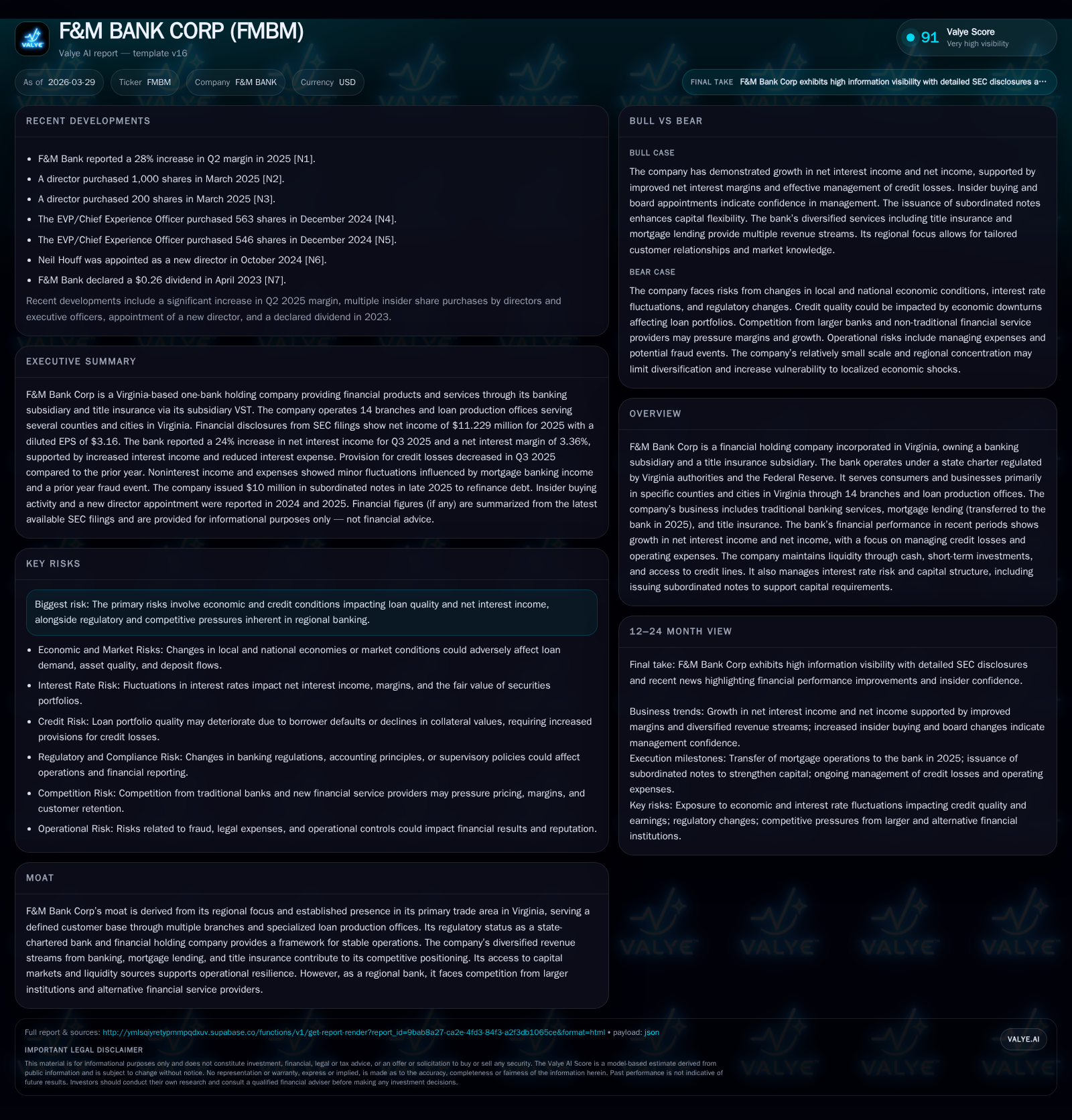

F&M Bank Corp Accelerates Profit Growth Leveraging Regional Strength and Diversified Services

The bank's focused regional presence in Virginia and integration of mortgage and title insurance businesses underpin a 54% net income increase in 2025.

F&M Bank Corp has achieved substantial earnings growth through its concentrated market strategy across select Virginia counties, expanded service offerings, and prudent financial management. In 2025, net income surged over 50%, driven by rising net interest income and diversified fee income from title insurance and card services. The company maintains solid liquidity supported by a sizeable securities portfolio and credit lines while managing interest rate and credit risks proactively. Capital levels strengthened with an equity base exceeding $104 million, supporting resilience amid evolving regulatory landscapes.

Regional Foundations: Historic Growth Drivers and Market Position

F&M Bank Corp roots its competitive moat in a well-defined regional footprint spanning several Virginia counties including Rockingham, Shenandoah, Augusta, Frederick, and the cities of Harrisonburg, Staunton, Waynesboro, and Winchester [S2][S9]. Operating as a state-chartered bank under Virginia regulation and Federal Reserve supervision enables it to deploy tailored financial services attuned to this community banking niche. Its network encompasses 14 branches supplemented by specialized loan production offices targeting mortgage and dealer financing channels.

The company’s business model historically leverages three core revenue streams: traditional deposit-taking and lending activities; mortgage banking (integrated into the bank subsidiary as of Q2 2025); and title insurance through its VST subsidiary [S2]. This diversification fortifies revenue stability against localized economic cycles and competitive headwinds within the financial services sector.

Reviewing historical financials shows steady progression with notable inflections coinciding with strategic initiatives such as mortgage operation integration [F1]. This structure provides a stable platform for deposit accumulation through strong trade area penetration—a critical factor given the ongoing competition from larger institutions seeking scale advantages.

Historical Financial Performance

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 11 | 17 | 1 | +54.1% |

| 2024 | 7 | 7 | 0 | +162.9% |

| 2023 | 3 | 2 | 5 | -66.7% |

| 2022 | 8 | 40 | 4 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 16 | 10.7 |

| 2024 | 7 | 8.5 |

| 2023 | -3 | 3.5 |

| 2022 | 36 | 11.7 |

Source: SEC companyfacts cache [F1].

This table highlights significant earnings acceleration in FY2025 alongside robust cash flow generation supporting capital allocation flexibility [F1].

2025 Performance Highlights: Revenue, Income, and Expense Dynamics

FY2025 marked a pronounced acceleration in profitability for F&M Bank Corp as net income jumped by approximately 54% year-over-year to $11.23 million [F1]. Underpinning this surge was a meaningful increase in net interest income reaching approximately $30.5 million for the first nine months of 2025—a growth of nearly $5.6 million versus prior year—driven primarily by an expanding loan book alongside improving net interest margins which climbed roughly 60 basis points to over 3.3% at September-end [S10][S28].

Noninterest income contributed positively with an approximate $281,000 increase fueled largely by robust title insurance premiums reflecting higher closing volume plus gains from card services post-renegotiated interchange contracts [S10][S22]. These helped offset declines in mortgage banking income tied to lower originations due to market interest rate impacts.

Noninterest expenses increased about $1.3 million primarily due to rising personnel costs—including salary adjustments—legal/professional fees increases, data processing enhancements supporting operations, alongside pension-related expenses which rose following increased periodic pension costs despite settlement gains recorded prior year periods [S10][S22]. Expense increments were partially offset by absence of prior external fraud loss.

This dynamic resulted in overall strong earnings performance despite incremental cost pressures related mostly to investments in operational capabilities essential for long-term service quality.

Interest Rate and Credit Risk Management: Navigating Industry Headwinds

Interest rate volatility remains a key risk exposure area given prevailing macroeconomic uncertainties [S4][S26]. The Company employs an Asset-Liability Committee (ALCO) tasked with monitoring interest rate sensitivity and shaping mitigation strategies [S26].

The securities portfolio—a core tool in interest rate risk management—is weighted mainly toward high-quality U.S. Treasury instruments alongside agency-backed mortgage securities aligned with duration targets supporting liquidity readiness while buffering earnings fluctuations caused by repricing gaps between assets and liabilities [S7][S13].

Dynamic repricing efforts on loans (especially variable-rate products) combined with shifting deposit composition toward more savings accounts over time deposits compressed cost of funds from around 3.18% down to approximately 2.7% year-over-year at September-end boosting net interest margin expansion [S6][S28].

Credit risk oversight remains vigilant; provision for credit losses increased modestly to about $1.6 million in the first nine months of 2025 compared with prior periods consistent with portfolio growth yet reflects conservative coverage metrics especially within commercial real estate and automobile loan segments [S10][S12][S17]. Allowance levels remain adequate relative to nonperforming assets maintaining coverage ratios above 100%, underscoring prudent credit loss reserves [S7].

Capital Allocation Priorities: ROE, Cash Flow Trends, and Shareholder Returns

Capital structure analysis reveals an equity base nearing $104.8 million at December year-end 2025 representing significant build-up from prior years ($86.1 million at end-2024) [F1]. The approximate return on equity for FY2025 stands around a healthy 10.7%, reflecting efficient earnings leverage within its capital framework [F1].

Operating cash flows more than doubled year-over-year surging from $7.49 million in FY2024 up to over $16.5 million in FY2025 driven by improved core earnings quality along with working capital dynamics [F1]. Meanwhile annual capital expenditures remained low at under $750 thousand enabling free cash flow generation near $15.8 million—a strong funding source supporting organic growth or potential capital returns without compromising liquidity cushions.

The company executed modest share repurchases totaling roughly $400 thousand during FY2025 evidencing prudent use of excess capital for shareholder value enhancement [F1]. Dividend policy details remain limited within filings but retained earnings growth supports capacity to sustain future payouts should conditions warrant.

Diversification Strategy: Mortgage Lending Integration and Title Insurance Contributions

A pivotal strategic move was completed in Q2 2025 whereby F&M Mortgage’s operations were formally consolidated into the banking subsidiary streamlining lending workflows under unified regulatory oversight [S2]. This integration enhances product cross-selling opportunities leveraging existing customer relationships while improving operational efficiency through reduced structural complexities.

Title insurance via VST has proven a vital component augmenting fee-based revenues that diversify income away from interest rate cyclicality common among lending-focused institutions [S2]. Growth here stems from increased transaction volumes facilitated by active residential real estate markets within their service regions—a distinct advantage over peers lacking this vertical integration.

The expansion of card services reflecting renegotiated interchange agreements further bolsters noninterest income streams indicating effective utilization of modern payment ecosystems contributing stable revenue sources beyond traditional deposit services.

Liquidity Profile and Debt Structure: Balancing Flexibility with Prudence

Liquidity remains ample with liquid assets around $110 million equating roughly to an 8% share of total assets providing safety buffers against depositor fluctuations or credit demands [S4][S9]. Significant holdings in available-for-sale securities add flexible collateral options while ensuring relatively stable fair value amid interest rate movements.

Access to external funding lines includes broad federal funds unsecured lines totaling approximately $90 million plus a secured borrowing facility of about $168 million via the Federal Home Loan Bank underpinned by qualifying loan collateral pledges [S4][S9]. This multi-channel liquidity infrastructure supports tactical balance sheet management adapted to market conditions.

The issuance of subordinated notes during late 2025 updated capital instrument terms introducing SOFR-linked floating coupon structures replacing older fixed rates securing cost-effective permanent capital improving cushion layers aligned with Basel III equivalents for regional banks [S5][S25].

Forward-Looking Indicators: Outlook on Growth Opportunities and Operational Constraints

Forward-looking commentary from management signals careful balancing between leveraging economic momentum within their insured trade areas while remaining cautious about downturn risk potentials including loan demand softening or weakening credit quality trends amid inflationary pressures or changing Fed policies [S2][S20]. Rising competition from both traditional large financial institutions extending local footprints alongside fintech entrants poses ongoing challenges requiring continued product innovation and service excellence.

Maintaining or improving asset quality metrics while sustaining margin expansion efforts through dynamic liability mix adjustment will be critical milestones ahead for preserving profitability trajectories amidst interest rate uncertainty.

Capital ratio stability will demand ongoing vigilance given possible regulatory evolutions affecting smaller regional financial holding companies with respect to leverage thresholds or stress testing outcomes.

Governance Update and Strategic Leadership Moves

Governance enhancements include appointing Bret V. Harrison as a director on January 27, 2026 bolstering board expertise coinciding with recent results releases suggesting intent towards reinforced oversight capabilities especially regarding risk management policies amid complex macro-financial dynamics confronting regional banks today [S3]. Such moves align well with best practice frameworks emphasizing proactive director involvement in strategic risk domains.

This analysis synthesizes information solely available from referenced SEC filings ([F1], [S#]) without speculative assumptions or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments