How Launch Two Acquisition Corp. Aligns Experienced Management with Its Upcoming Merger Target

Launch Two Acquisition Corp. leverages seasoned leadership and $237 million IPO capital to pursue a technology-focused business combination before its October 2026 deadline.

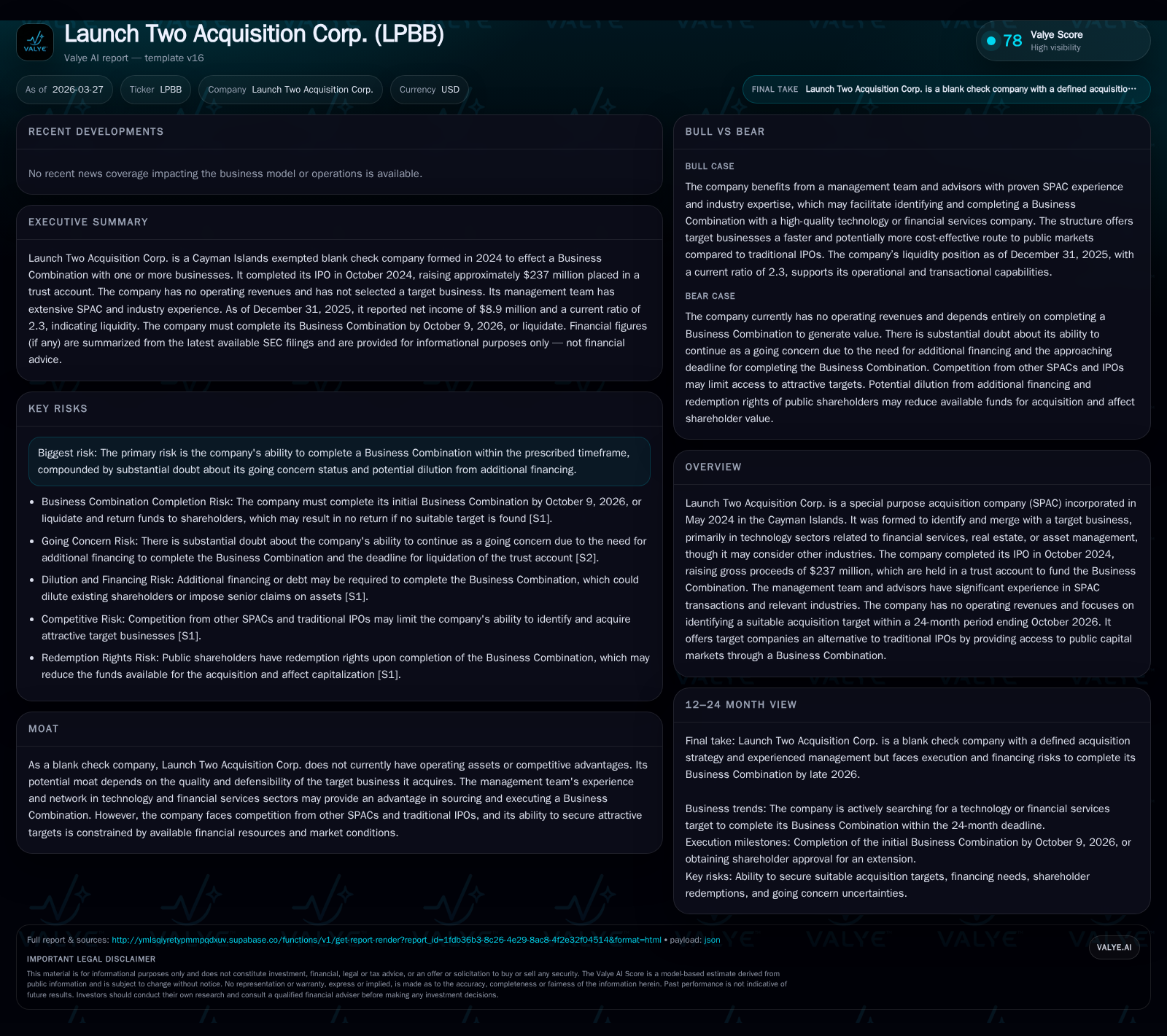

Launch Two Acquisition Corp. (LPBB) is a Cayman Islands-incorporated SPAC formed in May 2024, raising approximately $237 million in its October 2024 IPO to find a merger target primarily in the technology segments related to financial services, real estate, or asset management. With no operating revenues to date, LPBB must finalize a business combination within 24 months, creating pressure amid a competitive SPAC environment. The experienced management team emphasizes targets with scalable tech platforms and strong cash flow profiles. Investors should watch upcoming milestones including shareholder votes, redemption activity, and any additional financings as indicators of LPBB’s path forward.

Completion Window and SPAC Formation Background

Launch Two Acquisition Corp. (LPBB) was incorporated in the Cayman Islands on May 13, 2024, as a special purpose acquisition company formed to complete a business combination within a defined timeframe [S1]. The company conducted its initial public offering (IPO) in early October 2024, selling 23 million units at $10 each. This raised gross proceeds totaling approximately $230 million from the public offering plus an additional $7.1 million from private placement warrants issued to its Sponsor and underwriters—aggregating about $237 million [S1].

These proceeds are held in a trust account dedicated solely to funding the eventual merger or acquisition transaction (the "Business Combination") and related shareholder redemptions [S7]. LPBB's Amended Articles require completion of this Business Combination by October 9, 2026 (24 months post-IPO), or else be forced to liquidate and return funds held in trust back to shareholders [S1]. This deadline creates significant pressure on management to identify an attractive target without compromising deal quality.

As typical for blank check companies like LPBB, the entity does not generate operating revenues nor hold significant operating assets prior to consummation of the Business Combination. Its success depends largely on execution related activities rather than operational performance at this stage [S1].

Historical Financial Performance and IPO Capitalization

Though non-operational pre-combination, LPBB's financial statements reveal key metrics reflecting capital structure effects and administrative costs through FY2025 [F1]. Operating income declined sharply year-over-year from a loss of about -$173K in FY2024 to -$909K in FY2025—a drop of nearly -425%—reflecting increasing administrative expenses tied to search efforts and regulatory compliance [F1].

Conversely, net income rose materially by over 300% from roughly $2.2 million in FY2024 to about $8.9 million in FY2025 [F1]. This gain primarily arises from non-operating factors such as changes in fair value of warrant liabilities or unrealized gains on trust account investments common in SPAC accounting presentations—not cash-generated profitability [F1].

Operating cash flow worsened (negative $611K vs. negative $334K prior year), underscoring ongoing spend ahead of revenue generation [F1].

Balance sheet data shows current assets of approximately $360K against current liabilities near $156K at year-end 2025 yielding a current ratio above 2.3x—a positive near-term liquidity indicator—while equity remains significantly negative near -$10.7 million reflecting founder share accounting conventions under ASC guidance [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 9 | -610622 | -909063 | +302.2% |

| 2024 | 2 | -334067 | -173185 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -82.9 |

| 2024 | -22.5 |

Source: SEC companyfacts cache [F1].

Note: Negative ROE reflects distorted measure due to unique SPAC equity treatment.

Target Industry Focus and Acquisition Criteria

LPBB’s management expresses preference for technology-oriented firms intersecting financial services domains such as fintech infrastructure focused on digital asset enablement via blockchain integration with traditional finance systems [S5]. Within these verticals—financial services technology platforms including real estate tech and asset management solutions—LPBB seeks companies demonstrating predictable free cash flow alongside recurring revenue models typical of SaaS or platform-based businesses [S10].

Additional priorities include defensible competitive advantages derived through proprietary technology offering pricing or solution benefits that differentiate them meaningfully within competitive landscapes [S4][S10]. LPBB emphasizes scalable growth potential facilitated by efficient customer acquisition and cross-selling capabilities supported by established management teams experienced with public markets post-combination [S10].

Management retains flexibility to consider opportunities outside preferred sectors if strategic imperatives are met but commits to transparent disclosures should deviations occur [S4].

Competitive Environment for SPAC Mergers

LPBB operates within a crowded market where many contemporary blank check companies compete for high-quality targets fitting similar fintech-adjacent themes [S4]. Numerous peers are pursuing companies leveraging blockchain enhancements within traditional finance.

LPBB highlights differentiation through its experienced management team's sector expertise and transactional networks developed over years across relevant industries [S1][S4]. This "pricing, solution or timing advantage" framework reflects seeking not only fundamental target strength but also adeptness navigating complex deal processes amid valuation pressures [S4].

Nonetheless, elevated competition increases bidding intensity potentially inflating acquisition prices while diligence timelines compress calendar room before LPBB’s mandatory deadline . Regulatory scrutiny around SPAC structures adds another layer complicating swift execution.

Liquidity, Capital Structure, and Funding Options

As of December 31, 2025, funds available from IPO proceeds held within the trust account totaled approximately $243.4 million prior to deferred fees payable per underwriting agreements [S7][F1]. This forms the primary capital pool for deploying during the Business Combination.

LPBB holds no committed external debt facilities but maintains flexibility to raise debt or equity capital if needed either pre- or post-announcement should cash demands exceed trust funds—for example due to substantial Public Shareholder redemptions or larger target valuations requiring more consideration [S20][S25].

Additional financings could lead to dilution impacting existing Public Shareholders both through share volume increases and potential seniority rights embedded in convertible securities issued [S20]. Debt issuance may introduce covenants restricting operations post-combination.

This hybrid approach combining trust-held cash with opportunistic financing aligns with standard mid-sized SPAC practices targeting higher-value deals beyond cash-only transactions , though absence of firm third-party financing commitments introduces uncertainty if redemption levels are material or target enterprise values exceed initial capitalization.

Investor Returns, Dividends, and Shareholder Redemption Mechanics

Public Shareholders retain redemption rights enabling cash exit upon completion of the Business Combination at prices reflecting Trust Account valuations net of tax and fees—approximately $10.58 per share as of December 31, 2025—with payments made accordingly reflecting final adjustments [S3][S6][S14][S23].

This mechanism protects investors against failure or adverse deal terms by enabling orderly capital return near original IPO pricing plus accrued interest conservatively earned within Trust accounts following liquidation of original investments under regulatory constraints limiting risk exposure [S9].

Sponsor founders have contractually waived redemption rights on Founder Shares reducing dilution risk somewhat though insider purchases post-IPO could reinstate participation rights creating nuances on capital return prioritization upon wind-up scenarios [S3][S8]. Warrants issued as part of units expire worthless if no Business Combination occurs meaning warrant holders bear downside risk separately.

Shareholder vote structures via proxy or tender offers allow sponsor discretion regarding capital raises or timing maneuvers balancing shareholder approvals versus expedited closure objectives aligned with governance charters prior to IPO listing requirements enforcement [S14].

Operational Risks and Regulatory Landscape

LPBB’s primary operational risk is failing to consummate an initial Business Combination before October 9, 2026 triggering automatic dissolution where all liquid assets held in trust are returned less costs incurred during wind-down—a material binary existential risk unlikely mitigated barring rare SEC-approved extensions requiring special resolutions [S1][S14].

Further risks include dilution pressures corresponding with ancillary financings eroding shareholder stakes depending on seniority clauses linked with convertible instruments common within SPAC deals today [S20], evolving regulatory definitions affecting permissible Trust Account investments constraining yield strategies relative to earlier cohorts [S9], and contingent creditor claims against Trust Account monies arising from vendor disputes or fiduciary duty allegations potentially diminishing distributable balances despite internal controls—a recognized litigation risk heightened during wind-down phases absent waivers secured contractually from third parties engaged pre-merger agreements [S19].

No material litigation is currently pending involving LPBB’s officers or directors per disclosures [S13], limiting immediate reputational risks.

Key Milestones Ahead and What Analysts Should Track

Critical events shaping LPBB’s path forward over the next year until its combination deadline include:

- Timing and specifics of any merger announcement revealing target identity.

- Outcomes of shareholder votes required for approval involving sponsor-aligned founder shares alongside institutional investors.

- Redemption volumes impacting liquidity positioning ahead of closing.

- Announcements regarding incremental debt or equity fundraising signaling deal sizing expansions or recapitalization needs.

- Potential amendments relating to extension requests that could alter timing pressures.

- Market reception gauging investor appetite supporting deal valuations consistent with stated acquisition parameters.

- Ongoing regulatory developments affecting allowable structuring norms impacting reported financial disclosures.

For analysts monitoring LPBB amidst competitive fintech-focused SPAC mandates these indicators serve as essential barometers assessing strategic execution speed combined with governance discipline and adaptive financing prudence given elevated competition for scarce quality acquisition opportunities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments