Chilean Cobalt Corp: Unlocking Value from Northern Chile’s Cobalt-Copper District

Early-stage exploration and strategic partnerships define Chilean Cobalt's foundation for growth in a prime cobalt-copper district.

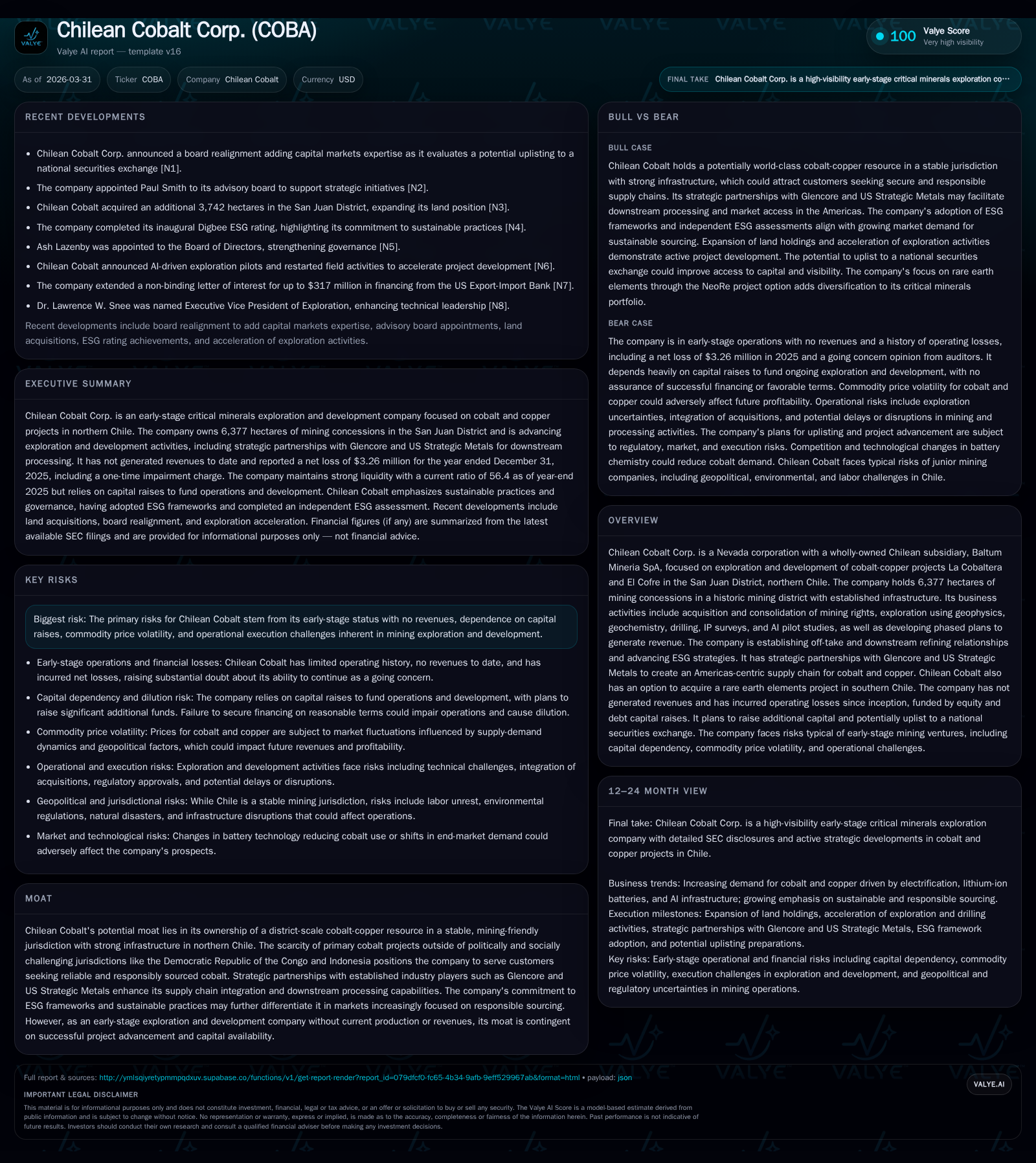

Chilean Cobalt Corp. operates as an early-stage cobalt-copper exploration company with no current revenues, focused on district-scale projects in northern Chile. Despite mounting operating losses and negative cash flows through 2025, the company has bolstered its land position and established significant alliances with Glencore and US Strategic Metals, aiming to build an integrated Americas-centric supply chain. Capital raises and governance enhancements reflect efforts to secure financial stability and credibility while preparing for potential uplisting, but ongoing operational risks and the absence of production remain substantial challenges.

Early Stage Growth and Historical Financial Performance

Chilean Cobalt Corp., through its wholly-owned Chilean subsidiary Baltum Mineria SpA, remains firmly at the exploration stage without any operating revenues since inception through fiscal year-end 2025 [F1]. Over the last four years (2022–2025), the company recorded continuous operating losses that notably deepened in FY2025 to approximately $-1.4 million — a nearly 56% worsening compared to 2024’s $-0.9 million loss [F1]. Net income has followed this worsening trend with FY2025 net losses ballooning to about $-3.26 million from $-0.88 million the prior year, translating into a negative return on equity (ROE) around -117%, highlighting unprofitable capital deployment amid expansion activities [F1].

Operating cash flows have remained negative throughout this period, expanding to over $-1.14 million in FY2025 versus $-0.79 million in FY2024 as expenses associated with exploration initiatives grew year-over-year [F1]. Despite this ongoing burn, Chilean Cobalt exhibits robust liquidity backed by a minimal current liabilities base (~$50k) versus current assets exceeding $2.8 million at December 31, 2025 — supporting an exceptionally high current ratio above 56x that cushions short-term financial pressures while awaiting development milestones or additional financing rounds [F1][S20].

Historical performance (annual)

| FY | Rev | Net ($mm) | CFO ($) | OpInc ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 0 | -3 | -1146473 | -1405174 | -269.7% |

| 2024 | 0 | -1 | -791706 | -899005 | +31.7% |

| 2023 | 0 | -1 | -929418 | -1312967 | -25.2% |

| 2022 | 0 | -1 | -673796 | -1033108 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -116.7 |

| 2024 | -201.7 |

| 2023 | -154.1 |

| 2022 | -157.8 |

Source: SEC companyfacts cache [F1].

Note: ROE calculated as (Net Income / Equity) ×100.

Exploration Advances and District Land Expansion

The core business activity underpins acquisition and consolidation of mining concessions totaling about 6,377 hectares within the historic San Juan District of northern Chile’s Atacama region — a mining-friendly jurisdiction offering established infrastructure including roads, power supply, water access, and port facilities; all crucial for eventual mine development costs containment [S1]. The district comprises the La Cobaltera and El Cofre projects well noted for containing copper oxide alongside cobalt-copper oxide and sulphide mineralization with indications of gold mineral potential at depth.

Recent news disclosed by Chilean Cobalt confirms accelerated exploration efforts including expanded landholdings particularly related to their NeoRe Rare Earth project—a separate ionic adsorption clay style REE deposit enriched with strategic elements like yttrium and neodymium critical for defense applications. This expansion aims at strengthening the company’s position within broader critical minerals supply chains beyond cobalt-copper deposits alone [N3].

Exploration methods are comprehensive comprising geophysical mapping techniques such as induced polarization (IP) surveys alongside geochemical sampling programs augmented by drilling campaigns aimed at resource delineation within district scale targets. Notably, AI pilot studies testing innovative analytical approaches demonstrate management’s intent to leverage technology for efficient resource identification—a forward-looking strategy uncommon among junior explorers [S1].

Strategic Partnerships and Offtake Agreements in Supply Chain Integration

Chilean Cobalt has strategically aligned itself with global commodity heavyweight Glencore Ltd., which holds first and last right of refusal on all cobalt and copper concentrate production from the La Cobaltera and El Cofre projects in perpetuity—reflecting an early commitment toward securing exit channels essential for project viability once production commences [S11]. This relationship serves both as a marketing anchor for customers seeking reliable sources of responsibly sourced metals amid growing scrutiny of supply ethics globally.

Additionally, collaboration with US Strategic Metals establishes further downstream refining relationships envisaged to create an integrated Americas-centric supply chain model—a competitive differentiator given ongoing geopolitical uncertainties surrounding cobalt sourcing predominantly centered in jurisdictions like the Democratic Republic of Congo (DRC) where supply chain disruptions remain acute [S1]. These partnerships aim not only at off-take but also at reinforcing ESG-compliant mining practices responding to escalating stakeholder expectations.

Capital Structure, Funding Activities, and Shareholder Returns

The company’s capital structure mirrors typical junior explorer dynamics focused on equity-based funding rather than debt instruments reflecting its nascent operational stage without revenue streams [F1][S20]. Noteworthy corporate actions include a forward stock split implemented on May 2, 2023 which issued three shares per existing share resulting in approximately a tripling of shares outstanding—a move likely designed to improve trading liquidity post private placements [S4].

Equity incentive programs feature prominently in retaining management talent with grants made under successive equity incentive plans approved between 2022–2023 encompassing stock options vesting over multi-year horizons signaling long-term alignment of interests [S16]. The absence of any dividend policy or share repurchase scheme is consistent with prioritizing capital allocation towards exploration expenditures and operational scaling rather than returning capital during this phase [S8][S11].

Recent financings include private placements notably raising net proceeds approaching $2.75 million in late 2025 priced at $0.50 per share evidencing continued investor appetite albeit likely dilutive given recurring capital needs documented by management’s warnings on going concern issues absent future raises [S11][S20]. Current cash on hand around $2.77 million sustains liquidity but is insufficient to cover forecasted annual expenditures exceeding $4.8 million requiring further fundraising imminently [S12].

Future Growth Catalysts and Development Constraints

Forward momentum hinges crucially on phased implementation plans emphasizing accelerated conversion of exploration success into defined mineral resources leading toward production feasibility studies—the latter still pending as the company advances geology-focused technical work aimed at economic resource delineation consistent with industry practice before large-scale development decisions can be made [N3][S1].

Demand-side growth factors include strong secular tailwinds from electric vehicle (EV) adoption requiring cobalt as a key battery cathode component despite potential medium-term substitution risks from emerging battery chemistries aiming to reduce cobalt content—introducing market uncertainty primarily tied to technological evolution beyond control of mining operators [S1].

Constraints derive mainly from known operational execution risks endemic to mining ventures; permitting complexities governed by Chile’s stringent environmental oversight; potential delays caused by Indigenous community consultation requirements increasingly embedded within ESG frameworks; as well as volatile commodity price environments affecting project valuation assumptions profoundly [S5][S7][S22].

Board realignment toward capital markets expertise announced recently underscores preparatory steps toward potential uplisting on a national securities exchange—an important milestone poised to improve access to larger pools of institutional capital necessary for scaling operations while imposing more rigorous corporate governance demands reflecting maturation trajectory [N1].

Governance Evolution and Market Positioning

Simultaneous announcements appointing experienced advisors such as Paul Smith augment board capabilities aligning leadership competencies with expected future operational scales—these moves serve dual purposes: boosting internal oversight mechanisms while enhancing credibility among investors sensitive to governance standards amid increasing scrutiny directed at ESG compliance frameworks such as IRMA and Digbee adopted internally since mid-2025 forming part of corporate social responsibility mandates across critical minerals sectors [N2][N1][S21].

This governance strengthening appears calibrated to address concerns associated with emerging growth company status while navigating complex permitting landscapes typical for mining projects located in politically stable yet regulation-intensive jurisdictions such as Chile.

Risks Specific to Mineral Exploration and Political Environment

Extensive risk disclosures elucidate foundational concerns: persistent operating losses heighten going concern doubts documented explicitly by auditors citing liquidity insufficiency without additional financing rounds; heavy dependence on successful capital raises exposing shareholders to dilution risks; inherent commodity price volatility especially cobalt and copper prices impacting potential project economics; stringent environmental permitting regimes coupled with evolving regulatory frameworks potentially delaying project timelines or imposing onerous remediation obligations; geopolitical risks including labor unrest common in Chile mining sector; legal exposure from environmental fines (including past small fine negotiation with CONAF detailed below); competitive pressures within developing critical minerals supply chains [S1][S5][S7][S14][S15][S19][S20].

Note: CONAF fine relates to vegetation disturbance incident self-reported in May 2019 potentially subjecting Baltum Mineria SpA to up to $4,000 fine possibly halved under mitigation but deemed immaterial overall. [/note]

Failure to meet escalating quality standards demanded by customers or government regulations could compound operational risk given reliance on third-party processors for cobalt compounds production—raising liability concerns around product specifications that may translate into contractual penalties or lost sales opportunities if unmet consistently [S24],[S25],[S26],[S28],[S29].

Key Milestones and What Investors Should Watch

Absent explicit forward-looking revenue guidance or definitive timelines disclosed publicly thus far, key near-term catalysts investors should monitor include:

- Continued assay results from expanded drilling programs focusing on resource delineation within La Cobaltera and El Cofre holdings along with NeoRe Rare Earth project advancements expected per March announcements reflecting accelerated field activity pacing efforts toward resource estimation thresholds [N3];

- Finalization and formal execution of off-take agreements clarifying volumes and pricing terms anchored by Glencore’s preferential rights coupled with downstream refining arrangements elucidating pathway toward monetization post-mineral extraction phases outlined conceptually so far but subject to negotiation dynamics inclusive of ESG clauses set forth within partners’ expectations [S11];

- Completion of ongoing board realignments plus additional governance disclosures potentially triggered by uplisting application preparations providing insight into corporate maturity metrics critical for institutional investor uptake enhancing trading liquidity profiles post-listing execution attempts projected through mid-to-late calendar year 2026 horizon [N1];

- Capital raise activities presumably required imminently given burn rate projections versus estimated cash reserves potentially involving dilutive issuances which will significantly impact share price dynamics along with operational continuity assumptions central for long term viability assessment amid prevailing economic uncertainties confronting junior explorers globally; any delays here could critically impair progress or lead to restructuring alternatives.

Overall, Chilean Cobalt remains emblematic of an emerging critical minerals junior player grappling simultaneously with balancing technical geological advancement against stringent financial discipline amid elevated market uncertainties — it embodies both opportunity afforded by district-scale cobalt-copper assets situated in favorable geopolitical terrain plus attendant risks typical for pre-production explorers.

This analysis is based exclusively on publicly filed documents including SEC Form 10-K disclosures through March 31, 2026 ([F1], [S#]), official press releases ([N#]), and company announcements without extrapolation beyond stated financials or proprietary data sources. It does not constitute investment advice or solicitations but aims solely at providing detailed factual insight into Chilean Cobalt Corp.'s historical performance, strategic positioning, operational status, capital activities, governance evolution, risk profile, and forward-looking considerations relevant for stakeholders evaluating early-stage critical mineral enterprises.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments