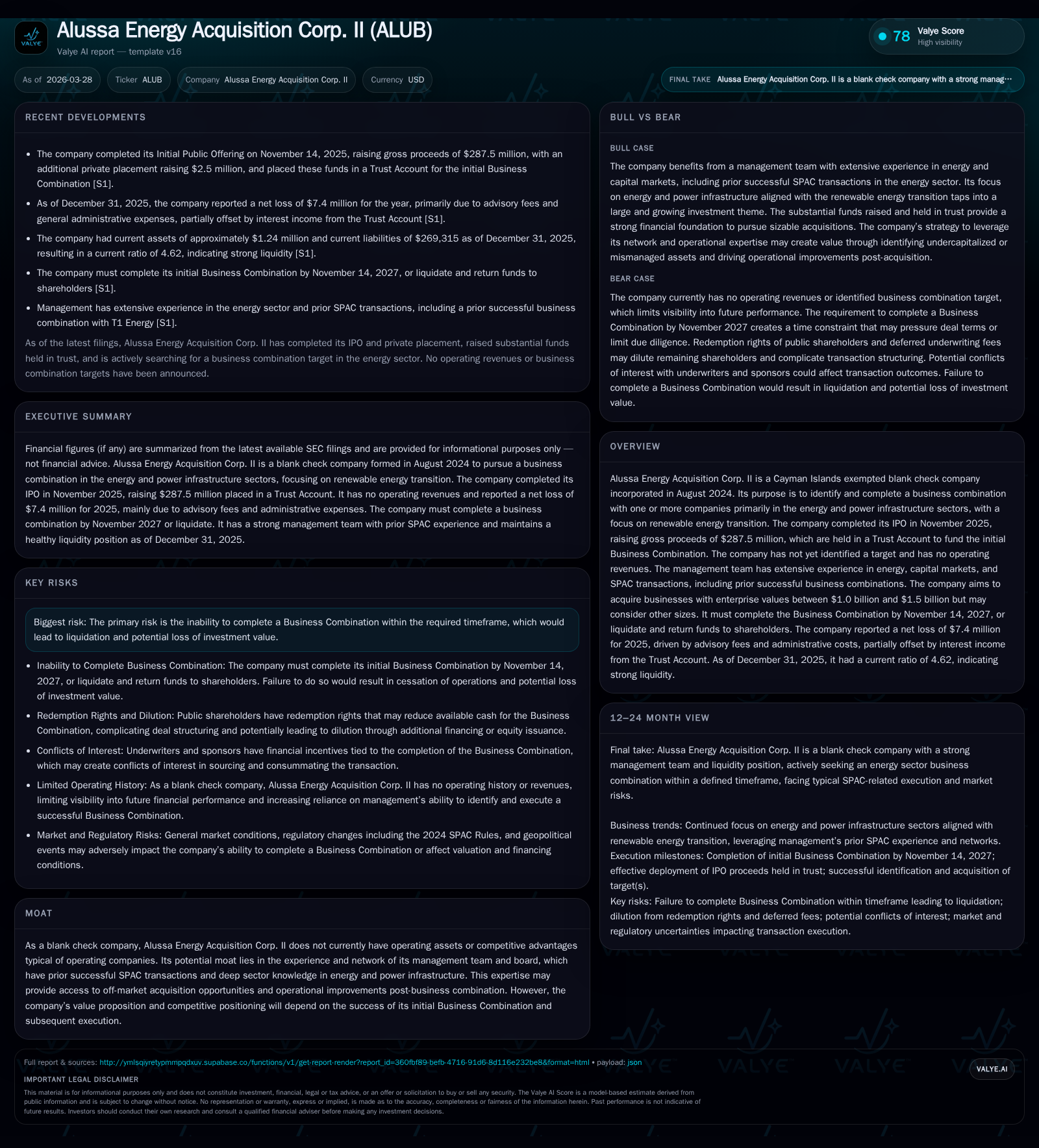

Alussa Energy Acquisition Corp. II Faces SPAC Deadline with $288M Trust Amid Renewable Energy Search

Examining Alussa Energy Acquisition Corp. II’s financial footing and strategic approach as it races toward its November 2027 business combination deadline focused on renewable energy.

Alussa Energy Acquisition Corp. II, a Cayman Islands exempted blank check company formed in August 2024, raised $287.5 million in its November 2025 IPO to pursue acquisitions in the energy and power infrastructure sectors targeting renewable energy transitions. With no operating revenues yet, the company has incurred net losses driven mainly by advisory fees and administrative expenses, offset partially by interest income on trust assets. Governance features tied to its Cayman jurisdiction grant founders significant voting control over the business combination approval process, potentially limiting public shareholder influence. The company faces heightened regulatory scrutiny from new SEC SPAC rules, which may increase transaction complexity and costs. The critical near-term milestone is locating and closing a qualifying business combination by November 14, 2027 to avoid liquidation and protect trust account capital.

From Inception to IPO: Capital Raising and Early Financial Outcomes

Alussa Energy Acquisition Corp. II was incorporated as a Cayman Islands exempted blank check company on August 16, 2024, with the purpose of effecting one or more business combinations primarily within the energy and power infrastructure sectors emphasizing renewable energy transition opportunities [S1]. Since inception through December 31, 2025, the Company has generated no operating revenues due to its pre-combination status but engaged in organizational efforts and preparing for acquisition activities.

The Company completed its IPO on November 14, 2025, issuing 28,750,000 units at $10 per unit including full exercise of the underwriter's over-allotment option [S1]. This raised gross proceeds of $287.5 million deposited into a Trust Account invested mainly in cash equivalents and short-term U.S. government securities designed to preserve capital while earning modest interest income [S6], [S27].

Operating expenses have been meaningful relative to scale given startup overhead and advisory costs: net losses reached approximately $7.4 million for the year ended December 31, 2025 [F1]. This loss primarily reflects an advisory fee of $8.625 million paid upon IPO consummation plus general administrative expenses of about $219 thousand [S1]. These costs were partly offset by interest income from investments held in the Trust Account totaling roughly $1.44 million during the same period [F1]. No revenue generation is expected until after completing a Business Combination.

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Note: The current ratio stood at approximately 4.62x as of December 31, 2025 reflecting strong liquidity [F1]. Operating cash outflows remain limited consistent with the SPAC's early stage.

Structural Features of a Cayman Islands SPAC

Incorporation in the Cayman Islands results in governance features differing from typical U.S.-based SPACs [S12]. Founder shares represent approximately 20% ownership post-IPO with enhanced voting rights that can enable approval of a Business Combination even without majority public shareholder support [S2]. Management may elect not to hold a public shareholder vote unless legally required or mandated by exchange rules.

This structure concentrates decision-making power among initial shareholders (founders), who have contractually agreed to vote in favor of any proposed Business Combination [S2]. While this may streamline execution by mitigating shareholder dissent risks, it also reduces minority investor protections relative to other jurisdictions.

Exclusive jurisdiction provisions designate Cayman courts for disputes related to the company's memorandum and articles of association potentially complicating shareholder litigation [S12]. These structural elements underscore reliance on management's judgment.

Strategic Focus on Renewable Energy Transition Sectors

Although there are no recent news citations available ([N/A]), filings describe management as experienced professionals with backgrounds in energy sector transactions and capital markets activities [S21].

Their strategy targets businesses within energy and power infrastructure benefiting from or driving renewable energy transitions—an area gaining significant investor attention globally [S1]. Target enterprise values range roughly from $1 billion to $1.5 billion but remain flexible depending on quality.

Post-acquisition plans emphasize operational improvements and leveraging emerging industry trends aligned with decarbonization efforts [S22], reflecting an understanding that successful assets combine stable cash flows with growth linked to evolving policy environments.

Impact of New SEC SPAC Regulations Effective in 2024

The SEC's new rules impose increased disclosure requirements including sponsor-related party details, conflict-of-interest transparency, dilution analysis, co-registration obligations for SPACs and targets during de-SPAC registration statements, and heightened Investment Company Act scrutiny [S1].

These regulatory changes are expected to increase transaction complexity, legal costs, and timing uncertainties associated with completing Business Combinations [S1]. For Alussa II—already navigating cross-border governance—these rules heighten execution risks.

Market participants anticipate longer due diligence periods alongside more rigorous review of financial projections and sponsor incentives alignment post-merger necessitating careful navigation by management.

Financial Overview: Losses Offset by Strong Trust Account Assets

As detailed earlier ([F1], [S6], [S13]):

- The net loss for fiscal year ended December 31, 2025 was approximately $7.4 million driven mainly by advisory fees and operating expenses.

- Interest income earned on Trust Account investments amounted to about $1.44 million reflecting low-risk holdings.

- Assets held in Trust Account totaled nearly $289 million earmarked exclusively for funding the Business Combination.

- Current liabilities remained low at approximately $269 thousand comprising accrued professional expenses rather than debt-like obligations.

No long-term debt exists other than minor ongoing fees payable until completion of the Business Combination or liquidation [S5], maintaining balance sheet simplicity common among blank check companies.

Capital Allocation Priorities Including Deferred Fees

Capital raised via IPO Units plus private placement warrants purchased by Sponsor exceeded $290 million intended solely for Business Combination funding [S1], [S5], [S7].

Underwriting fees include a deferred amount of approximately $8.625 million payable only upon consummation of the Business Combination aligning incentives between stakeholders and underwriters while minimizing upfront costs pending value realization [S5], [S20].

No dividends or share buybacks occur given absence of operating earnings; capital allocation focuses entirely on preserving acquisition capital until closing or liquidation triggers otherwise [S7].

Approaching the Business Combination Deadline: Risks and Contingencies

The Company must complete an initial Business Combination by November 14, 2027 or initiate liquidation procedures returning Trust Account funds (less certain expenses) to public shareholders shortly thereafter [S1], [S2], [S21].

Failure risks include loss of upside potential beyond recouped trust funds diminished by transactional deductions common across SPACs worldwide.

Extension amendments are possible subject to public shareholder approval allowing redemption rights exercisable under extended terms but may dilute existing shareholders if new units are authorized granting additional negotiation runway [S21].

Success depends on identifying suitable targets meeting investment criteria focused on renewable energy infrastructure aligned with favorable market dynamics [S22].

Risks Affecting Completion Probability

Key risks derive from both macroeconomic conditions impacting M&A activity and intrinsic blank check company factors:

- Market volatility could affect target valuations amid inflationary pressures impacting energy supply chains;

- Geopolitical instability such as ongoing conflicts may disrupt international deal flows or regulatory approvals;

- Additional regulatory changes beyond current SEC reforms could emerge increasing compliance burdens;

- Lack of operating history limits ability to demonstrate operational execution reducing negotiating leverage versus established acquirers or private equity firms competing for similar assets [S1], [S4].

Investor exposure centers on risk of non-completion triggering liquidation thereby limiting return prospects prior to deal closure.

Monitoring Points for Investors Moving Forward

Stakeholders should watch for:

- Public disclosures identifying prospective targets within stated enterprise value ranges focused on renewables/energy infrastructure;

- Proxy statements detailing terms of proposed Business Combinations including valuation metrics;

- Notices scheduling shareholder meetings concerning transaction approvals or extension amendments;

- Updates regarding financing arrangements involving share issuances or debt affecting post-closing capital structure;

- Information on management retention post-business combination signaling integration plans.

The approaching contractual deadline emphasizes importance of timely progress updates throughout the remainder of the current phase.

This report is based solely on information disclosed in Alussa Energy Acquisition Corp. II's SEC filings through March 27, 2026 ([F1], [S#]) without extrapolation beyond referenced data sources. No investment recommendations are provided herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments