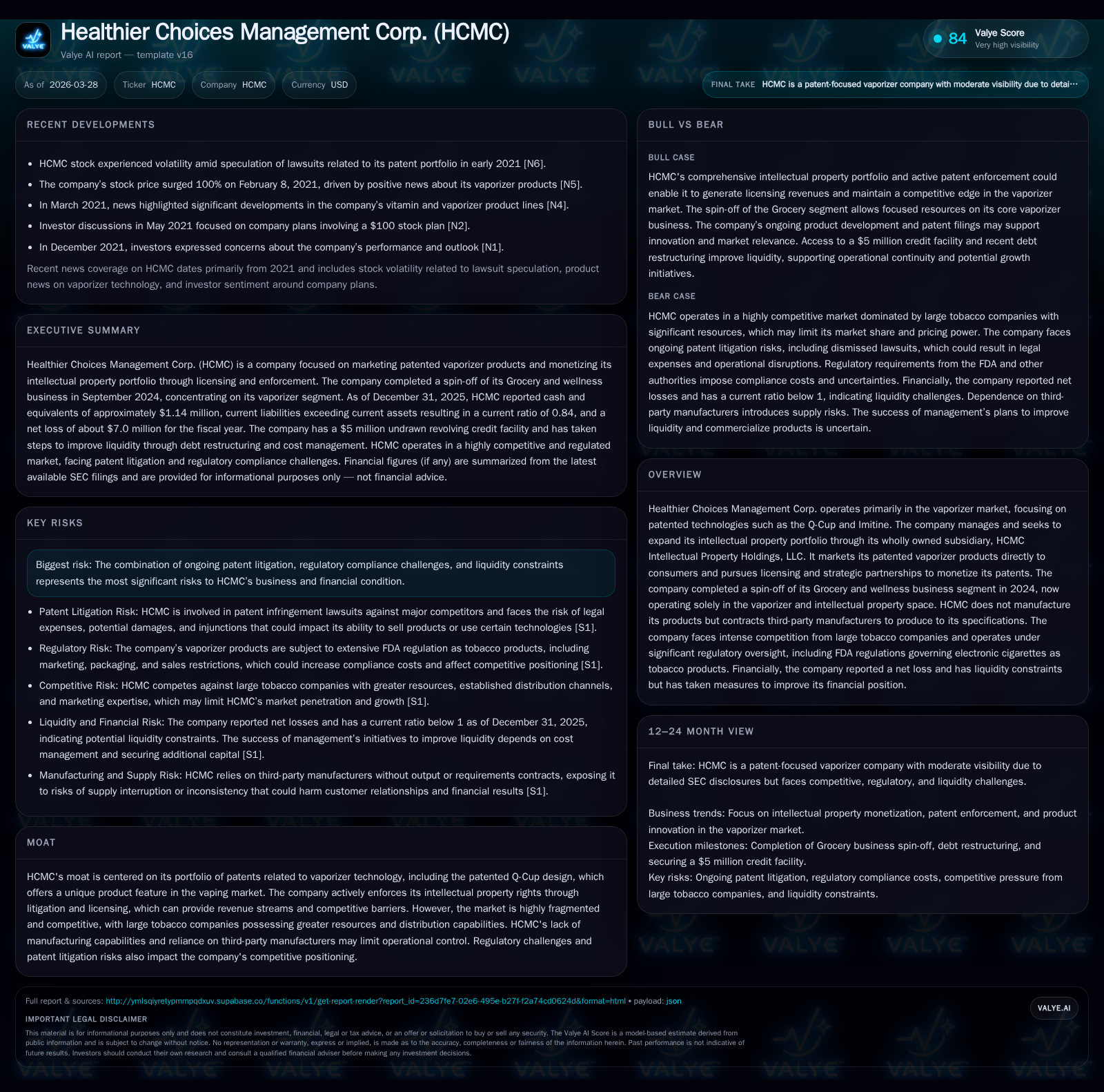

Healthier Choices Management Corp.: Patent Battles and Market Ambitions in the Vaporizer Sector

HCMC seeks to harness patented vaporizer technology revenues while navigating regulatory and litigation complexities post-Grocery spin-off.

Healthier Choices Management Corp. (HCMC) has transformed its corporate identity following the 2024 spin-off of its Grocery and wellness business, sharpening focus on vaporizer intellectual property commercialization. Despite persistent operating losses and negative cash flows since 2022, the company leverages its innovative Q-Cup™ technology as a distinctive moat amid a highly competitive market dominated by big tobacco. Ongoing patent litigations, notably with Philip Morris and R.J. Reynolds, along with FDA regulatory frameworks, represent significant operational headwinds. Key growth avenues lie in international patent expansion and expanding licensing streams, though liquidity remains constrained despite recent debt restructuring and an available credit facility.

From Spin-Off to Focus: Evolution of HCMC’s Business Model

In September 2024, Healthier Choices Management Corp. completed a strategic spin-off of its Grocery and wellness business segments—formerly operated under subsidiary Healthy Choice Wellness Corp.—to become an independent publicly traded company [S1][S8]. This marked a pivotal shift for HCMC from a diversified holding including retail grocery brands towards a pure-play vaporizer technology and intellectual property entity. The spin-off streamlined operations around patented vaporizer products such as the Q-Cup™ and Imitine technologies marketed directly to consumers via third-party manufacturing arrangements [S1][S8].

This separation entailed reporting discontinued operations for the Grocery segment for historical periods through the Spin-Off Date while consolidating financials post-spin-off solely within vaporizer-related activities [S1][S14]. The move intensified HCMC's exposure to sector-specific risks including intellectual property enforcement challenges, regulatory pressures from FDA oversight of electronic cigarettes as tobacco products, and competitive intensity within vaping hardware innovation [S5][S6][S10].

The narrow product focus allows targeted investment in expanding the IP portfolio managed by wholly owned subsidiary HCMC Intellectual Property Holdings LLC but concomitantly limits diversification which previously offered revenue buffers [S1]. Operationally, absence of manufacturing capability means HCMC relies entirely on contract manufacturers producing according to its specifications—a model common in vaping startups but exposing it to supply continuity risks [S7].

Historical Financial Performance: Trends, Operating Losses, and Revenue Analysis

Financially, HCMC’s continuing operations have yet to reach profitability since the spin-off consolidation period. Revenue figures are not disclosed separately post-2018 but pre-spin off top-line was approximately $14.6 million [F1]. Operating income was deeply negative from 2022 through 2025 though losses narrowed notably over this period (operating loss reduced by about 17% from $8.5M in 2024 to $7.0M in 2025). Net loss followed a similar trend improving from -$11.9M in 2024 to -$7.0M in 2025 indicating tighter cost controls or revenue growth support [F1].

Operating cash flow remains negative annually with a slight worsening rate (-6% YoY in 2025), primarily reflecting ongoing expenses exceeding earnings before capital investments. Capital expenditures have steeply declined (-75.5% YoY by 2025) consistent with reduced investment outlays post spin-off [F1]. Cash balances stood at approximately $1.1 million at year-end 2025 with current liabilities slightly exceeding current assets yielding a current ratio under unity at 0.84 [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -7 | -4 | -7 | 47185 | +41.0% |

| 2024 | -12 | -4 | -9 | 192865 | +35.7% |

| 2023 | -18 | -5 | -18 | 184349 | -156.1% |

| 2022 | -7 | -4 | -9 | 480925 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -4 | 568.9 |

| 2024 | -4 | 761.7 |

| 2023 | -5 | -273.5 |

| 2022 | -4 | -35.7 |

Source: SEC companyfacts cache [F1].

Though losses persist, improvement suggests either incremental revenue from licensing/royalty streams or cost optimization after shedding non-core assets [F1][S8][S3]. However, negative equity reported at approximately -$1.23 million at end-2025 signals accumulated deficits influencing balance sheet strength [F1].

Patented Innovation as a Competitive Moat: Q-Cup and Beyond

Central to HCMC’s competitive edge is its portfolio of patented vaporizer technologies managed under HCMC Intellectual Property Holdings LLC [S1][S14][S20]. The flagship is the Q-Cup™, featuring a small quartz microdosing cup designed for cannabis or CBD concentrates that is heated externally—enabling efficient vaporization without direct contact with the substance [S1][S14]. This design differentiates HCMC products by providing enhanced user convenience and dosing precision.

Since initial patents granted in October 2018 covering this technology, HCMC has steadily expanded its IP holdings with nine new patents awarded related to electronic vaporizers through the end of 2025 [S20]. The company actively pursues international patent filings in key global markets to strengthen cross-border protections and unlock monetization opportunities globally [S10]. This approach aligns with standard industry practice where robust patent portfolios underpin royalty streams and licensing negotiations.

Continuous research and development feed incremental enhancements to existing IP assets while new applications are pending approval — critical for maintaining technological relevance given rapid innovation cycles in vaping hardware markets dominated by larger competitors like Altria or R.J Reynolds who invest heavily into patent accumulation themselves [S10]. Such patents serve dual roles: erecting legal barriers amid intense market fragmentation thus providing potential licensing leverage; but also exposing HCMC to counter-litigation risk aimed at invalidating those patents or design-arounds by rivals [S6][S7].

Litigation Frontlines and Regulatory Landscape Impacting HCMC

HCMC’s patent enforcement trajectory has been marked by high-profile infringement disputes involving industry giants Philip Morris USA/Philip Morris Products S.A., targeting their IQOS™ heated tobacco device, and R.J Reynolds Vapor Company relating to Vuse e-cigarettes [S5][S6][S7]. In December 2024, a significant setback occurred when the Federal Circuit denied HCMC's appeal against USPTO Board decisions invalidating core patent claims underpinning the Philip Morris lawsuit, leading to dismissal of that case—delaying potential gains from royalties or settlements tied to that matter [S5].

Meanwhile, R.J Reynolds sought an inter partes review (IPR)—a specialized administrative challenge mechanism before the USPTO aimed at reevaluating patent validity—which could further impact claim enforcement efforts [S5]. Such IPR challenges are common tactical tools employed by larger competitors (") in this IP-heavy sector to limit smaller players’ leverage.

Overlaying these legal battles is a stringent regulatory environment governed primarily by FDA authority treating electronic cigarettes as "tobacco products" under the Family Smoking Prevention and Tobacco Control Act rather than drugs or medical devices because HCMC's vaporizers are not marketed for therapeutic claims [S13][S12][S9]. Consequently, compliance mandates such as product registration, ingredient disclosure, marketing restrictions including bans on free samples or vending machine sales except in youth-restricted venues impose both operational costs and marketplace constraints.

Additionally, evolving state/local regulations supplement federal rules with taxation changes, advertising limitations, packaging requirements including graphic health warnings—all elevating complexity for companies seeking broad consumer reach or flexible promotional strategies [S9][S12]. Failure to comply precisely exposes firms like HCMC to financial penalties potentially material enough to affect profitability trajectories given tight margins currently experienced.[S13]

Growth Prospects: Licensing, International Patent Expansion, and Product Development

Looking forward, HCMC emphasizes extracting commercial value from its IP portfolio mainly through expanded licensing arrangements including exclusive/non-exclusive deals facilitated via its dedicated IP subsidiary [S14][S10][S1]. These partnerships aim both at direct royalty revenue generation but also strategic co-development ventures that can accelerate product innovation leveraging shared know-how.

International patent filings form a critical component of this strategy providing defensive scope protection while opening untapped geographic markets—many with distinct regulatory frameworks presenting licensing opportunities differing from U.S.-centric plays [S10]. Innovation continues internally with new product lines incorporating proprietary designs such as refinements on Q-Cup® related hardware components intended for rollout pending patent award outcomes—signaling ongoing R&D commitment beyond legacy offerings [S14][S20].

Capitalizing on these prospects will depend on successful defense/winning outcomes in ongoing litigation plus adept navigation of regulation-driven barriers affecting market entry timelines or sales mechanisms.

Liquidity and Capital Allocation: Debt Settlement, Credit Facilities, and Cash Flow Dynamics

Despite ongoing operating losses that necessitate external funding support,[F1] management executed key liquidity bolstering maneuvers including settling $4 million of intercompany debt via issuing over 43 billion shares in late December 2025—substantially reducing liabilities without cash outflow impact while diluting equity structure significantly [S3][F1].

Further financial flexibility comes from an undrawn $5 million revolving credit facility secured November 7th, 2024 extended through end-December 2026 carrying a relatively high interest premium at 12% per annum—available exclusively for working capital purposes should cash needs arise imminently but unused through year-end fiscal 2025 reflecting prudent liquidity stewardship or cautious capital expenditure approach given prevailing uncertainty [S3][F1].

Capital allocation has thus far omitted dividends or share repurchase programs consistent with negative operating cash flow trends ([F1]), underscoring priority toward stabilizing balance sheet health while investing modestly in product development evidenced by subdued capex levels declining sharply (-75%) through year-end 2025 versus previous years [F1][S8].

Two aspects merit attention: (i) lingering negative equity position underscores cumulative losses impacting shareholder value; (ii) net operating cash flow remains consistently negative close to $3.9 million annually implying continued dependency on financing or licensing inflows beyond internal earnings alone until path toward sustained profitability solidifies.

What to Watch: Key Milestones and Potential Catalysts Ahead

With no explicit public guidance available,[N0] several determinants dominate near-term outlook for stakeholders tracking evolving dynamics:

- Legal verdicts in outstanding patent infringement matters particularly any rulings on R.J Reynolds Vuse IPR challenges which could reshape enforceability landscape;

- Progression toward additional licensing deals domestically and internationally generating recurring royalty streams critical for bridging cash flow gaps;

- FDA regulatory developments imposing novel requirements/clarifications potentially increasing compliance costs or restricting distribution channels;

- Patent grant notifications concerning pending applications which can unlock fresh product introductions enhancing competitive positioning;

- Management’s success refining operational cost structures further sustaining liquidity amidst evolving market conditions;

- Potential financing moves including equity raises or strategic investments required if organic cash generation stalls longer than anticipated.

Persistent monitoring of these vectors provides contextual understanding of opportunities balanced against intrinsic risks within this volatile sector shaped heavily by IP litigation outcomes combined with evolving public health regulatory regimes.

This analysis leverages public filings as of March 27th, 2026 inclusive of Healthier Choices Management Corp.’s fiscal twenty twenty-five results without projecting unconfirmed financial estimates or speculative forecasts beyond documented company disclosures ([F1],[S1]-[S20]). It aims solely to present an informed overview combining financial data interpretation with sector specific insight reflecting inherent challenges facing niche vaporizer IP holders competing against dominant tobacco conglomerates under shifting legislative frameworks. The content herein does not constitute investment advice nor endorsement regarding securities discussed.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments