Intrusion Inc.’s Revenue Growth Amid Financial Challenges and Concentrated Market Focus

Intrusion relies on proprietary threat intelligence and a concentrated government customer base, facing ongoing financial pressures and competitive challenges.

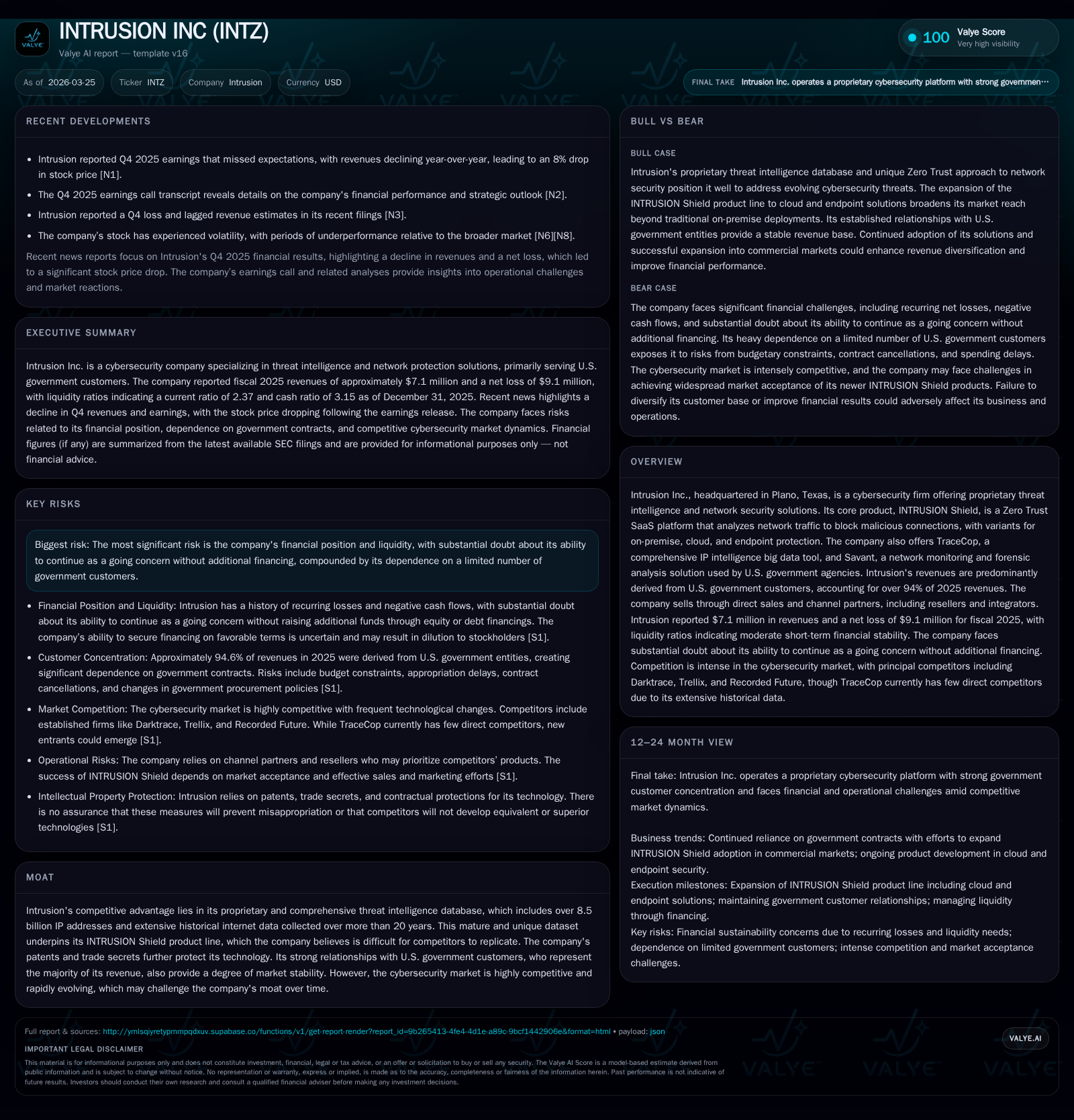

Intrusion Inc., a cybersecurity company focused primarily on U.S. government clients, reported revenues of $7.0 million in 2025, up from $5.8 million in 2024, alongside a net loss of $9.1 million. The company’s growth is tempered by heavy revenue concentration in four government customers and liquidity constraints that raise substantial doubt about its going concern status. Intrusion’s INTRUSION Shield platform leverages a unique threat intelligence repository accumulated over two decades, providing a differentiated Zero Trust solution. However, competition from larger firms and slow commercial adoption pose challenges to scaling beyond its core market. Key factors to monitor include revenue progression, contract renewals within government accounts, and access to capital markets.

Historical Financial Performance

Intrusion Inc.'s financial results for fiscal year 2025 reflect moderate revenue growth accompanied by increased losses and cash burn [F1]. Revenues rose approximately 22% from $5.8 million in 2024 to $7.0 million in 2025. Despite this top-line improvement, operating income deteriorated by about 8.5%, reaching a loss of $9.16 million, while net losses expanded roughly 16% to $9.06 million [F1]. Operating cash flow continued negative trends at -$6.76 million, a decline of 7.4% year-over-year during rising capital expenditures which increased by nearly 46% to $777 thousand [F1]. These figures underscore the operational challenges faced as Intrusion invests in expanding its platform within a competitive cybersecurity landscape.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -9 | -7 | -9 | 777000 | -16.3% |

| 2024 | -8 | -6 | -8 | 533000 | +43.9% |

| 2023 | -14 | -8 | -12 | 157000 | +14.4% |

| 2022 | -16 | -13 | -16 | 307000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -8 | -124.5 |

| 2024 | -7 | -124.6 |

| 2023 | -8 | 145.4 |

| 2022 | -13 | 385.0 |

Source: SEC companyfacts cache [F1].

Note: Revenue data prior to FY2024 is not disclosed.

Customer Concentration and Revenue Composition

A defining characteristic of Intrusion's business is its reliance on U.S. government contracts, which constituted approximately 94.6% of total revenue in fiscal year 2025, up from about 83.8% in the previous year [S6]. Revenues derive both directly from federal agencies and indirectly through system integrators, value-added resellers (VARs), and other channel partners [S4]. Four key government customers account for the majority of sales, with three individually contributing more than 10% each [S5]. This concentration presents risks related to budget fluctuations, contract cancellations without penalty, seasonal procurement cycles, and political or economic uncertainties impacting government spending patterns [S6][S17].

Export sales remain minimal at under three percent of revenue, indicating limited international diversification [S4]. The company's order backlog is modest with an immaterial non-cancellable portion [S5]. Channel partners are critical for go-to-market efforts but operate under non-exclusive agreements that may prioritize competitors’ products [S4].

Proprietary Technology: INTRUSION Shield Suite

Central to Intrusion's competitive positioning is its INTRUSION Shield platform—a Zero Trust reputation-based Software as a Service (SaaS) solution that inspects network traffic at the packet level using source/destination IP addresses, domain data, port usage, and cross-references against its proprietary threat intelligence database amassed over more than two decades covering over 8.5 billion IP addresses [S18],[S26]. This approach enables detection of zero-day exploits and sophisticated malware often missed by traditional signature-based firewalls.

The product suite includes multiple deployment options: on-premise hardware behind firewalls; cloud-focused solutions protecting Infrastructure-as-a-Service (IaaS), Platform-as-a-Service (PaaS), Software-as-a-Service (SaaS), and serverless environments; as well as endpoint protection extending coverage for mobile workers and remote devices [S26]. Complementary offerings include TraceCop, an IP intelligence big data tool, and Savant, a forensic network analysis solution used predominantly by government entities featuring customizable automated rulesets for anomaly detection [S14].

The company holds patents protecting core technologies and relies on trade secrets safeguarded through non-disclosure agreements [S14]. Despite these advantages, intense competition from better-funded incumbents such as Darktrace, Trellix, and Recorded Future requires ongoing innovation to maintain differentiation [S9][S21].

Liquidity Profile and Capital Allocation

As of December 31, 2025, Intrusion held cash and cash equivalents totaling $3.62 million against current liabilities of approximately $1.79 million for a current ratio near 2.37 [F1]. However, recurring negative operating cash flows (-$6.76 million) combined with capital expenditures ($777 thousand) result in an approximate free cash flow deficit of $7.54 million for the year [F1], underscoring liquidity constraints.

The company has depended on equity financings including a registered direct offering raising $7 million and proceeds from standby equity purchase agreements recorded previously at $1.5 million to fund operations during fiscal year 2025 [S1][S25][F1]. No dividends or stock buybacks have been declared historically or are planned in the foreseeable future given the focus on preserving capital for operations and product development [S20][F1][S27].

An auditor’s going concern explanatory paragraph highlights substantial doubt regarding the company's ability to continue absent additional financing or strategic alternatives [S1][S22]. Regulatory limitations related to public float size restrict issuance capacity under Form S-3 registration statements further complicating capital access [S16].

Competitive Landscape

Intrusion operates within an intensely competitive cybersecurity market where rivals benefit from greater financial resources, broader customer bases, stronger brand recognition, and more comprehensive product suites [S9][S21]. Competitors such as Darktrace leverage AI-driven behavioral analytics while Recorded Future offers extensive ecosystem integrations.

Intrusion's primary moat is its proprietary historical threat data repository accumulated over decades—a barrier difficult for competitors to replicate—but this advantage must be continuously reinforced through innovation given dynamic cyber threats and rapid technological evolution [S14][S26].

Outlook and Strategic Focus

Management aims to expand INTRUSION Shield adoption beyond defense-focused federal agencies into civilian government sectors characterized by longer procurement cycles but potential volume growth as well as cautiously entering commercial markets with higher demand variability but larger addressable opportunities [N2][N3][S6][S18].

This growth depends heavily on enhancing indirect sales channels including system integrators who bundle INTRUSION Shield with complementary cybersecurity offerings—a strategy complicated by reseller non-exclusivity that may dilute partner incentives toward larger incumbents [S4][S13][N2].

Government budget unpredictability remains the chief constraint with contract cancellations or delays posing downside risks given limited backlog visibility; thus diversification efforts are critical for sustainable mid-term growth [S6][N3]. Technological enhancements targeting endpoint protection for cloud-native workloads and remote users launched recently show promise but require time for broader market penetration typical of enterprise cybersecurity adoption cycles spanning multiple quarters or years [N2][S26].

Key Metrics and Milestones to Monitor

Investors should track quarterly revenue trends excluding one-time spikes to assess underlying business momentum following recent Q4 revenue declines that triggered share price weakness (-8% post-earnings release March '26) reflecting sensitivity toward maintaining growth amid macroeconomic uncertainties ([N1],[N3]). Renewals among top government clients (>10% revenue each) warrant close observation due to inherent cancellation flexibility affecting near-term visibility ([S6]).

Liquidity milestones including successful equity raises or debt facility access are vital given regulatory restrictions tied to sub-$75 million public float valuations impacting capital raising capacity ([S22],[S16]). Progress expanding civilian agency pipelines via channel partners measured through backlog changes can indicate diversification success ([N2]). Lastly, sustaining relevance of the large historical IP database amid evolving threats will be critical for long-term moat durability versus AI-driven behavioral analytics competitors ([S9],).

This analysis is based exclusively on publicly filed documents including Intrusion Inc.'s Annual Report on Form 10-K filed March 25, 2026 ([F1],[S1]) supplemented with earnings call transcripts ([N2]) and market news ([N1],[N3]) without extrapolation beyond verified numeric data or stated management commentary. Readers should weigh risks associated with concentrated government customer exposure alongside cyclical budgetary impacts when evaluating Intrusion’s operating performance trends presented herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments