Hydrofarm Faces Steep Financial Hurdles as Liquidity Worsens in 2025

Hydrofarm’s significant operating losses paired with severe liquidity shortfalls challenge its growth trajectory and capital structure stability.

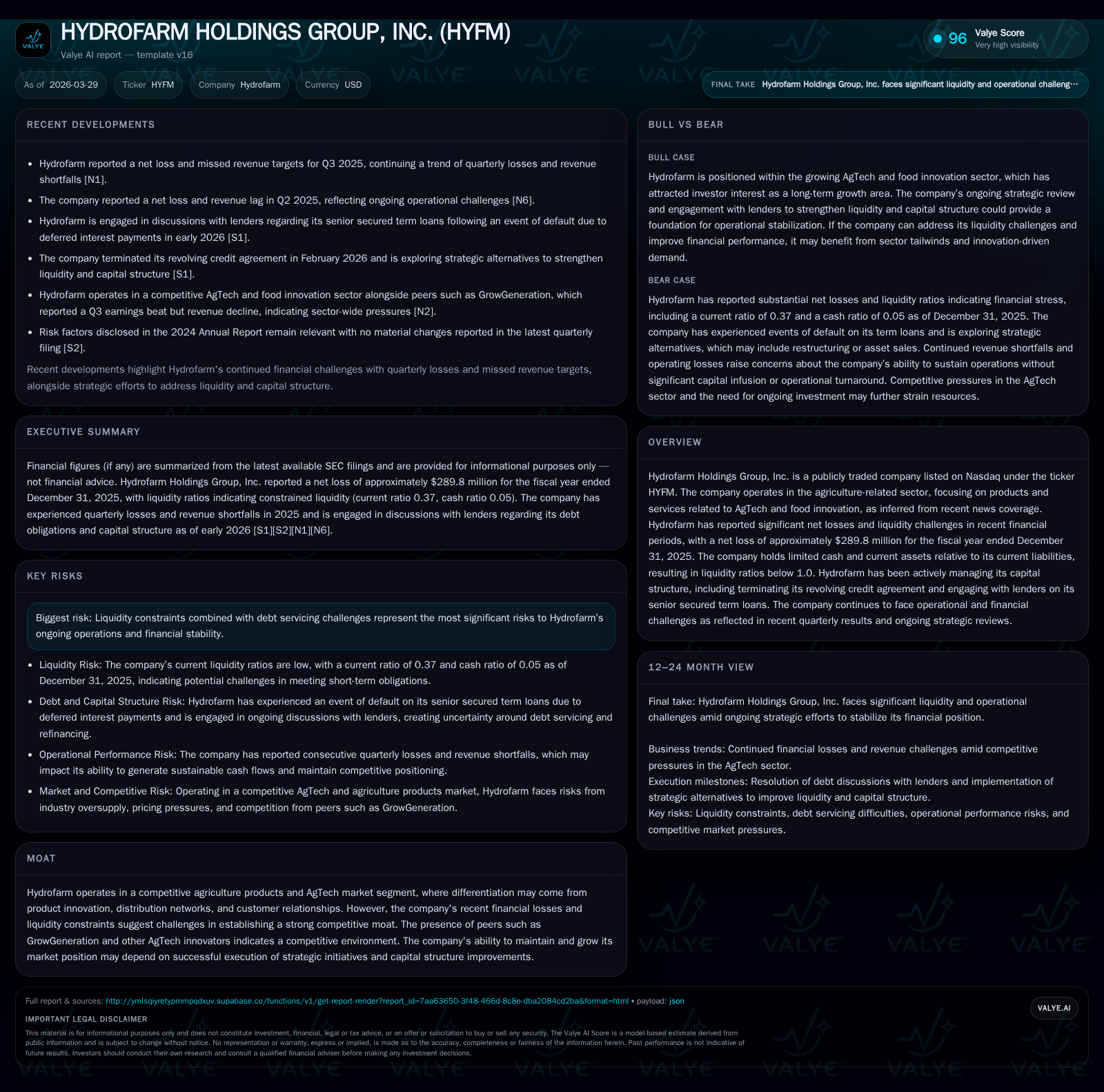

Hydrofarm Holdings Group, Inc. endured a marked deterioration in financial performance during fiscal year 2025, recording a net loss nearing $290 million and operating income plunging over 430% year-over-year. Liquidity pressures intensified, with a critically low current ratio of 0.37 driven by cash and current assets far below current liabilities. The firm’s capital structure is strained by events of default on senior secured term loans, prompting management to engage lenders in strategic discussions. Despite ongoing efforts, Hydrofarm’s ability to resume growth is constrained by its financial stresses and competitive market realities.

A Sharp Shift: Hydrofarm’s Recent Financial Performance and Its Drivers

Hydrofarm Holdings Group, Inc.’s fiscal year 2025 was marked by a steep decline in financial results that signal severe operational strain. Operating income deteriorated dramatically from -$52.2 million in FY2024 to -$276.9 million in FY2025, representing a drop exceeding 430% year-over-year [F1]. This pronounced margin pressure likely reflects unfavorable cost structures amid market oversupply conditions common in the agriculture product sector, compounded possibly by elevated SG&A expenses or impairments referenced generally in filings but without granular breakdowns.

Net income followed this negative trajectory, with the loss widening more than threefold from -$66.7 million to nearly -$289.8 million in the latest fiscal year [F1]. This magnitude of loss undermines equity base strength as shown by equity plummeting to negative $63.3 million by FY2025-end compared to a positive $223.7 million one year prior [F1], underscoring erosion of shareholder value.

Operating cash flow turned sharply negative to approximately -$14.1 million versus a modest negative of $0.3 million a year earlier [F1], indicating deteriorating core business cash generation. Capital expenditures concurrently reduced by nearly two-thirds year-over-year to about $1 million yet remain insufficient to offset cash burn [F1]. This snapshot portrays an entity battling through sustained operational inefficiencies amid adverse industry dynamics.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -290 | -14 | -277 | 1 | -334.4% |

| 2024 | -67 | 0 | -52 | 3 | -2.9% |

| 2023 | -65 | 7 | -50 | 4 | +77.3% |

| 2022 | -285 | 22 | -282 | 8 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -15 | 457.8 |

| 2024 | -3 | -29.8 |

| 2023 | 3 | -22.3 |

| 2022 | 14 | -81.6 |

Source: SEC companyfacts cache [F1].

Note: Cash flows and income show marked volatility suggesting cyclical and structural headwinds.

Unraveling Liquidity Stress: Current Asset vs. Liability Mismatch Implications

Liquidity metrics capture the acute financial tightness faced by Hydrofarm entering 2026. The company's current ratio stands at an alarming 0.37, calculated from current assets of $51.4 million against current liabilities totaling approximately $140 million as of December 31, 2025 [F1]. Such a sub-1 current ratio signals that the firm does not have enough short-term resources even to cover near-term obligations without liquidity support or asset sales.

This mismatch exacerbates pressure on working capital cycles—a critical factor for agribusinesses where inventory management and receivables collection heavily influence cash availability. The limited cash balance at only about $6.3 million suggests scant buffer against operational disruptions or debt servicing demands [F1]. SEC disclosures detail ongoing discussions with lenders regarding term loans under its Credit and Guaranty Agreement emphasizing these constraints are central strategic issues for Hydrofarm management [S5][S10][S16].

Capital Structure Pressures and Term Loan Default Events

Hydrofarm’s capital structure has come under intense pressure following cumulative operating losses and liquidity erosion that led the company to terminate its revolving credit facility on February 17, 2026 [S10]. Termination leaves the company reliant on outstanding senior secured term loans initially set at $125 million principal issued under amended agreements from October 2021.

A key event transpired on February 4, 2026 when Hydrofarm elected to defer interest payments amounting to roughly $2.8 million on these term loans beyond allowed grace periods, triggering formal default notifications from lenders as per administrative agent roles outlined in financing contracts [S7][S10][S13][S16]. Although lenders have not pursued remedies immediately, company-lender negotiations continue actively aiming at restructuring or alternative arrangements.

These developments underscore substantial refinancing risk inherent in Hydrofarm’s debt profile—a salient consideration for credit evaluations—especially since revolving credit termination eliminates flexible liquidity sources while default clouds covenant compliance status.

Growth Prospects and Operational Challenges Ahead

Positioned within the agriculture products and AgTech market segments, Hydrofarm’s growth potential depends materially on innovation capacity, product differentiation, and operational scale efficiency amidst competitive pressures from peers like GrowGeneration [N1][S6]. However, recent operational setbacks coupled with constrained access to capital hamper expansions or R&D investment needed for sustainable advancement.

The company’s Board is undertaking comprehensive strategic reviews exploring potential pathways—including asset divestitures or recapitalization scenarios—to stabilize operations while pursuing selective growth initiatives consistent with financial realities [S3][S10]. Given prevailing industry oversupply trends impacting pricing power and margin resilience alongside funding difficulties noted above, realizing meaningful growth will require successful execution of these strategic adjustments.

Assessing Strategic and Financial Controls to Steer Recovery

Management disclosures indicate active engagement with financial advisors and lender groups as part of an ongoing strategic alternatives process aimed at improving liquidity profiles and restructuring debt commitments [S3][S10]. Although formal guidance remains absent pending outcomes, emphasis rests on preserving core business continuity while seeking feasible capital solutions.

Governance changes including leadership transitions observed during late 2025—with CEO William Toler assuming helm—reflect attempts to strengthen oversight amid crisis resolution efforts [S21][S22]. These measures suggest prioritizing operational discipline alongside financial control enhancements integral for recovery prospects.

Capital Allocation Realities: Cash Flow, Dividends, and Shareholder Returns

Hydrofarm’s cash flow pattern shows stark declines—operating cash flow declined over four-thousand percent compared to prior year moving into significantly negative territory (~-$14M) while capex expenditures reduced commensurately reflecting austerity measures aimed at conserving cash reserves [F1]. Free cash flow thus approximates negative $15 million indicating persistent net outflows draining liquidity further.

No evidence emerges of dividend distributions or share repurchase programs across recent filings suggesting curtailed returns toward shareholders consistent with preservation-focused capital allocation amid financial distress [S17][S21][S26]. Such posture aligns with typical practices among companies prioritizing solvency stabilization over distributions during downturn phases.

Critical Risks in Finance and Regulation

Principal risks revolve around Hydrofarm’s highly leveraged position compounded by weak liquidity metrics threatening covenant compliance within credit facilities potentially triggering accelerated repayment obligations or lender enforcement actions if unresolved promptly [S4][S6][S8][S9]. Competitive dangers derive from fast-evolving agricultural technology sectors requiring sustained innovation funding which tighter finances may jeopardize.

Regulatory risks include exposure inherent to litigation described broadly within SEC risk disclosures though no singular material legal contingency appears definitive at this stage but merits continuous monitoring given complex sector compliance demands [S4][S8].

What to Watch: Milestones, Financing Developments, and Market Dynamics

Investors and analysts should monitor several critical near-term indicators shaping Hydrofarm’s trajectory: successful refinancing or restructuring agreements resolving term loan defaults; forthcoming quarterly earnings for signs of operational stabilization; updates from ongoing strategic review outcomes disclosed through SEC filings or press releases; shifts in competitive positioning vis-à-vis peers enhancing relative market share; and any material changes impacting liquidity including working capital management effectiveness or asset monetizations [N1][S3][S16].

Navigating these elements will be crucial for evaluating whether Hydrofarm can overcome its current impediments and return toward sustainable growth normalization.

Disclaimer: This report is for informational purposes only based on publicly available information as of March 29, 2026. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments