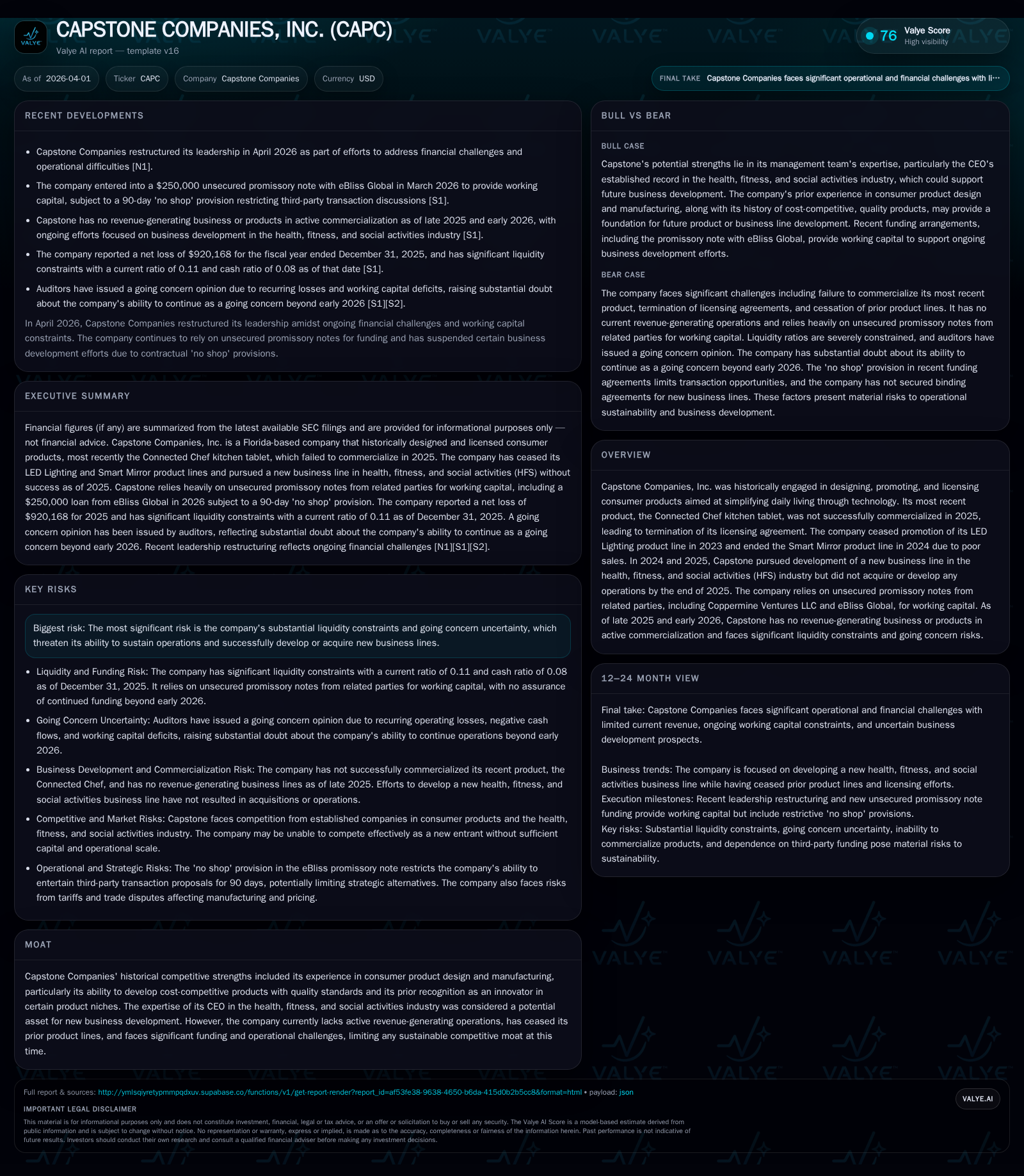

Capstone Companies Faces Critical Crossroads After Failed Product Launches

Capstone’s shift from consumer tech to health and fitness ventures unfolds under severe liquidity strain and operational suspension.

Capstone Companies, Inc. has seen a pronounced erosion of its consumer product business, culminating in the termination of key product lines like Connected Chef and LED lighting by 2025. Despite efforts to pivot toward the health, fitness, and social activities industry leveraging new leadership expertise, no tangible operations or acquisitions materialized through 2025. The company is now critically reliant on unsecured related-party promissory notes for working capital amidst substantial operating losses and a grim liquidity position, underscored by auditor going concern warnings. Its near-term viability hinges on raising new funding or securing strategic transactions during an ongoing ‘no shop’ period tied to recent debt arrangements.

From Innovation to Stagnation: Capstone’s Historical Revenue Decline and Product Exits

Capstone Companies, Inc. historically operated as a designer, promoter, and licensor of consumer products aimed at simplifying everyday living through technology. This legacy included several niche products such as LED lighting and smart mirrors alongside its more ambitious Connected Chef kitchen tablet initiative launched in the early 2020s. However, the company's top-line trajectory vividly illustrates an erosion starting from total revenues of approximately $346K in FY2022 descending sharply to stagnant levels around $143K for FY2023 and FY2024 [F1]. This decline directly correlates with strategic decisions to terminate unprofitable product lines: the LED Lighting product line ceased promotion in 2023, while the Smart Mirror line was abandoned by the end of 2024 due to poor market traction and inventory write-offs [S1].

This downward spiral culminated in no sustainable revenue streams by the close of fiscal year 2025 as Capstone lacked commercially active products or operations [S1]. The failure to evolve beyond these discontinued offerings marks a stark transition from previous decades of innovation into operational stagnation.

Failed Commercialization of the Connected Chef and Prior Product Line Shutdowns

The Connected Chef kitchen tablet represented Capstone’s last major attempt to reclaim relevance within consumer lifestyle technology. Developed throughout 2023 with an accessory platform designed for food preparation tasks, it incorporated Google Mobile Services compliant tablet technology—a notable edge in an emerging connected kitchen device segment [S1][S19]. Yet despite this promising framework, Capstone failed to transition Connected Chef into a viable commercial product during FY2025. The licensing agreement terminated without generating revenue, reflecting fundamental commercialization shortcomings including capital constraints and inability to secure distribution partnerships [N1][S1].

Such setbacks replicate earlier failures with the LED lighting division which had already been phased out by 2023 due to declining sales and competition. The Smart Mirror product also suffered poor consumer acceptance leading to complete shutdown after inventory liquidation in early 2024 [S1]. These failures highlight a recurring pattern where innovative concepts lacked execution horsepower or adequate funding support necessary for market success.

Liquidity Woes Defined: Working Capital Reliance on Related Party Notes

In absence of operating revenues since late 2024, Capstone has depended heavily on unsecured promissory notes extended predominately by related parties such as Coppermine Ventures LLC and more recently eBliss Global [S4][S5][S6]. Notably, Coppermine has provided multiple advances that cumulatively exceeded $530K through amendments executed during 2024–26 bearing simple interest at roughly seven percent annually [S5][S6]. Similarly, eBliss Global extended an unsecured loan exceeding $500K in March 2026 under terms that include a restrictive 'no shop' provision lasting initially ninety days—a contractual mechanism intended to prioritize discussions between eBliss and Capstone regarding possible business combinations or alliances without external interference [S26].

This reliance underscores acute working capital stress with reported deficits over $459K by December 31, 2025, alongside limited cash balances around $39K—insufficient for sustained operations without further influxes of capital [F1][S6]. Moreover, these financing instruments provide little security or conversion flexibility, intensifying the risk profile given Capstone’s precarious financial condition.

Strategic Shift Toward Health, Fitness, and Social Activities: Plans Without Execution

Starting late 2024, Capstone sought refuge in pivoting toward the rapidly expanding health, fitness, and social activities (HFS) sector leveraging leadership changes including appointment of Alexander Jacobs as CEO with direct industry experience via Coppermine Ventures [S20][N1]. Board restructuring introduced directors specialized in real estate transactions and business development aimed at facilitating acquisitions or strategic alliances within HFS.

However, despite these directional shifts accompanied by memoranda of understanding (MOUs) encompassing development plans for customer management applications aligned with Coppermine’s facility operations [S20], no actual acquisition or organic development was completed through fiscal year-end 2025 [S1]. The efforts morphed into exploratory pursuits hamstrung mainly by lack of working capital and suspended due diligence phases attributable in part to the eBliss note's 'no shop' clause restricting alternative deal negotiations during early 2026.

Financial Performance Snapshot: Operating Losses, Cash Burn, and Equity Erosion

Capstone’s financial trajectory until end-2025 characterizes a company hemorrhaging cash without offsetting revenues:

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 143269 | -1 | -282959 | -1 | 0.0% | +4.4% |

| 2024 | 143269 | -1 | -289548 | -1 | -25.4% | +43.3% |

| 2023 | 192176 | -2 | -614527 | -2 | -44.5% | +36.3% |

| 2022 | 346474 | -3 | -1904367 | -3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($) | ROE% |

|---|---|---|---|

| 2025 | 200.4 | ||

| 2024 | -332518 | -208.7 | |

| 2023 | 11662 | -657497 | 75.7 |

| 2022 | 11662 | -1936295 | 488.4 |

Source: SEC companyfacts cache [F1].

*Note: Revenue for FY2025 is reported with calendar year ending December 31st; prior years reflect latest annual filings as per company data [F1].

Operating losses exceed one million USD annually with mild deterioration seen between FY24–25 reflecting persistent negative EBITDA conditions compounded by declining net income losses partially offset by slightly improved net results in FY25 compared with FY24.

Operating cash flow remains negative but relatively stable around negative $280K-$290K yearly indicating ongoing cash burn syndrome sustained mainly via financing initiatives rather than internal earnings generation. Equity shifted negatively entering FY23 (-$2.24M) then improved somewhat ($461K positive mid-FY24) before returning negative again (-$459K in FY25), highlighting volatility tied likely to equity issuances related to preferred stock conversions for debt settlements [F1][S5]. These financial stress signals have fueled auditor issued going concern opinions highlighting existential risks.

Capital Structure and Funding Sources: Promissory Notes and Convertible Preferred Stock

In addressing stranded debt obligations stemming from prior lenders—many affiliated insiders or related parties—Capstone executed cancellation agreements converting principal balances into Series B-1 convertible preferred shares totaling over $3.6 million at an exchange price fixed at $0.07 per share [S5]. Such conversions effectively diluted common equity holding structures though represent non-cash charge relief permitting ongoing operation.

Coppermine Ventures is now a primary lender under amended promissory notes aggregating over half a million USD advanced between late-2024 through early-2026 accruing seven percent simple interest maturing late December next year [S5][S6]. In addition stands the sizeable recent extension from eBliss Global structured similarly but distinctly marked by an explicit 'no shop' clause that limits Capstone's ability to entertain other transaction proposals during initial three-month negotiation periods ending mid-2026 unless overtaken by superior offers [S26][N1].

The overall debt profile limits borrowing capacity given lack of collateralized assets while equity markets remain constrained due to market capitalization concerns coupled with penny stock status restricting broader institutional participation.

Operational Risks: Auditor Doubts and Going Concern Warnings

Auditors have expressed formal substantial doubt concerning Capstone’s ability to continue as a going concern for at least twelve months following fiscal year-end December 31st [S1]. This cautions stakeholders about heightened uncertainties leading potentially towards liquidation if adequate funding fails. Such opinions generally reflect:

- Negative equity trends compounded by accumulated deficits nearing $12.68 million,

- Persistent operating losses exceeding revenues,

- Inadequate operating cash inflows,

- Very limited liquid assets relative to liabilities,

- Difficulties accessing traditional capital markets while constrained asset base reduces financing options further. These disclosures intensify hurdles around raising fresh capital given elevated risk perception among investors while complicating new business acquisition prospects notably within health & fitness sectors requiring upfront investments.

Furthermore,the company's common stock trades on OTC Market Group QB Venture Market under penny stock designation aggravating liquidity scarcity impeding secondary trading volume vital for investor confidence [N1][S22].

What Investors Should Watch: Potential Milestones and Capital Raising Catalysts

Looking ahead there are several pivotal developments market participants should monitor closely:

- Expiration date of eBliss Note 'no shop' period around mid-2026 will re-open avenues for merger discussions or third-party proposals potentially altering strategic trajectory [S26].

- Any announcements regarding definitive agreements resulting from talks with eBliss Global or other third parties could materially influence Capstone's survival chances as operational status currently hinges on successful completion of transformative deals.

- Additional working capital raises either via debt or equity remain imperative if existing related party advances are not renewed post maturity dates spanning late 2026 timeline.

- Resumption or pivot back towards Connected Chef licensing might occur if HFS segment development proves infeasible given recent termination announcements impacting prior product lines retention strategies [N1][S26].

- Regulatory compliance adherence costs pose continuous baseline financial drains requiring funding regardless of commercialization success [S22]. Although speculative presently due to sparse concrete disclosures on forward-looking milestones beyond public filings,* investors face heightened risks tied primarily not only to commercial execution but also fundamental solvency constraints.*

Disclaimer: This analysis presents factual data derived solely from available filings and reputable news sources without forecasting outcomes or issuing investment recommendations. It provides an objective narrative framing Capstone Companies’ financial struggles amid strategic transitions emphasizing contextual understanding rather than predictive advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments