CaliberCos Inc. Confronts Liquidity Strains with Strategic Shift to Digital Assets and Vertical Integration

The company balances a shrinking revenue base and recurring losses against expansion in digital assets and an integrated real estate platform.

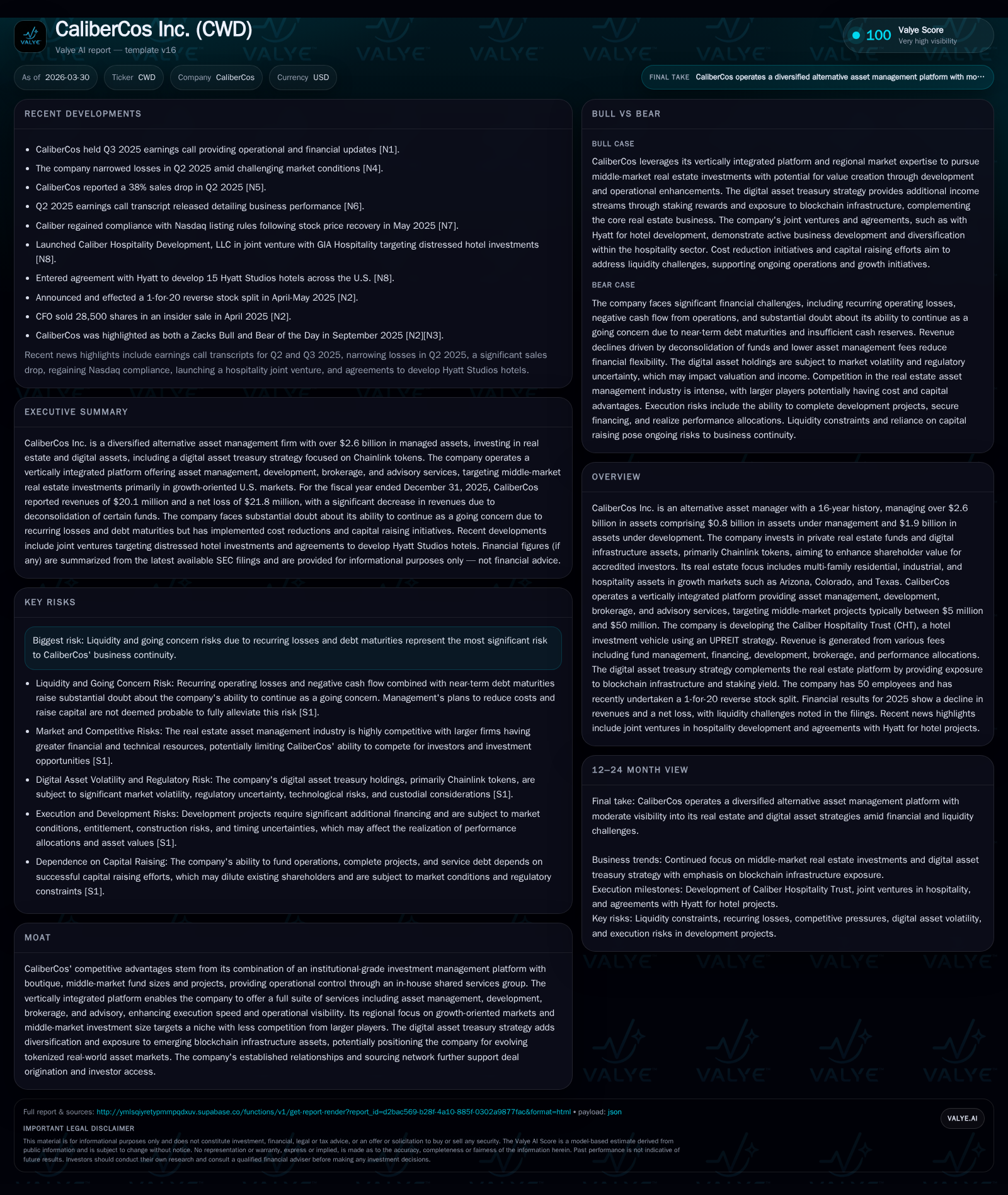

CaliberCos Inc., an alternative asset manager with a 16-year track record, manages over $2.6 billion across private real estate funds and digital infrastructure assets. Its core real estate focus spans middle-market properties in growth regions of the U.S., complemented by a growing digital asset treasury emphasizing Chainlink tokens. Despite strategic initiatives including vertical integration and fund innovation such as the Caliber Hospitality Trust, CaliberCos faces acute liquidity challenges highlighted by consecutive annual losses, significant debt maturities, and negative operating cash flows. Management’s active capital raising efforts and cost controls aim to address near-term funding pressures, while execution risks persist amid volatile fee-related earnings and a competitive investment landscape.

Historical Performance and Financial Overview

Founded over sixteen years ago, CaliberCos has established itself as a diversified alternative asset manager with a portfolio exceeding $2.6 billion comprising both assets under management (AUM) at about $0.8 billion and assets under development (AUD) near $1.9 billion [S1]. The platform predominantly invests in private real estate funds focused on middle-market projects valued between $5 million and $50 million alongside emerging exposure to blockchain infrastructure digital assets.

Fiscal year 2025 witnessed a stark revenue contraction of approximately 60.7%, falling to $20.1 million from $51.1 million the prior year [F1]. This material decline is attributed mainly to the volatility inherent in performance allocation income recognized upon realization events within funds—an area governed by accounting standards that defer income recognition until substantially certain [S14]. Net losses widened further to $21.8 million versus $19.8 million in 2024, continuing multi-year negative profitability trends [F1]. Operational cash flows also deteriorated severely from a modest positive of $0.55 million in 2024 to a negative outflow of approximately $12.1 million in 2025 [F1], underscoring growing liquidity pressures.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 20 | -22 | -12 | -60.7% | -10.2% |

| 2024 | 51 | -20 | 1 | -43.8% | -55.7% |

| 2023 | 91 | -13 | -19 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -1635.3 |

| 2024 | 157.1 |

| 2023 | -484.3 |

Source: SEC companyfacts cache [F1].

This table highlights the pronounced financial swings characteristic of CaliberCos’s business model dependent on fund performance cycles.

Business Model and Competitive Positioning

CaliberCos operates a vertically integrated platform overseeing asset management, development and construction management, brokerage activities, advisory services, and fund formation tasks [S24]. This unified operational approach delivers enhanced execution speed and operational visibility compared with fragmented outsourcing models prevalent among competitors [S10][S22]. The firm targets middle-market real estate investments emphasizing multifamily residential, industrial warehouses, and hospitality assets situated primarily in growth-oriented U.S. regions such as Arizona, Colorado, Texas with some exposure to Alaska and Kansas [S1][S22].

Vertical integration achieves cost efficiencies especially by allocating high-margin low-volume functions internally while outsourcing commoditized high-volume tasks—a balance that supports operational scalability without excessive overhead [S7]. The company typically pursues projects sized between $5 million and $50 million per asset with funds raised ranging from approximately $5 million for syndications up to around $200 million for multi-asset discretionary funds [S24]. Notably, CaliberCos has developed the Caliber Hospitality Trust (CHT), leveraging an UPREIT strategy structured for hotel investment with ambitions for a Nasdaq public listing contingent on surpassing a billion dollars in AUM [S24].

CaliberCos leverages localized market insights through its established relationships with property owners, financial institutions, and brokers within its target geography—a critical sourcing advantage amid intense competition from larger institutional investors who often operate at scale but may lack agility or regional expertise [S10][S22]. Their boutique middle-market focus also sidesteps direct competition with mega-funds that concentrate on large-scale trophy assets.

Digital Asset Treasury Strategy

A distinctive element of CaliberCos’s evolution is its formal adoption of a Board-approved Treasury Reserve Policy in August 2025 emphasizing accumulation of blockchain-based financial infrastructure assets—specifically Chainlink tokens (LINK) [S1]. LINK functions as a decentralized oracle network essential for enabling smart contracts to access external data securely.

Management views LINK’s entrenched enterprise adoption coupled with its foundational role in tokenization ecosystems as key reasons for inclusion as the inaugural digital treasury holding [S1]. Since policy adoption, CaliberCos has raised equity capital partially earmarked for acquiring LINK tokens valued at approximately $12.6 million as of late-2025 accounting records [S5]. These holdings are reported at fair value on the balance sheet subject to volatility that impacts reported earnings.

Further steps include plans to stake portions of the LINK treasury—a blockchain protocol activity contributing network security while generating yield estimated internally between 3%–9% annually—thereby augmenting non-traditional income streams [S1]. The company is also exploring validator-related operations on the Chainlink network which could generate supplemental revenue from protocol participation fees.

These digital initiatives aim to future-proof CaliberCos against shifting paradigms in asset tokenization by integrating traditional real estate investment platforms with decentralized finance constructs [S1]. Tokenizing fractional ownership interests may also broaden investor accessibility and liquidity channels beyond conventional fund structures.

Liquidity Profile and Capital Allocation Challenges

Despite strategic breadth across asset classes and geographies, CaliberCos confronts substantial liquidity headwinds accentuated by ongoing operating losses coupled with maturing debt obligations [S4][S11][F1]. At year-end December 31, 2025, unsecured promissory notes aggregated approximately $29.6 million bearing average interest above 11%, with principal maturities concentrated within twelve months post-report date—a critical liquidity risk vector given the company's available cash approximating only $2.9 million [S4][F1].

Management’s response includes multiple concurrent initiatives: raising approximately $6.4 million proceeds through Series AA preferred stock issuances under Reg A+, converting nearly $1.9 million of corporate notes into equity via conversion programs offering shares at prices between $3.14–$3.72 per share; refinancing shorter-term notes into longer-duration instruments; as well as implementing workforce reductions expected to yield annualized compensation savings near $3.9 million [S5][S6][S21].

Additionally planned tactics encompass accelerating collection on receivables totaling roughly $10.7 million plus investments of about $11.6 million from managed funds; monetizing or securing financing against corporate headquarters; expanding fundraising channels including ATM facilities; all designed to replenish working capital reserves while shoring up capital allocation flexibility [S5][S14].

Nevertheless, management acknowledges that these remediation plans face uncertainty outside their control resulting in sustained doubts regarding going concern status absent successful execution or market improvements [S5]. Substantial liabilities relative to company size curtail maneuverability compared with peers of similar or larger scale operating with lower leverage profiles [S21][F1].

Revenue Composition and Fee Streams

CaliberCos generates revenues primarily through various fee mechanisms embedded along the investment cycle within its asset management platform—the "Platform"—which excludes consolidated fund assets but captures revenues tied directly to fund management activities including:

- Fund management fees,

- Organizational/offering fees,

- Financing fees related to project loans,

- Construction management fees,

- Brokerage commissions,

- Performance allocations realized upon surpassing preferred return hurdles [S24][S8][S25].

Performance allocations produce significant volatility because they are recognized only upon realization events like sales or refinancing exceeding preferred returns typically ranging from 6%–12%. Such fee timing delays contribute materially to fluctuations in reported earnings relative to underlying economic progress within funds’ portfolios [S14][S25].

Digital asset treasury income derived from staking rewards or appreciation in LINK holdings introduces further earnings variability due to cryptocurrency market price swings; these gains/losses are recorded directly through consolidated statements impacting net income disproportionately versus cash flows from operations [S1][F1].

Future Prospects and Growth Drivers

CaliberCos’ future growth trajectory hinges on several elements:

- Scaling fundraising outreach beyond current high-net-worth individuals into institutional segments such as registered investment advisers (RIA), family offices and boutique institutions,

- Launching additional specialized funds/platforms potentially enhancing fee-related earnings,

- Progressing CHT toward listing should it exceed targeted AUM thresholds,

- Exploiting innovative blockchain applications for tokenized real estate offerings aiming at liquidity enhancement and global investor expansion,

- Realizing operational synergies from vertical integration accelerating deal execution speed amidst competitive pressures,

- Leveraging geographic specialization focused on business-friendly growth states avoiding oversaturated markets,

- Expanding digital asset treasury exposures cautiously subject to regulatory conditions while pursuing yield opportunities through staking/validator roles.

Notwithstanding these initiatives there remain significant constraints primarily relating to capital availability given maturing debt profiles coupled with continued top-line compression driven by competitive dynamics limiting acquisition potential or capital deployment velocity.

Risks Summary

While CaliberCos possesses differentiated capabilities combining traditional middle-market real estate investing with frontier blockchain infrastructure exposure supported by verticalized investment servicing capabilities, the most salient risk remains acute liquidity stress compounded by prolonged negative profitability measures requiring continual access to capital markets for survivability purposes [S11][F1]. Deteriorating credit conditions or disruption in investor demand might exacerbate difficulty refinancing debt or raising new equity thereby imperiling growth strategies.

Further risks derive from inherent volatility attendant upon performance allocation recognition timing; dependency on successful project development/acquisition pipelines; potential regulatory changes affecting digital asset strategies; technological implementation risks related to blockchain tokenizations affecting operational efficacy; rising inflation increasing construction costs adversely impacting project returns; evolving tax landscapes especially relating Qualified Opportunity Zone incentives recently extended indefinitely which could alter strategy effectiveness; legal exposure common within complex investment environments; reliance upon third parties for certain fund operations limiting total control; competition from better-capitalized sponsors poised aggressively bidding middle-market deals; dynamic macroeconomic interest rate environments influencing debt service costs—all warrant continuous mitigation attention going forward.

Conclusion

CaliberCos stands at an inflection point balancing foundational strength via sizeable managed assets coupled with innovative integration of digital infrastructure tokens against palpable near-term financial stresses emanating principally from insufficient liquidity coverage of obligations coupled with compressed operating cash flow generation arising from uneven realization-dependent incomes. Its mid-market focus combined with vertically integrated capabilities offers sustainable differentiation but necessitates robust capital management discipline amidst intensifying competition across alternative asset space. Monitoring forthcoming execution along new fundraising channels particularly Reg A+ initiatives supporting both corporate liquidity needs as well as expanded product suites like CHT will provide insight into feasibility of current turnaround trajectory. Natural earnings volatility stemming from performance allocation accounting rules will persist as inherent characteristic underpinning reported profitability fluctuations. Successful navigation mandates balancing cautious innovation adoption within digital asset treasury pursuits tempered by prudent leverage handling and rigorous cost controls executing parallel growth ambitions sustainably. Continued analysis should focus on post-report equity issuances outcomes alongside digital staking revenues realization versus market-induced valuation swings that may materially influence near-term reported results absent underlying cash generation improvements.

This analysis is based exclusively on disclosed filings and does not constitute investment advice or recommendations concerning financial securities or instruments mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments