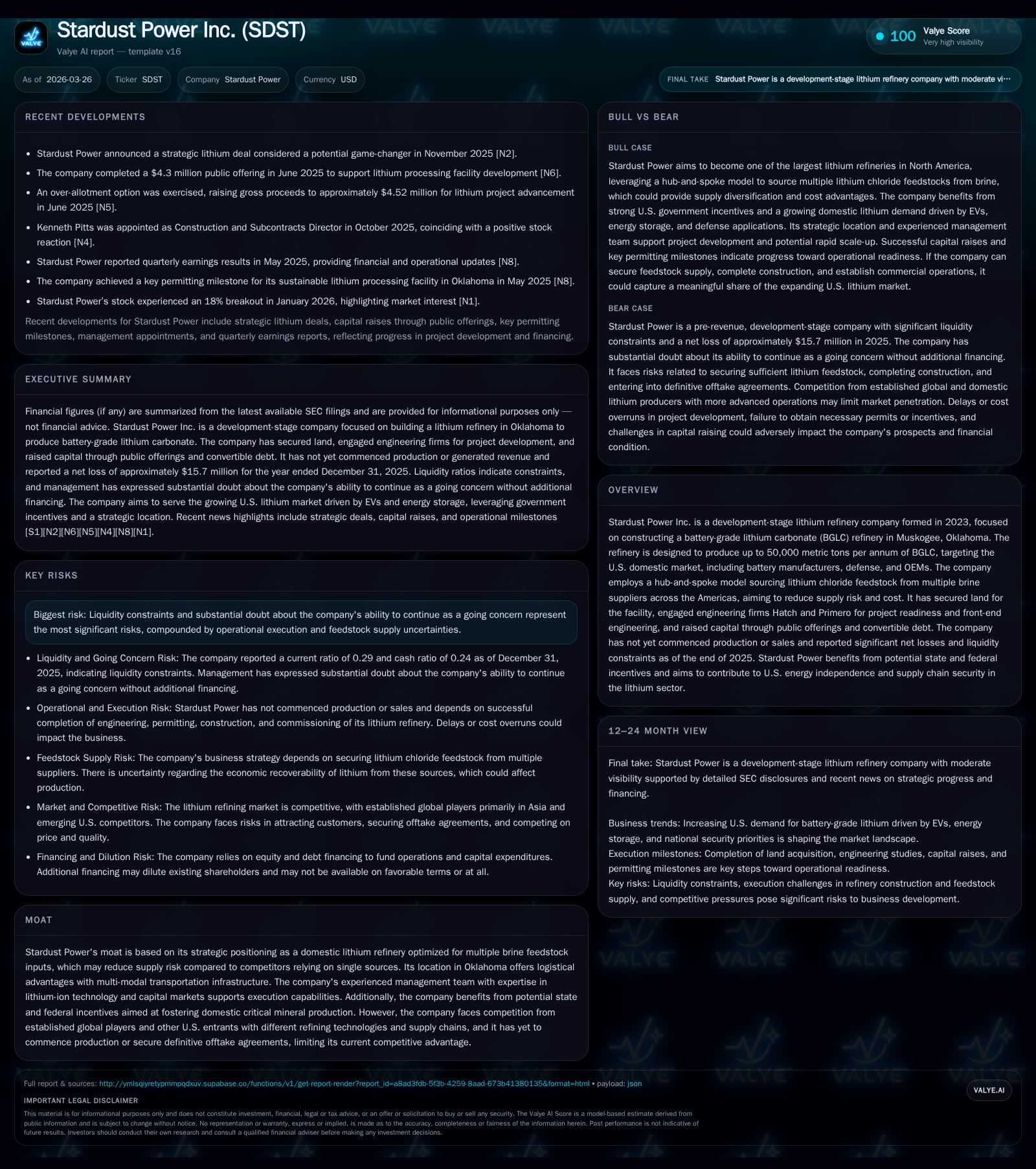

Stardust Power's Ambitious Lithium Refinery Project Faces Financial and Execution Hurdles

Development-stage lithium refinery firm targets U.S. battery supply but grapples with liquidity, operational risks, and unproven supply agreements.

Stardust Power Inc. is building a battery-grade lithium carbonate refinery in Oklahoma with an annual capacity of 50,000 metric tons, aiming to serve U.S. battery manufacturers and defense clients. Since its founding in 2023, the company has made progress in land acquisition and engineering partnerships but remains pre-production and non-revenue generating, reporting sharp net losses and negative cash flows through 2025. Significant liquidity constraints raise substantial doubt about continuation as a going concern. Growth depends heavily on securing reliable lithium feedstock supply via its hub-and-spoke model and closing binding offtake contracts, while competitive pressures and regulatory complexities add to execution risks.

Company Background and Development Stage

Stardust Power Inc., established in March 2023 through a series of corporate restructurings involving Stardust Power LLC and Legacy Stardust Power, is focused on constructing a battery-grade lithium carbonate (BGLC) refinery in Muskogee, Oklahoma. The Company's facility is designed for an annual capacity up to 50,000 metric tons targeting domestic U.S. demand from battery producers, defense contractors, and original equipment manufacturers (OEMs) [S1].

The company’s strategic approach centers on a hub-and-spoke model that sources lithium chloride feedstock from multiple brine suppliers across the Americas to reduce dependence on any single supplier or geographic region. This model aims to enhance supply chain stability against volatility common in lithium markets [S1]. The facility's location benefits from favorable multimodal transportation logistics.

As a development-stage enterprise, Stardust Power has not commenced commercial production or generated revenue to date. Its business plan encompasses advancing site acquisition, finalizing engineering feasibility via engagements with Hatch and Primero Engineering firms, securing feedstock supply agreements, obtaining binding off-take contracts for product sales, and raising capital through equity and debt financing [S1][S23].

Historical Financial Performance

Operating results since incorporation highlight the expected cash burn pattern typical for early-stage miners/refiners investing in inorganic growth through capital expenditures.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -16 | -8 | -16 | +33.8% |

| 2024 | -24 | -10 | -18 | -17189.1% |

| 2023 | 0 | -1 | -2 | -99.1% |

| 2022 | 15 | -2 | -2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 270.5 |

| 2024 | 122.5 |

| 2023 | -0.7 |

| 2022 | -102.3 |

Source: SEC companyfacts cache [F1].

Net income figures show significant negative swings in absolute terms as the company scales development activities with no corresponding revenues. [F1]

The cash flow from operations remains negative reflecting ongoing expenses tied to engineering studies and project preparation rather than operational cash inflows. Equity is deeply negative due to accumulated losses exceeding contributed capital [F1].

Growth Prospects and Catalysts

Stardust Power’s planned refinery could fulfill growing U.S. demand for domestically produced battery-grade lithium carbonate amid increasing geopolitical emphasis on securing critical minerals supply chains for energy storage technologies.

Key growth drivers include:

- Completion and commissioning of the Muskogee lithium refinery facility.

- Successful implementation of the multi-sourced lithium chloride feedstock strategy reducing risks inherent in relying on single-source supplies.

- Execution of definitive binding offtake agreements beyond existing non-binding letters like the one signed with Sumitomo for up to 20k metric tons/year over a decade [S23].

- Leveraging state incentives up to $257 million from Oklahoma conditioned on milestone achievement that substantially offset capital costs [S7][S26].

- Potential federal incentive programs under the Inflation Reduction Act or Defense Production Act enhancing financial viability though subject to political uncertainty [S18][S27].

- Partnership with seasoned engineering firms Hatch and Primero mitigating technical execution risk by employing proven refining technology.

However, stagnation or failure modes stem from several sources:

- Liquidity constraints raise substantial doubt about continued operations without successful future fundraising efforts [F1][S16].

- Uncertainty over the economic viability and availability of upstream brine feedstock which requires exploration and extraction success by third-party suppliers underpins raw material risk.

- Competitive pressure from entrenched multinational refiners primarily based in China possessing scale advantages and long-standing customer relationships may limit market penetration.

- Regulatory complexity around environmental permitting due to potential impacts related to water usage and hazardous materials handling introduces potential delays or cost overruns [S4][S6].

- Absence of definitive binding off-take agreements means that even if production commences there is no guaranteed immediate market for output.

- Possible technological shifts such as evolving battery chemistries reducing future lithium demand may also impair market growth.

Forecasts and Expectations

Explicit forward guidance is not provided due to developmental status. However future indicators to monitor include:

- Progress towards construction milestones: site preparation completion dates,

- Feedstock contract signings converting existing LOIs/MOUs into binding volume commitments,

- Offtake agreement finalizations ensuring stable revenue streams,

- Government incentive approvals releasing incremental subsidization,

- Capital raises addressing current working capital shortfall,

- Environmental permitting achievements enabling construction advances,

- Unexpected litigation outcomes such as the ongoing breach of engagement claim filed by H.C. Wainwright impacting operational focus or cash resources.

These markers will crucially influence Stardust’s ability to proceed toward first production and commercialization in line with stated objectives [S23][S8].

Capital Structure and Returns Analysis

As of December 31st 2025: • Cash & Equivalents: Approximately $3.5 million • Current Liabilities: Approximately $14.3 million • Current Ratio: Approximately 0.29 indicating severe short-term liquidity pressure [F1] • Accumulated Deficit leads to Negative Equity at about -$5.8 million figure reflecting sustained losses since inception [F1] • Operating Cash Flow remains deeply negative (-$8.3 million) consistent with ongoing project development costs that outpace cash inflows given zero revenues so far [F1] • No dividends or share repurchase activity reported given capital preservation focus at this stage; all funding directed towards project advancement [S15].

Funding has been sourced primarily through:

- Public offerings completed in early-mid 2025 raising upwards of $10 million gross before fees,

- Convertible senior secured note issuance raising approximately $4 million December 2025,

- Private placements totaling several million dollars during late 2024,

- Agreements such as B.Riley Purchase Agreements providing potential additional capital access albeit with dilution risks [S7][S15][S21].

Management warns of substantial doubt about ability to continue as going concern absent additional equity or debt funding beyond current resources [F1][S16][S17]. This stresses the importance of upcoming capital market access measures being timely executed.

Return metrics such as Return on Equity are distorted by large historic losses leading to negative equity base; approximate ROE calculated is algebraically high (~270%) but reflects accounting loss relative to negative denominator rather than positive profitability [F1].

Industry Positioning and Competitive Environment

Stardust Power positions itself in a niche focused on domestic U.S.-based lithium refining optimized for battery-grade quality outputs sourced from multi-origin brines rather than conventional spodumene concentrates predominantly processed overseas or controlled by China-based companies like Tianqi Lithium.

Although the U.S. government has amplified support for domestic critical mineral processing under recent infrastructure laws aimed at reducing dependence on foreign suppliers (especially China), competition is intensifying as other entrants establish refineries using different technological approaches or prioritize integrated mine-to-refine operations.

The company’s moat relies partly on its sourcing model hedging feedstock procurement risk across various brine producers; however both upstream supply reliability and scalability remain largely unproven.

Barriers include:

- Significant capital intensity associated with refinery construction,

- Regulatory hurdles relating to environmental compliance,

- Establishing customer trust through quality certifications necessary for battery manufacturers and OEM acceptance,

- Responding swiftly to market price dynamics influenced by regional geopolitical factors impacting lithium demand/supply balance,

- Legal risks associated with intellectual property protection still mostly undeveloped at this early stage [S9][S13].

Risks Summary

The company highlights key risks including: • Limited operating history complicates forecasting business prospects reliably; • Substantial doubt about going concern due primarily to liquidity gaps that threaten operational continuity absent financing success; • Dependence on successful exploration/extraction efforts by upstream partners supplying brine-derived lithium chloride feedstock; • Execution risks related to timely construction completion amidst possible delays; • Potential inability to secure binding customer contracts may result in costly inventory buildup or underutilization; • Intense competition from better-funded international players could compress margins; • Regulatory environment increasingly complex especially regarding environmental permits and safety standards — noncompliance could result in sanctions; • Legal exposure exemplified by pending lawsuit alleging breach of contract potentially causing diversion of resources and reputation impact; • Market price volatility arising from general macroeconomic conditions affecting sustaining customer demand. [S1], [S4], [S6], [S7], [S8], [S9], [S13], [F1]

Conclusion/Outlook Analysis

Stardust Power’s vision aligns closely with U.S. strategic policy priorities emphasizing domestic control over critical minerals vital for electric vehicle batteries and grid storage solutions; however execution challenges inherent in development-stage projects weigh heavily against near-term commercial viability.

Stakeholders will be observing whether management can successfully unlock additional financing amid tight liquidity pressures while advancing construction without regulatory setbacks. Securing definitive off-take contracts beyond currently non-binding arrangements will be critical validating commercial demand assumptions underpinning projected revenues once operations commence.

Navigating growing competition within an evolving legal and environmental compliance landscape also constitutes an ongoing test of organizational capability beyond mere engineering prowess.

Ultimately Stardust Power exemplifies the high-risk/high-reward nature typical within nascent cleantech mining/refining ventures operating downstream where timing fundamentals intersect heavily with external macro-political developments impacting global critical minerals trade flows.

This analysis summarizes publicly available information about Stardust Power Inc.’s strategic direction, financial condition as at FYE 2025 per SEC filings and industry context without constituting investment advice or endorsement.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments