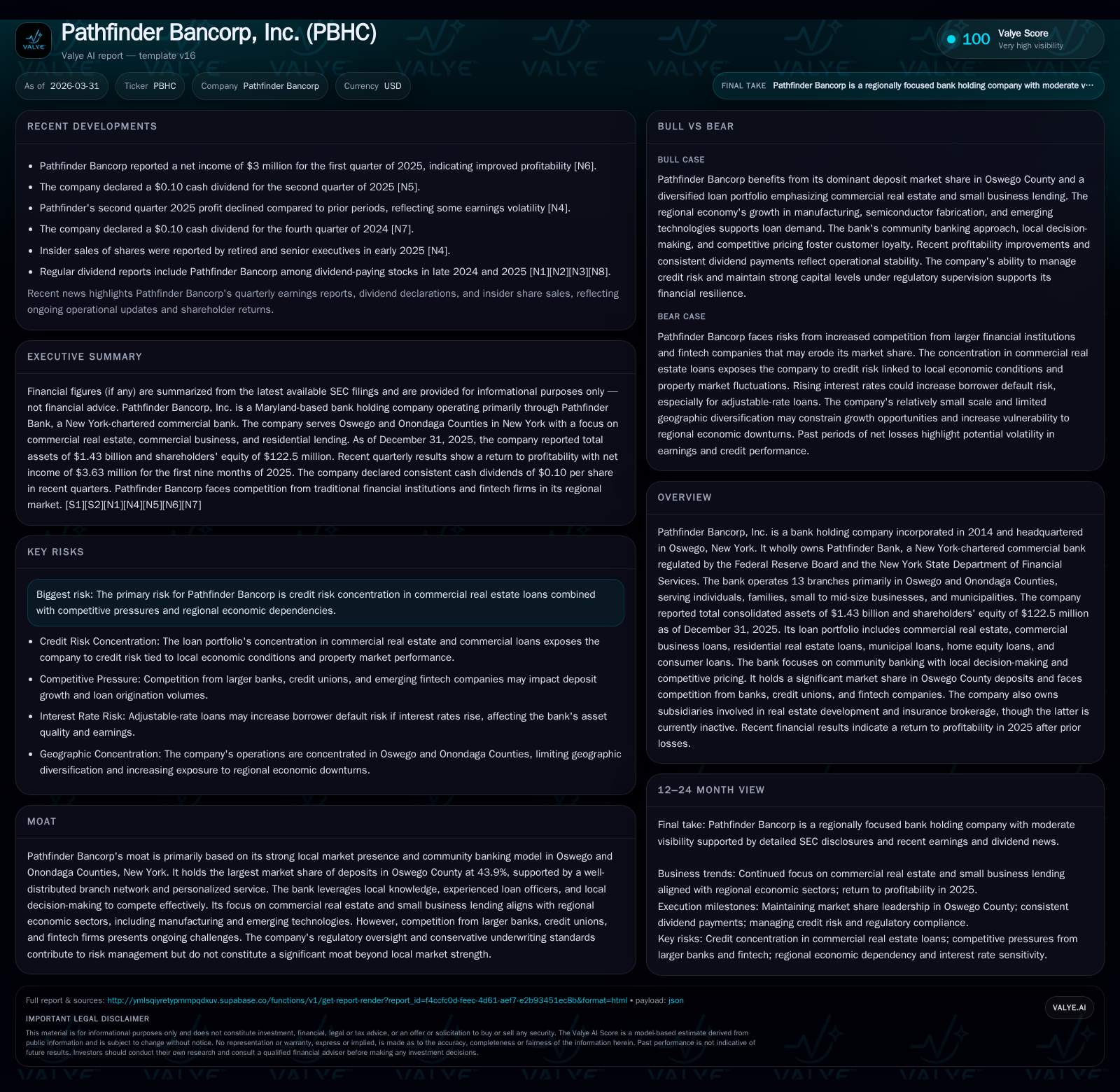

Pathfinder Bancorp’s Regional Banking Strength Tested by Income Volatility and Credit Concentration

Pathfinder Bancorp’s dominant deposit franchise in Oswego County confronts earnings pressure and loan portfolio risks amid evolving local competition.

Pathfinder Bancorp, Inc. maintains a commanding local deposit market share in Oswego County, supported by its community banking model and personalized service. However, its net income plummeted by over 157% year-over-year in 2025 due to increased credit loss provisions stemming from concentrations in commercial real estate loans and weaker asset quality. While operating cash flow remains consistently positive, the bank faces the challenge of balancing conservative underwriting with competitive pressures in its primary markets. Capital allocation shows steady dividend payouts despite earnings volatility, and management leverages a diversified funding mix including brokered deposits and FHLB borrowings to sustain liquidity. Looking ahead, growth opportunities rely on expanding commercial real estate and small business lending within Oswego and Onondaga counties, yet regulatory scrutiny and regional economic dependencies present ongoing risks.

Local Market Leadership and Historical Financial Performance

Pathfinder Bancorp operates through Pathfinder Bank with a stronghold in Oswego County, where it commands a dominant deposit market share of 43.9%, underscoring its entrenched local presence [S15]. Its branch network of 13 locations is well positioned throughout Oswego and Onondaga Counties to serve individuals, families, small- to mid-sized businesses, and municipalities. Total consolidated assets stood at $1.43 billion with shareholders’ equity at $122.5 million as of December 31, 2025 [S1].

Historically, Pathfinder exhibited solid profitability, with net income peaking at approximately $12.9 million in FY2022 before descending to a $1.93 million net loss in FY2025 according to company facts [F1]. The trajectory illustrates a pronounced income volatility driven primarily by changes in credit costs and loan portfolio risk exposure.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -2 | 12 | 1 | -157.1% |

| 2024 | 3 | 11 | 2 | -63.6% |

| 2023 | 9 | 15 | 2 | -28.1% |

| 2022 | 13 | 22 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 1908000 | 10 | -1.6 |

| 2024 | 1840000 | 9 | 2.8 |

| 2023 | 1690000 | 13 | 7.8 |

| 2022 | 1568000 | 20 | 11.7 |

Source: SEC companyfacts cache [F1].

Despite the steep decline in net income especially in FY2025 (-157.1% YoY), Pathfinder maintained robust operating cash flow ($11.7 million) demonstrating operational resilience even under profit pressure [F1]. The company sustained dividend payments totaling just under $2 million annually [F1], reflecting an emphasis on shareholder return continuity.

Earnings Volatility: Unpacking the Recent Net Income Decline

The transition from profitability to net loss in FY2025 is largely attributable to increased provisions for credit losses amid deteriorating asset quality [S2][S13]. As detailed in quarterly filings through late 2025 [S2], two significant commercial relationships shifted into nonperforming status during Q3 leading to a provision expense of $3.5 million for that quarter alone—a considerable burden relative to prior periods.

Management responded by initiating a comprehensive loan portfolio review covering loans over $500k—approximately representing 90% of outstanding balances—which targeted identification and mitigation of emerging credit risks ahead [S13]. This step evidences proactive risk management but simultaneously underscores the underlying volatility tied to concentrated exposures.

Loan Portfolio Composition and Credit Risk Concentration

Pathfinder’s loan book composition tilts heavily towards commercial real estate loans secured primarily by multi-family residential units and office properties within its local market footprint [S15]. While the bank has sought diversification through incremental commercial business loans and residential mortgage lending products—including fixed-rate residential real estate loans—their concentration poses vulnerability given regional economic dependence on manufacturing sectors alongside emergent but limited technology industry growth.

This concentration is further accentuated by geographic confines; Pathfinder draws customers predominantly from Oswego and Onondaga counties [S15]. The risk is compounded by substantial individual loan concentrations subject to regulatory ceilings—10% of Tier capital under internal policy limits—and state laws restricting unsecured exposures [S14]. Potential problem loans tagged as special mention or substandard rose notably to $66 million at September 30, reflecting increasing stress within specific borrower segments [S20].

Capital Structure Dynamics and Liquidity Mix Strategy

A key pillar supporting Pathfinder’s operations is its multifaceted funding approach blending core deposits ($1.18 billion total deposits end-2025) with supplemental borrowings through brokered deposits sourced via CDARS/ICS reciprocal programs as well as advances from the Federal Home Loan Bank of New York (FHLB-NY) [S4][S24].

At year-end December 31, 2025 deposits exhibited modest growth with strategic shifts favoring interest-bearing account types such as money market deposits [S9]. Approximately $152 million or nearly14% of deposits were uninsured on an FDIC basis but mitigated through reciprocal insurance arrangements or collateralized municipal funding programs enhancing deposit stability [S7][S9].

Borrowings showed a decline during 2025—down roughly $31 million—from reduced reliance on short-term FHLB advances following adjustments in liquidity preference [S19]. Meanwhile outstanding subordinated debt ($25 million issued October 2020) coupled with trust preferred securities totaling $5 million continued serving as Tier 1 capital enhancers subject to regulatory recognition uncertainties beyond current horizon [S21].

Liquidity is actively managed via established lines of credit aggregating over $240 million among correspondent institutions ensuring appropriate runway for lending activities even amid deposit fluctuations [S6][S7][S9]. ALCO oversight formalizes these policies aligning funding mix with balance sheet growth objectives.

Dividend Policy, Capital Allocation, and Return Metrics

Notwithstanding earnings swings into negative territory in FY2025 (-$1.93 million net income), Pathfinder declared consistent quarterly dividends culminating in approximately $1.91 million paid out during the year—reflecting a cautious capital distribution stance aligned with Federal Reserve guidelines favoring dividends out of current earnings but balanced against capital needs [S11][F1].

No share buybacks were reported recently; historical data suggests absence of repurchases from at least FY2017 onward implying focus remains on preserving capital rather than repurchasing shares amidst profitability challenges [F1][S11]. Return on equity reached an estimated negative -1.6% in FY2025 based on net income versus equity base—signifying pressure primarily rooted in elevated loan loss provisions eroding profits despite stable equity levels [F1].

Free cash flow generation remained positive at roughly $10.4 million (operating cash flow less capex), implying adequate operational liquidity to support ongoing dividend payments without immediate strain on core balances [F1]. Capital expenditures reduced materially by nearly 39% YoY as Pathfinder moderated investment spending consistent with slower growth environment.

Future Opportunities: Growth Outlook within Oswego and Onondaga Counties

While explicit forward guidance remains limited from recent disclosures [N/A], analysis suggests growth initiatives focused on expanding commercial real estate lending targeted to small business borrowers with typical deal sizes ranging from $500k up to $2 million—aligned with regional economic fabric comprising manufacturing hubs complemented by nascent technology ventures [S15].

Pathfinder’s deep local knowledge coupled with agile local decision-making confers advantages relative to larger competitors potentially less attuned to nuances of these markets; this may facilitate selective pipeline growth if credit quality can be stabilized post-loan review interventions.

Expanding municipal deposit relationships stands as another avenue given existing offerings tailored toward public entities within operative counties—though exposure includes seasonality requiring prudent liquidity buffers [S4].

Competitive Environment and Regulatory Risk Considerations

Competition arises not only from large New York-area banks but increasingly fintech firms targeting small business delivery models alongside specialized credit unions offering alternative community-based propositions . These rivals sometimes provide services beyond Pathfinder’s scope such as trust administration or private banking which may impact customer retention or acquisition especially among higher-net-worth segments.

Regulatory oversight by the Federal Reserve Board as a registered bank holding company plus supervision by New York State Department means compliance costs remain material along with requirements around capital buffers limiting aggressive growth or distributions under stressed conditions [S11]. Conservative underwriting remains critical safeguarding asset quality but also constrains risk appetite which could favor more nimble competitors willing to deploy looser criteria.

Key Milestones to Watch for Pathfinder’s Recovery Trajectory

Investors should monitor Pathfinder’s upcoming quarterly earnings releases focusing on trends in net charge-offs and provision expense trajectory reflecting effectiveness of the ongoing loan portfolio review concluding end-2025 [S13]. Shifts towards normalized credit cost levels would provide confidence regarding stabilization.

Dividend declarations remain a barometer for board confidence regarding capital sufficiency—next scheduled payout is May 8th , reflecting steady policy maintaining shareholder returns despite past losses [S3][S11]. Liquidity position updates including deposit mix evolution or changes in borrowing will further indicate ability to sustain lending while managing funding costs effectively.

Enhanced transparency on commercial real estate sector health locally—including occupancy rates or valuation trends impacting collateral values—would improve visibility into medium-term risk profiles impacting lender outlook beyond immediate fiscal periods.

This report integrates publicly available SEC filings and company facts data through March–April 2026 for informational purposes only without providing investment recommendations or price targets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments