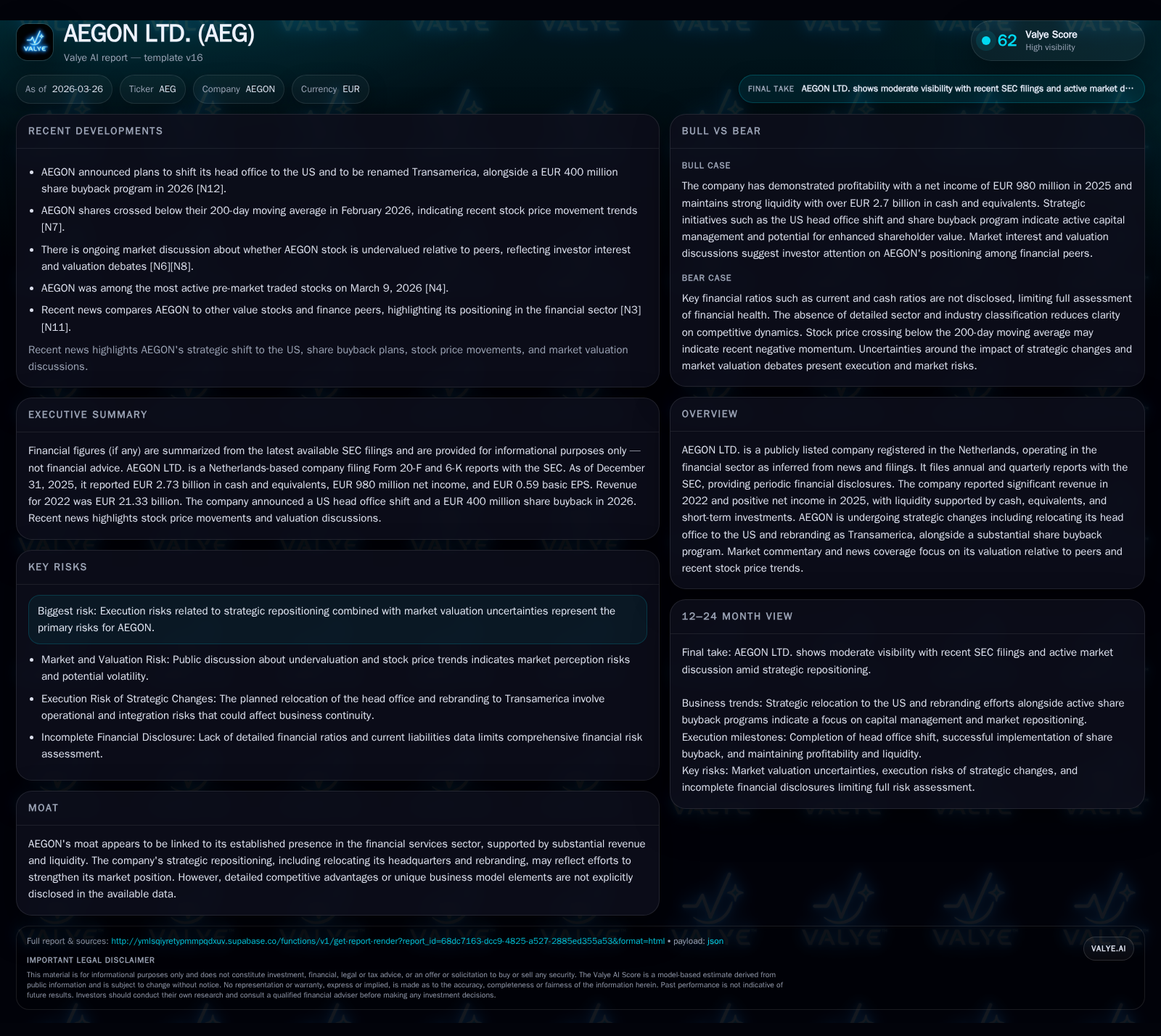

AEGON’s Turnaround: From Revenue Declines to Strategic US Reorientation

AEGON transitions from significant revenue erosion to renewed profitability amid a strategic relocation and robust capital management.

After several years marked by revenue declines and net losses, AEGON Ltd. has returned to net income profitability in 2025 driven by operational improvements and strategic focus on the US market. The company is executing a landmark headquarters relocation to the United States, rebranding as Transamerica, alongside an aggressive share repurchase program that underscores disciplined capital allocation. While growth prospects center on expansion within the US life insurance and retirement segments, execution risks around redomiciliation, regulatory shifts, and competitive pressures remain notable. Investors should monitor progress on US GAAP adoption and buyback completion as key near-term milestones.

Historical Performance and Revenue Volatility Trends

AEGON experienced a pronounced reversal in its top-line trajectory across the four-year span ending in FY2022. Revenue diminished by nearly €6.9 billion or about -24% cumulatively from €28.2 billion in FY2019 to €21.3 billion in FY2022 ([F1]). This decline reflects a combination of structural challenges including divestitures and persistent market headwinds affecting investment returns and underwriting volumes.

Concomitant with revenue contraction were substantial net losses recorded for FY2022 (-€1.4 billion) and FY2023 (-€199 million), underscoring operational strains before returning to solid profitability in FY2024 (€676 million) and further expansion in FY2025 (€980 million), a striking YoY increase of approximately 45% ([F1]).

Dividend payouts exhibited gradual increases even during loss periods, rising from €347 million paid in FY2022 to €596 million in FY2025, evidencing management's commitment to shareholder remuneration despite earnings volatility ([F1]).

Historical performance (annual)

| FY | Net ($mm) | Net YoY |

|---|---|---|

| 2025 | 980 | +45.0% |

| 2024 | 676 | +439.7% |

| 2023 | -199 | +85.8% |

| 2022 | -1404 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 596 | 10.3 |

| 2024 | 521 | 7.3 |

| 2023 | 495 | -2.1 |

| 2022 | 347 | -9.9 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures available through FY2022; net income and dividends cover through FY2025 ([F1]).

Drivers Behind Recent Profit Recovery

The sharp rebound in net income through FY2025 emanates principally from stringent cost control measures alongside improved underwriting margins reflecting enhanced reserve adequacy assessments ([S1],[N6],[N8]). Aegon’s adaptation of its risk management framework — incorporating more conservative pricing models for guaranteed products — mitigated exposure to adverse claims fluctuations.

Investment returns contributed positively with beneficial market conditions boosting earnings on in-force policies particularly within variable annuities ([S20]). The reduction of new business strain via optimized product mix also played a role.

Operational efficiencies tied to streamlining global platforms increased margin potential as Aegon took strides toward consolidating portfolio management systems ([S16]). These factors combined have underpinned the restoration of sustainable profitability.

Strategic Shift: US Headquarters Relocation and Rebranding as Transamerica

A pivotal development is AEGON’s announced relocation of its corporate head office from Schiphol, Netherlands (legal domicile Bermuda), to the United States, targeted for completion by January 1, 2028 ([S6],[S11],[N3]). Concurrently, the holding company will be rebranded Transamerica Inc., cementing focus on the US life insurance marketplace where Transamerica already accounts for roughly 70% of operations.

This move aims to capitalize on the largest global life insurance market's growth opportunities—particularly among "Main Street" American middle market households underserved by existing players ([S6]). The transition also requires migration from IFRS accounting principles to US GAAP standards commencing fiscal year-end reporting for full-year 2027 ([S6]).

Execution risks are non-trivial: regulatory reporting adjustments impose near-term financial statement complexity; tax residency change may alter effective tax rates materially; talent retention amidst geographic shift poses continuity risks ([S11],[S19]). Additionally, brand equity must be carefully managed through customer communications during rebrand implementation phases.

Capital Allocation: Share Buybacks, Dividends, and Investment Priorities

Capital discipline stands out as a cornerstone of AEGON's recovery narrative. In July–December 2025, it successfully completed a EUR 400 million share buyback representing over sixty-one million shares canceled immediately thereafter ([S7]), followed by commencing an additional EUR 400 million buyback program split evenly across H1 & H2’26 ([S9]). This move reflects confidence in undervaluation relative to intrinsic business value as echoed in recent market commentary ([N6],[N3]).

Dividends increased consistently with payout climbing from €347 million in FY22 to €596 million in FY25 ([F1]), supported by steady free cash flow generation overlapping these years (approximately €0.8 billion per annum run-rate expected with incremental growth per [S16]). Capital returned is thus balanced against maintaining Cash Capital at Holding within targeted midpoints (€0.5–1.5 billion) ensuring strategic flexibility while preserving solvency ratios aligned with EU regulations ([S15],[S20]).

The approximate Return on Equity for FY25 was calculated at around 10.3%, illustrating effective deployment of equity capital towards earnings regeneration ([F1]).

Future Growth Prospects and Market Constraints

AEGON places primary growth bets on expanding its US footprint leveraging Transamerica’s distribution capabilities via World Financial Group’s agent network (approximately +14% life sales CAGR targeted). The Protection Solutions segment aims for a robust +15% annual life sales increase while bolstering retirement plan assets under administration toward roughly USD $275 billion by end-2027 with improvement in return-on-assets metrics ([S18],[N3]).

Internationally, AEGON intends measured investment into partnerships across emerging markets including China and Brazil complemented by asset management integrations driving operating result growth above EUR 200 million by FY27 ([S16],[S18]). Meanwhile, Aegon UK faces strategic review considering divestment options given shifting company focus toward US operations ([S16],[S18]).

Constraints include intensified competition within mature markets especially US life insurance; evolving regulatory capital requirements potentially elevating technical provisions; liquidity availability fluctuations; plus macroeconomic interest rate unpredictability impacting demand elasticity ([S19],[S21]). Notably absent is explicit forward-looking EBIT or net income guidance which places emphasis on monitoring quarterly updates for validation of growth momentum.

Risk Factors Surrounding Redomiciliation and Execution Challenges

AEGON’s filings provide exhaustive detail delineating risks specific to the ongoing redomiciliation project alongside broader operational hazards ([S11],[S19],[S21],[N3]). Execution risk looms large given multi-year scope requiring complex coordination across legal compliance, tax planning, IT systems conversion (including US GAAP adoption), and employee retention strategies.

Potential cost overruns could strain earnings; timing uncertainties might delay anticipated benefits; elevated operating costs post-move present profit margin pressure points; while customer disruption risks necessitate proactive communication efforts ([S11],[S19]). Regulatory uncertainty involves both European Commission stances on Bermuda equivalence status changes along with evolving US state-level insurance mandates requiring vigilant navigation ([S21],[S23]).

Operational risks also extend into cyber security vulnerabilities amplified during organizational upheaval as well as limitations on data privacy compliance impacting reputational capital. Furthermore, AEGON cautions that its actuarial models underpinning longevity/mortality assumptions could misrepresent future claims resulting from unpredictable shocks or model error propagation ([S22],[S25]).

What Investors Should Watch Next: Milestones and Valuation Metrics

With explicit financial forecasts limited beyond mid-2027 horizons, investors should prioritize tracking execution progress on relocating headquarters including cessation of IFRS reporting post-December-2027 fiscal year-end milestone ([S6],[N3]). Completion trends of ongoing EUR400 million share buyback scheduled through June-30-2026 will serve as tangible barometers of management confidence and capital return discipline ([S9]).

Equally important will be quarterly earnings stability reflecting sustained underwriting improvements offsetting macro uncertainties as well as management commentary regarding ongoing market share gains within protection products and retirement business lines ([N6],[N3]). Market commentary highlights AEGON trading at valuation multiples below some peers potentially warranting reassessment upon demonstrated delivery of strategic objectives ([N3],[N6]).

Close watch on effective tax rate movements post redomiciliation announcement will also provide early signals about operating leverage under expanded US regulation frameworks.

Disclaimer: This analysis is based solely on publicly available data extracted from Aegon Ltd.'s SEC filings and recent news coverage dated up to March 26, 2026. It does not constitute investment advice or recommendations but aims to provide an informed evaluation grounded strictly on disclosed information without speculative extrapolation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments