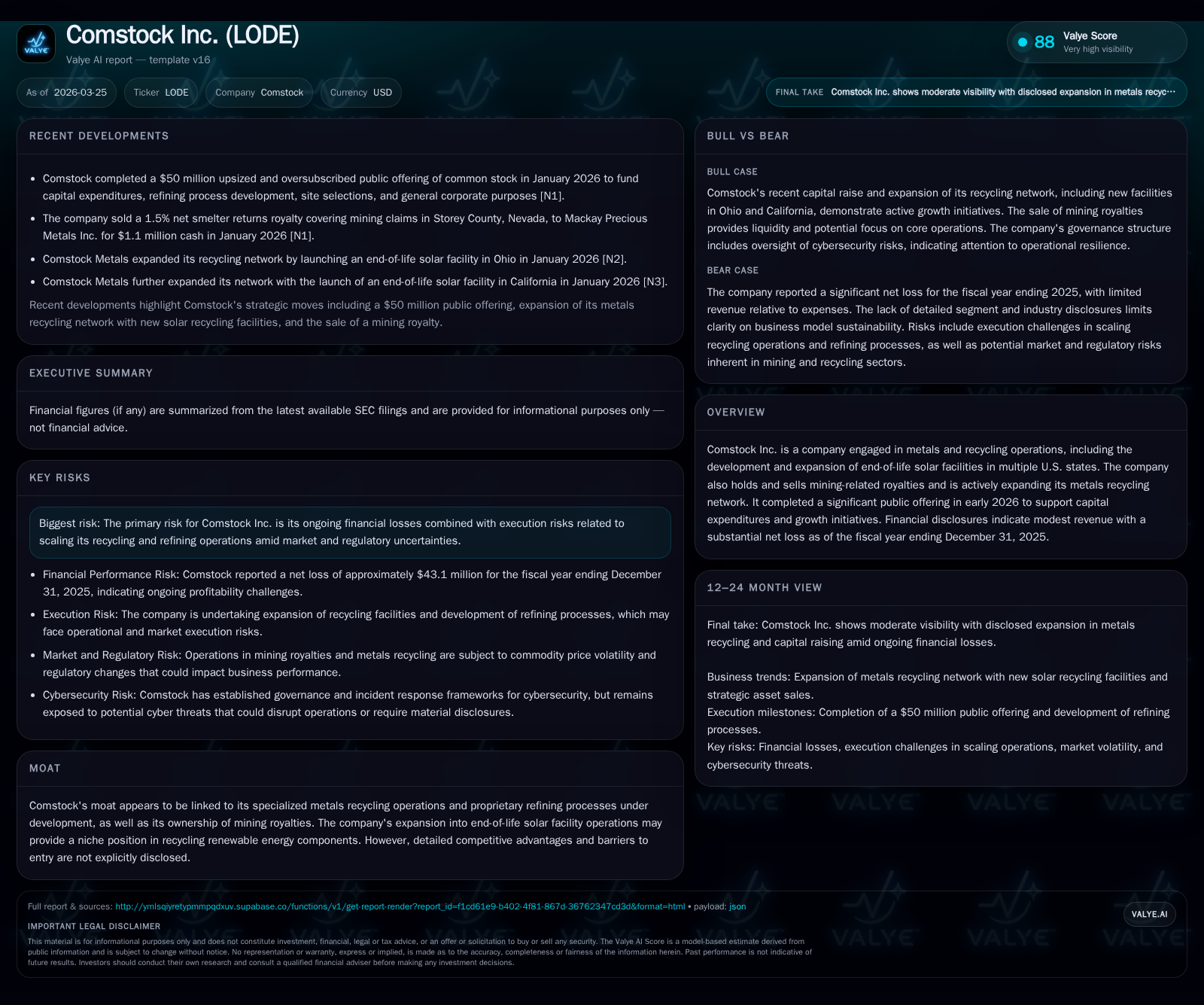

Comstock Inc.’s Metals Recycling Expansion Struggles Amid Steep Losses

Comstock Inc. pursues growth in metals recycling and end-of-life solar operations while contending with persistent financial deficits and operational scaling risks.

Comstock Inc. has steadily expanded its metals recycling and renewable solar component recovery segments, supported by a $50 million capital raise completed in early 2026. Despite modest revenue generation, the company continues to face substantial net losses exacerbated by costly refinery development and site expansion efforts. Its balance sheet shows reasonable liquidity and manageable debt levels, but reliance on equity financing and director stock compensation introduces dilution risks. Investors should monitor the company’s ability to translate scale-up investments into improved cash flow and operational stability amid a complex regulatory landscape.

From Modest Revenues to Heavy Operating Losses: Comstock’s Recent Performance

Comstock Inc.’s historical financial profile reveals a company deeply engaged in building capacity within highly specialized metals recycling fields but yet to achieve profitability. Annual revenues have fluctuated modestly with FY2025 reporting approximately $1.55 million—a steep decline from roughly $3.02 million in FY2024, indicating either a transitional product mix or timing shifts in contract fulfillment [F1]. Earlier years saw even lower revenues as the company ramped its operations.

Operating income illustrates an unrelenting pattern of large deficits: a $38.1 million loss in FY2025 was marginally better than the nearly $39.7 million loss registered the year before but far from breakeven territory [F1]. Net income losses mirror this trend; despite a reduction relative to FY2024’s $53.3 million deficit, the FY2025 loss remained substantial at about $43.1 million [F1]. This translates into a negative approximate Return on Equity hovering near -40%, underscoring that equity capital has not yet generated positive returns [F1].

Operating cash flows show increasing strain consistent with expanding scale efforts: CFO deteriorated 74.9% year-over-year to negative $24.4 million driven largely by significant capital investments in industrial metal recovery infrastructure [F1]. The bulk of capital expenditures occurred over recent years as refineries transitioned from pilot phases toward industry-scale operations.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 2 | -43 | -24 | -38 | -48.5% | +19.2% |

| 2024 | 3 | -53 | -14 | -40 | -606.6% | |

| 2023 | 11 | -14 | -13 | +122.5% | ||

| 2022 | -47 | -12 | -19 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -40.0 |

| 2024 | -89.2 |

| 2023 | 13.4 |

| 2022 | -87.2 |

Source: SEC companyfacts cache [F1].

Note: Capital expenditures for recent years are not fully disclosed in the available data set; outlier capex figure from CY2018 suggests early-stage investment focus.

Evaluating Key Growth Drivers and Headwinds in Metals Recycling and Solar Facility Operations

Comstock's operations revolve around metals recycling with a core concentration that increasingly includes end-of-life solar module processing across U.S regions—an emerging niche responding to the accelerating photovoltaic (PV) waste stream challenge. The company’s proprietary refining processes under development are positioned as critical enablers for enhanced metal recovery efficiencies from complex feedstocks typical of solar panels and other electronic scrap sources [N1][S13].

However, these advanced refining technologies remain at various stages of scale-up requiring substantial R&D expenditure and operational integration efforts that contribute heavily to overheads and sustained losses [S13]. Moreover, the complexity intrinsic to processing heterogeneous waste streams alongside fluctuating market demand for recovered metals pushes operational scalability challenges into focus.

Regulatory uncertainty compounds these headwinds: stringent environmental compliance regimes governing recycling processes and the nascent regulatory frameworks for PV module end-of-life treatment introduce variability in operational costs and permitted processing methods [S13]. Such dynamics could delay ramp timelines or require further capital deployment for compliance adaptation.

2026 Capital Raise: Deployment Plans and Growth-Enabling Investments

In late January 2026, Comstock completed a material equity financing raising gross proceeds of approximately $50 million through a public offering of over 18 million shares plus additional warrant instruments exercisable after six months at $3.16 per share strike price [S5][S6][S17].

The net proceeds are earmarked primarily to finance capital expenditure commitments for the construction of Comstock Metals LLC’s second industrial-scale recycling facility—aimed at augmenting volumetric throughput—and continued development of its proprietary refining solution aimed at boosting metal recovery yields [S5][S6]. Additional allocations include accelerated site identification activities and general corporate purposes that may encompass working capital needs against ongoing operating deficits.

The underwriting warrants issued alongside the offering introduce potential dilution risk dependent on future exercise activity which management has locked up for an initial period post-issuance [S5]. This structure reflects both investor appetite constraints for purely common stock issuance and strategic intent to preserve long-term incentivization mechanisms.

Financial Snapshot: Liquidity Position, Debt Profile, and Capital Structure Changes

As of December 31, 2025, Comstock reported cash and cash equivalents totaling approximately $16.95 million against current liabilities of about $10.0 million yielding a healthy current ratio near 2.06—a sign that short-term obligations can be met without immediate refinancing concerns [F1][S7][S10].

While detailed long-term debt disclosures confirm absence of incremental leverage escalation over recent periods indicating conservative approach to external debt financing relative to equity expansion initiatives , operating cash outflows remain pronounced reflecting continued burn tied to plant construction and technology development.

Equity base experienced significant growth from approximately $59.8 million at end-2024 to roughly $107.6 million at end-2025 reflecting successful capital raises including the January 2026 public offering executed shortly after fiscal year-end closing [F1]. The disparity between fiscal-year-end equity figures and early-2026 issuance is due to registration statement timing rather than overlapping accounting periods.

Shareholder Returns: Absence of Dividends Amid Equity-Based Compensation Strategies

Consistent with an early-phase industrial growth profile characterized by heavy reinvestment needs and ongoing operating losses, Comstock does not pay dividends nor conduct share repurchase programs presently—supported by SEC filings spanning late-2025 into early-2026 [S4][S8][S9][S11].

An additional notable element is director remuneration largely denominated via equity grants with issuances aggregating several hundred thousand shares across non-employee board members covering multi-year service periods up to March 2026 [S4]. Quarterly stock-based payments aim at bolstering director alignment with shareholder interests but inevitably result in share count dilution impacting metrics such as Earnings Per Share (EPS) should profitability emerge.

Risks on the Horizon: Execution, Market, and Regulatory Challenges Ahead

Comstock’s most prominent disclosed risk relates principally to the execution challenges inherent when scaling new metals recovery technologies from pilot scales toward full industrial capacity while maintaining cost controls amidst market fluctuations for secondary metal commodities [S13].

Given the company's formative status in its solar facility recycling program—a relatively novel segment within sustainable resource recovery—the regulatory environment remains unsettled around standards applicable to end-of-life PV modules potentially resulting in compliance cost volatility or operational delays as protocols evolve regionally across U.S jurisdictions.

Furthermore, cybersecurity governance receives specific mention given Comstock's information systems oversight framework which integrates incident response protocols led by senior financial officers ensuring preparedness against potential cyber threats—a reflection of modern operational risk awareness though tangentially impacting direct business metrics [S13].

What To Watch Next: Potential Milestones and Metrics Indicating Change

While explicit management guidance on future milestones is sparse beyond use-of-proceeds statements related to capital projects [S5], investors should monitor several key indicators indicative of operational transition:

- Revenue trajectory stabilization or reversal of recent declines signaling improved volume throughput or sales mix enhancement;

- Progress reports related to commissioning timelines or capacity utilization rates at Comstock Metals LLC’s second industry-scale facility;

- Updates concerning proprietary refining process pilot results transitioning into commercial application;

- Changes in operating cash flow trends toward less negative or positive conversion as capital spending cycles mature;

- Regulatory developments impacting renewable energy scrap processing sectors influencing permitting or compliance cost structures.

These metrics will be vital barometers demonstrating whether investments made during loss periods catalyze sustainable operational advancement.

This analysis relies strictly on publicly filed financial disclosures ([F1],[S#]) without forecasting future results or providing investment recommendations. Readers should consider market dynamics independently when interpreting Comstock Inc.’s complex developmental stage within metals recycling sectors.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments