Southland Holdings Faces Liquidity Strains Amid Revenue Decline and Legal Setbacks

The specialty infrastructure constructor wrestles with contract disputes and elevated debt service while repositioning its business.

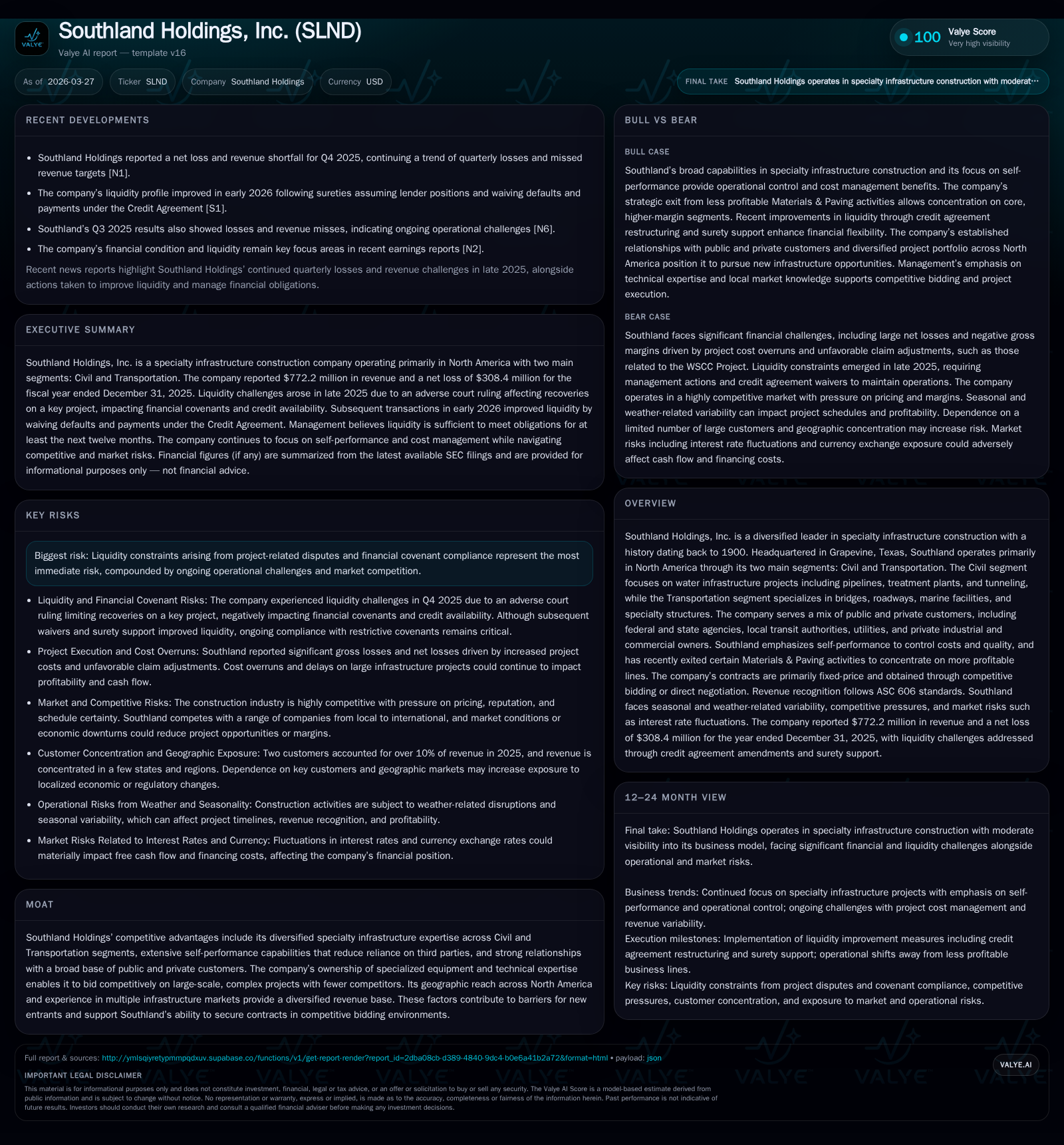

Southland Holdings, Inc. reported a sharp revenue decline of over 21% in 2025 following an adverse legal judgment related to a major WSCC project that impacted liquidity and compliance with financial covenants. Despite a diversified specialty infrastructure portfolio across Civil and Transportation segments, profitability eroded significantly with operating losses doubling year-over-year. Capital structure remains leveraged with ongoing principal and interest payment waivers negotiated with lenders, though the company maintains sufficient near-term liquidity through surety advances and asset sales. Near-term growth hinges on contract backlog conversion, prudent bidding, and resolution of ongoing disputes.

Company Background and Historical Performance

Founded in 1900, Southland Holdings, Inc. has evolved into a diversified leader in specialty infrastructure construction targeting primarily North American markets. The firm is structured around two main operating segments: Civil — focusing on water infrastructure including pipelines and treatment plants — and Transportation, which specializes in bridges, roadways, marine facilities, and specialty structures [S1]. Its subsidiaries include Johnson Bros. Corporation, American Bridge Company, Oscar Renda Contracting among others, which collectively enable Southland to bid on large-scale complex projects leveraging self-performance capabilities and ownership of specialized equipment [S1][S16].

From a financial perspective, Southland experienced a steep revenue contraction from $1.16 billion in 2023 to $980 million in 2024 (a 15.6% decrease), followed by a further decline to $772 million in 2025 (down 21.2% YoY) [F1]. This falloff reflects pressure from project execution hurdles, including an adverse legal ruling related to the WSCC Project during Q4 2025 which adversely affected expected claim recoveries and retention sums [S1][S7][S18].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 772 | -307 | 17 | -217 | -21.2% | -190.9% |

| 2024 | 980 | -105 | 2 | -126 | -15.5% | -447.3% |

| 2023 | 1160 | -19 | -10 | -31 | -1096.9% | |

| 2022 | 2 | -2 | -1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 75 | 13 | 217.5 |

| 2024 | 75 | -5 | -64.4 |

| 2023 | 75 | -21 | -7.7 |

| 2022 | -20.7 |

Source: SEC companyfacts cache [F1].

Revenue YoY calculated between each fiscal year; Operating losses expanded materially despite attempts at cost control.

Operational Challenges and Segment Focus

Southland’s strategic decision in mid-2023 to divest certain Materials & Paving assets within the Transportation segment illustrates an effort to sharpen focus on more profitable specialties [S1]. This pruning should theoretically enhance margin profiles through concentration on core capabilities such as water infrastructure design/construction and complex bridge or marine facility builds where fewer competitors have the required expertise and equipment [S1][S16].

However, the impact of contract disputes like the WSCC litigation has injected volatility into earnings and cash flow projections [S7][N1]. Fixed-price contracts prevalent in Southland’s portfolio limit pricing flexibility when faced with cost overruns or delays, common pitfalls exacerbated by supply chain disruptions or labor market tightness endemic across North America’s construction ecosystem.

Financial Discipline Amid Liquidity Pressures

Despite generating negative operating income for three consecutive years stretching back to at least 2023 (-216M USD in FY25 per [F1]), Southland produced positive operating cash flow of $16.6 million in FY25 versus only $1.9 million the prior year owing largely to working capital adjustments including reductions in contract assets and increases in payables and deferred taxes [S1][S13].

Capex expenditure decreased almost by half from $7.4 million to $3.8 million reflecting curtailed investment during operational retrenchment [F1]. Nonetheless, substantial leverage persists with total debt net of deferred financing costs measured at approximately $258 million at December 31, 2025 [F1][S14][S25]. The company's equity position turned negative at $(141) million after significant net losses despite some equity infusions or revaluations previously recorded [F1], signaling distress conditions.

Southland’s Credit Agreement executed September 30, 2024 provides for a secured term loan facility totaling $140 million with quarterly amortization requirements increasing from an initial principal payment rate of about 5% annually up to larger amortization steps later years [S4][S9]. Following the liquidity strains linked to WSCC project outcomes reported late last year, sureties assumed lender positions on March 17, 2026; they waived potential defaults and all scheduled principal/interest payments until maturity resulting in estimated cash savings exceeding $30 million through the next twelve months [S6][S18]. Additionally, these sureties advanced over $100 million post-year-end under bond support agreements critical for maintaining project execution continuity [S18].

This arrangement greatly alleviates imminent debt service obligations but requires collateral liquidation through disposal of idle equipment/assets alongside robust claim collection efforts directed towards principal repayments ahead of maturity [S12][S15]. The company also terminated its revolving credit facility upon final drawdown of term loan proceeds indicating tightened financial flexibility compared to prior years when a revolving facility up to $100 million was available albeit gradually reduced before termination [S12][S14].

Backlog Outlook and Market Positioning

Even as Southland confronts current operational headwinds, backlog stood at approximately $2 billion at fiscal year-end representing committed unearned revenue plus awarded but not started contracts as recognized under their accounting policy [S26]. However, typical industry contract arrangements involving termination rights held by customers imply that backlog isn’t an absolute safeguard against future revenue erosion.

Competition remains intense but also fragmented geographically and across end-market niches with few peer firms capable across both Civil and Transportation specialties nationally—especially considering Southland’s significant owned equipment fleet reducing dependency on rental markets serving as a key entry barrier for smaller competitors [S24][S16]. Strategic bidding selective toward projects that meet profitability thresholds alongside building long-standing customer relationships underpin management’s growth philosophy [S10][S24].

Returns and Capital Allocation Activity

Southland does not currently generate returns commensurate with invested capital given steep recent losses; approximate trailing ROE based on last reported net income over equity figures is negative but numerically inflated due to negative equity ($-306M / -141M ~217%), underscoring how leverage skews traditional metrics under distress conditions [F1].

No dividends were declared or paid amidst the liquidity focus; however prior buyback activities (~$74.6M cumulative repurchases noted for multiple years prior) indicate past attempts at shareholder value initiatives likely curtailed as financial stresses mounted [F1].

Cash generation modestly positive but constrained with free cash flow approximating $12.7 million after subtracting capex from operating cash flow for FY25—still relatively thin given scale of operations plus debt servicing needs highlighting necessity of ongoing liquidity management efforts including asset optimization [F1].

Risks Summary

Principal risks stem from liquidity challenges originating from WSCC Project disputes impairing anticipated collections; potential covenant breaches; competitive pressures impacting bidding success; cyclicality inherent in public/private infrastructure spending; reliance on fixed-price contracting exposing margin vulnerability; concentrated equipment investments tying up tangible assets; macroeconomic interest rate environment lifting borrowing costs; labor availability constraints increasing labor price inflation risk; legal exposures related to claims adjudications; and customer payment delays or defaults under protracted contracts [S7][S18][S23].[N1]

What To Watch Forward (Analysis)

- Track quarterly earnings improvements or worsening operating margins particularly how effectively management contains additional project overruns.

- Monitor litigation or claims resolution progress tied primarily to WSCC Project outcomes impacting cash recovery.

- Observe any capital restructuring events or amendment milestones related to Credit Facility terms including covenant compliance metrics.

- Watch backlog awards issuance rates plus renewal patterns especially larger scale Civil water infrastructure deals or multi-million-dollar Transportation contracts.

- Review asset disposals timing/valuation tied to credit agreements obligations toward debt reduction.

- Gauge broader sector construction input cost trends (materials/labor/equipment availability) influencing future bids profitability.

- Monitor credit market developments affecting refinancing opportunities amidst rising interest rate environment.

Conclusion

Southland Holdings represents a specialist player navigating turbulent waters with legacy operational setbacks impacting financial results sharply deteriorating into heavy losses despite improved near-term cash flow metrics achieved through active working capital management combined with lender concession packages enhancing short-run liquidity runway. The company’s industrial positioning — anchored by self-performance capabilities across difficult-to-enter Civil water systems construction alongside high-profile bridge & marine projects — buttresses competitive advantages amid relentless pricing competition across fragmented regional markets. Nonetheless, repairing balance sheet integrity while sustaining profitable topline growth remains daunting given fixed-price risk profile exacerbated recently by costly legal outcomes constraining available financing plus continued dependence on surety funding mechanisms supporting bonded jobs. Investor focus must remain calibrated closely on lawsuit resolutions monetization efforts alongside management’s ability to selectively bid while maintaining technical excellence delivering cost discipline vital for future profitability restoration within an unpredictable construction climate.

This analysis is based solely on publicly available information including SEC filings dated March 26, 2026 ([F1],[S#]) and recent market news ([N#]). It does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments