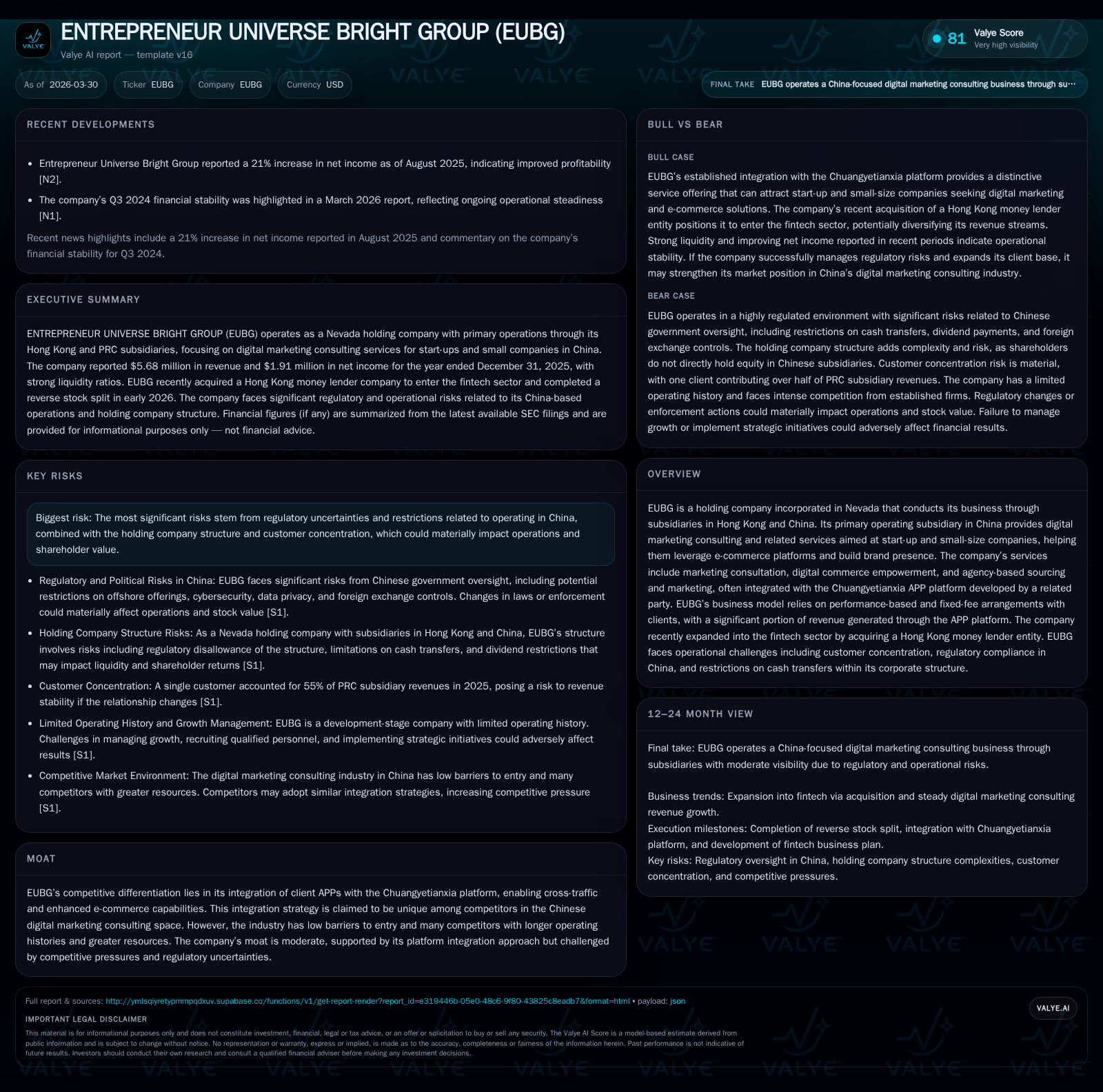

ENTREPRENEUR UNIVERSE BRIGHT GROUP: Platform Integration Spurs Steady 2025 Revenue Growth

EUBG’s integration strategy with the Chuangyetianxia APP and recent fintech acquisition underpin its steady expansion amid evolving regulatory and customer concentration risks.

Entrepreneur Universe Bright Group (EUBG) demonstrated modest yet consistent revenue growth of 7.7% in 2025, driven primarily by expanded digital marketing consultation services and integration with the proprietary Chuangyetianxia APP platform. The company’s unique platform synergy supports customer engagement for start-ups and small businesses seeking e-commerce acceleration. In February 2026, EUBG acquired Hong Kong fintech entity Heng Ying International Investment Limited, marking a strategic diversification into financial technology amid uncertainties related to license renewal. Key risks persist, notably high customer concentration—55% revenue reliance on one major client—and regulatory complexities tied to operating in China under a Nevada holding company structure. Strong cash flow generation balances these challenges, though capital returns remain limited.

Financial Evolution: Revenue and Profitability Trends Through 2025

Entrepreneur Universe Bright Group’s financial performance over recent years illustrates a trajectory of steady growth emerging from its relatively short operating history. Fiscal year (FY) 2025 revenue reached nearly $5.68 million, up from approximately $5.27 million in FY 2024, representing a year-over-year increase of about 7.7% [F1]. This improvement was driven largely by the expansion of its consultation services geared toward facilitating product sales for start-up and small enterprises in China [S1]. The company's net income grew even more robustly by nearly 28%, rising to just over $1.9 million versus $1.49 million in the prior year, indicating improving operating leverage and cost management.

Operating income moved upward by roughly 14%, reaching about $2.95 million in FY25 [F1], demonstrating increased efficiency despite incremental spending on operational activities or platform-related costs. Notably, capital expenditures surged significantly from under $2,000 in FY24 to approximately $117,000 in FY25—an indicative step suggesting reinvestment into technology or office infrastructure aligned with business scale-up plans [F1]. Meanwhile, operating cash flow (CFO) rose sharply by over 85% to around $2.52 million in FY25 from roughly $1.36 million the prior year, reflecting both profitability gains and effective working capital management [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 6 | 2 | 3 | 3 | +7.7% | +28.1% |

| 2024 | 5 | 1 | 1 | 3 | -15.5% | -34.8% |

| 2023 | 6 | 2 | 2 | 4 | +77.9% | +464.1% |

| 2022 | 4 | 0 | 0 | 1 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 2 | 2 | 18.2 |

| 2024 | 2 | 1 | 17.7 |

| 2023 | 2 | 25.0 | |

| 2022 | 0 | 5.9 |

Source: SEC companyfacts cache [F1].

The table summarizes key financial metrics evidencing EUBG's trajectory since FY22 along with notable year-over-year changes highlighting swings mainly impacted by business scale and market conditions.

Digital Platform Synergies Driving Growth and Client Acquisition

A defining feature of EUBG’s business model is its integration with the Chuangyetianxia APP platform, a digital commerce ecosystem developed by a related party that enables seamless connectivity among diverse client applications [S7]. This integrated APP platform facilitates cross-traffic generation where users of one client’s app are introduced to others within the same ecosystem enhancing marketing reach and accelerating brand awareness for small and startup clients primarily situated in China.

Over FY25, around 44.7% of total revenue was generated through services delivered over the APP platform compared to nearly full reliance (99%) on the same channel in FY24 [F1][S7]. This shift accompanies a gradual diversification of revenue streams wherein EUBG complements its previous predominance of performance-based fee structures (revenue share linked to client sales outcomes) with fixed monthly fees tied to newly launched digital commerce empowerment services designed to assist clients with ongoing brand exposure enhancement regardless of sales volumes [S7].

This strategic blending helps stabilize revenue flows amidst variable transactional results while reinforcing customer engagement through additional support personnel dedicated to digital empowerment efforts.

Strategic Leap into Fintech: The Heng Ying Acquisition and Its Implications

In early February 2026, EUBG broadened its operational scope through the acquisition of Heng Ying International Investment Limited—a Hong Kong-incorporated money lender licensed entity acquired for approximately HK$350,000 (~USD45,000) [S1][S3]. This move represents EUBG’s foundational step into financial technology (fintech), staking claims beyond pure digital marketing consultation into lending and financial empowerment sectors.

Currently held under Heng Ying is a money lender license pending routine renewal scheduled for April of this year [S3], after which management plans to initiate active operations aligned with broader fintech ambitions.

While this signals strategic diversification aimed at unlocking cross-sector synergies between e-commerce driven customer bases and tailored fintech services—the embryonic stage of Heng Ying’s operations coupled with license uncertainty introduces cautiousness concerning near-term contributions or regulatory hurdles.

Regulatory Framework Challenges in China’s Digital Marketing Landscape

EUBG operates at the intersection of evolving Chinese regulatory regimes tightly overseeing digital platforms, privacy protections, anti-monopoly enforcement, and foreign investment controls—all areas laden with uncertain interpretations that could materially impact operations [S6][S8][S21][S22].

Though not currently facing any government penalties or investigations regarding cybersecurity or monopoly practices [S21][S15], the company must allocate substantial resources towards compliance amidst stringent laws including the E-Commerce Law implemented in January 2019 which imposes responsibilities on online operators relating to merchant governance and consumer rights protection [S8].

Moreover, concerns persist regarding data privacy mandates requiring secure storage within Chinese territory as well as transparency around personal information handling—all factors potentially causing increased legal risk exposure and operational costs for EUBG’s subsidiaries that facilitate app integrations [S15][S16]. The complex overlay amplifies uncertainties particularly given EUBG’s holding structure whereby its principal operating company is located within mainland China but ultimate ownership rests offshore under Nevada jurisdiction—a structural nuance flagged as a material risk due to possible regulatory interference affecting shareholder value or business continuity [S14][S9].

Customer Concentration Risks and Their Impact on Stability

A critical vulnerability lies in customer concentration: Zhongchuang Boli Technology Holdings Co., Ltd accounted for approximately 55% of net revenues generated by EUBG’s PRC subsidiary during FY25 [S4][S9]. As Zhongchuang Boli serves as marketplace operator closely associated through related-party ties via the Chuangyetianxia platform it represents both strategic integration benefits yet potent dependency.

This level of concentration raises operational risks should contractual relationships be terminated or renegotiated negatively—potentially triggering sharp declines in revenues given limited alternative large-scale clients at present [S9]. Mitigation remains challenging due to focus on nascent start-up clientele with constrained bargaining power hence exposing EUBG to revenue volatility absent diversification progress.

Capital Allocation Overview: Strong Cash Generation Amid Limited Returns Policy

From a capital perspective, EUBG exhibits robust liquidity evidenced by cash & equivalents totaling just over $11 million at end-2025 compared against current liabilities approximating $1.3 million yielding an exceptionally strong current ratio above eight times coverage indicative of conservative balance sheet management [F1]. Operating cash flows boosted by profitable growth were reported at approximately $2.52 million translating to free cash flow around $2.4 million after deducting elevated capex spend totaling roughly $117 thousand for investments likely supporting technology infrastructure upgrades or capacity expansion initiatives [F1].

The company paid special dividends aggregating roughly $2.2 million during August-September periods in prior years but has not outlined explicit ongoing dividend strategies post-FY24 distributions noted [F1][S12]. Return on equity approximates a healthy near-18% mark pointing towards effective use of shareholders’ equity despite ongoing developmental phase needs.

The recently executed reverse stock split (1-for-10 ratio effective February ’26) reshaped share count dynamics primarily aiming at market listing compliance rather than direct capital return enhancement but could influence investor perceptions over time [S3].

What to Watch: Key Milestones and Indicators for Future Performance

Looking forward analysts should monitor several pivotal developments shaping EUBG’s future trajectory:

- The scheduled Heng Ying money lender license renewal in April ’26 will be critical for launching fintech operations planned post-acquisition; delays or denials here could raise strategic execution risks.[S3]

- Regulatory actions relating to China’s tightening oversight on offshore-listed companies—including scrutiny over information security compliance and anti-monopoly measures—may alter operational latitude or trigger adjustment costs impacting profitability.[S6][S21]

- Customer retention dynamics especially regarding Zhongchuang Boli as well as broadening client base beyond startups will be essential indicators reflecting revenue sustainability beyond concentrated contracts.[S4][S9]

- Expansion success within diversified consulting offerings beyond core performance-based fees towards fixed-fee empowerment services could stabilize cash flow visibility while maintaining competitive positioning using proprietary platform integration.[S7]

- Any modifications stemming from Chinese overseas listing regulations or further cybersecurity law implementations need continuous evaluation given structural holding complexities.[S14][S16]

Absent explicit company forward guidance [N1][S1], these milestones serve as key watchpoints informing assessment of growth momentum balanced against risk management effectiveness within an evolving external backdrop.

This analysis aggregates Entrepreneur Universe Bright Group's latest reported filings and public disclosures up to March 30, 2026, without projecting speculative investment outcomes or advising financial decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments