Jupiter Neurosciences Faces Solvency Challenges Amid Early-Stage Growth and Capital Reliance

Clinical-stage nutraceutical and pharmaceutical developer advancing JOTROL™ and Nugevia™ products under financial constraint.

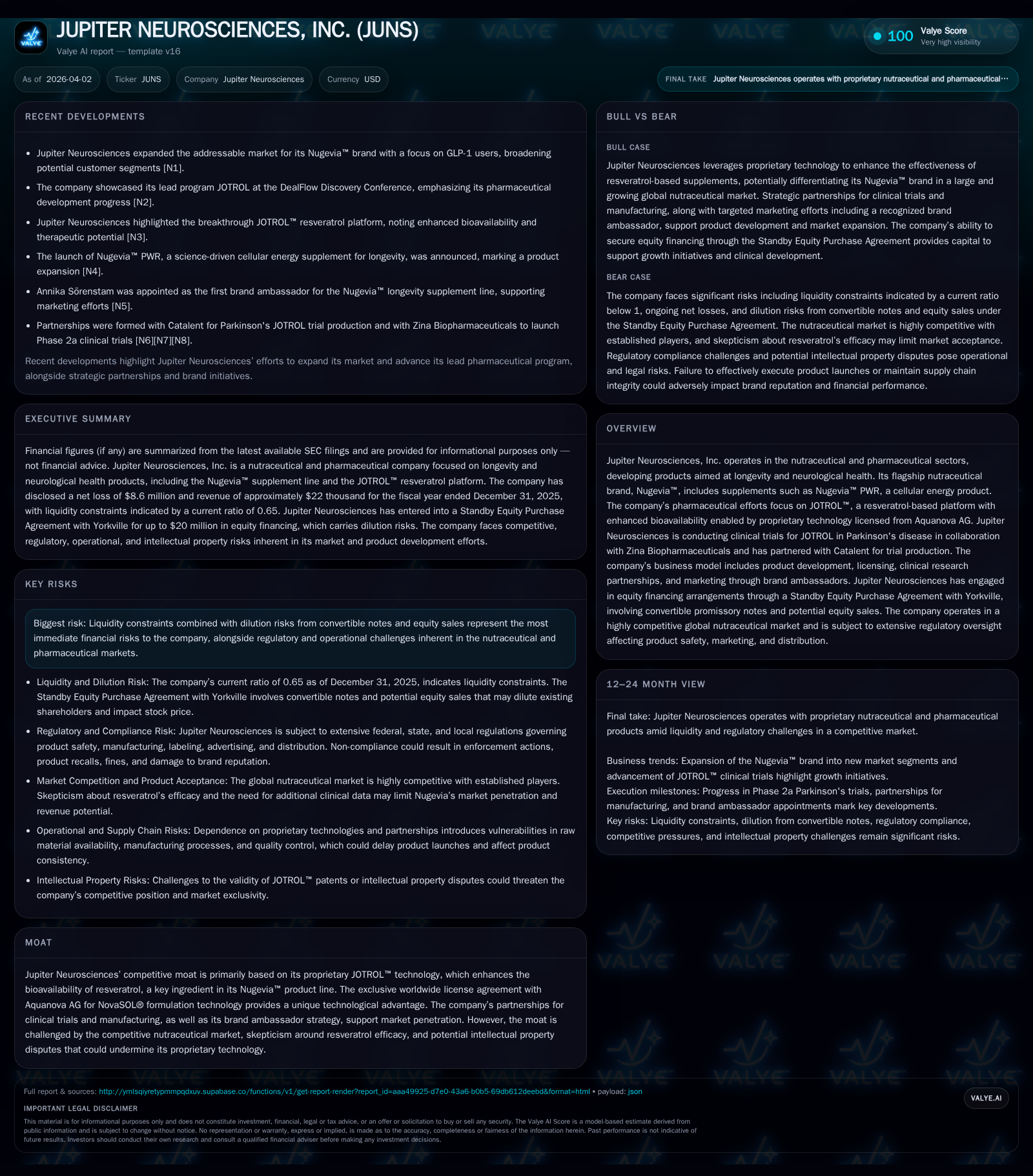

Jupiter Neurosciences, Inc. operates at the intersection of nutraceuticals and pharmaceutical development, focusing on longevity and neurological disease treatment via its enhanced resveratrol platform, JOTROL™. Although it has launched the Nugevia™ consumer wellness line, the company remains a clinical-stage entity with minimal product revenues and significant operational losses in 2025. Its growth depends heavily on ongoing clinical trials for Parkinson's disease and successful capital raises under a Standby Equity Purchase Agreement. However, its liquidity position, negative equity, and continued net losses raise material concerns about its going concern status and future financial flexibility.

Company Overview

Jupiter Neurosciences, Inc., incorporated in Delaware and trading on Nasdaq under JUNS since late 2024, concentrates its business efforts on developing neurological health treatments leveraging an improved oral resveratrol formulation known as JOTROL™. This proprietary platform utilizes NovaSOL® technology licensed exclusively from Aquanova AG to enhance bioavailability compared to traditional resveratrol compounds. Additionally, since early 2025, Jupiter has pursued the consumer nutraceutical segment through the Nugevia™ brand, particularly targeting longevity and wellness markets with formulations like Nugevia™ PWR.

From its founding in 2016 as Jupiter Orphan Therapeutics until rebranding in 2021, the company has transitioned from a pure drug development focus towards balancing pharmaceutical research with direct-to-consumer (DTC) supplement sales [S1].

Historical Financial Performance

Despite commercializing the Nugevia™ line initiated in H2 2025 using mainly social media marketing channels, revenue generation remains minimal. For fiscal year ending December 31, 2025, total revenue was reported at just $21,796.

Meanwhile, expenses have increased notably due to ongoing Phase IIa clinical trials for Parkinson's disease indications employing JOTROL™, higher production costs associated with Catalent partnerships, marketing investments for Nugevia™, and general administrative outlays.

Reported operating loss expanded drastically from $3.1 million in FY24 to $8.9 million in FY25 — a deterioration of over 188% year-over-year. Net losses mirrored this trend worsening by approximately 254% to reach $8.64 million at year-end 2025. Operating cash flows were similarly negative at around $5.4 million for FY25 compared to $3.9 million previously [F1].

These combined financial stresses led to negative shareholders’ equity of nearly -$1.8 million by the end of FY25 relative to positive equity of over $4.1 million one year earlier — mainly driven by accumulated losses exceeding capital plus asset book values.

Annual Financial Summary

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | -9 | -5 | -9 | -254.4% |

| 2024 | -2 | -4 | -3 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 471.9 |

| 2024 | -58.5 |

Source: SEC companyfacts cache [F1].

Note: Revenue figures represent primarily nascent direct-to-consumer nutraceutical sales; operating and net incomes reflect escalating R&D costs.

Growth Prospects and Future Catalysts

The core growth opportunity lies in successfully advancing JOTROL™ through its current Parkinson’s disease clinical trial phases and potentially extending into other neuroinflammation-related CNS disorders or rare diseases. Positive trial outcomes could validate the patent-protected enhanced bioavailability mechanism underpinning both therapeutic efficacy and differentiation.

On the consumer side, expanding the Nugevia™ portfolio offers near-term revenue upside by capturing increasing demand for scientifically backed longevity products. However, this market is deeply competitive and requires consistent marketing investment alongside clear evidence of product benefits.

Partnerships remain pivotal: Catalent serves as manufacturing partner for clinical supplies; collaboration with Zina Biopharmaceuticals supports trial execution; Asian region service agreements aim at market entry post-trial completion [S1]. These external relationships come with performance risk tied to milestone achievements.

Regulatory hurdles customary within pharmaceutical product approval pathways could delay or cap growth if results are inconclusive or adverse events arise.

Forecasts & Milestones to Watch

Formal company guidance is limited given its developmental stage; however key near-term milestones include:

- Completion data readout from Phase IIa Parkinson’s trial.

- Regulatory filings progress associated with JOTROL’s neurological indications.

- Expansion metrics from Nugevia™ sales volume and geographic reach.

- Incremental capital raises or SEPA tranche drawdowns impacting balance sheet strength and stockholder dilution. Monitoring announcements linked to these events will be essential to gauge viability of ramping operations toward profitability.

Capital Structure & Returns Analysis

In December 2024 Jupiter raised approximately $11 million gross proceeds through a public common stock offering priced at $4 per share [S1]. An additional liquidity facility involves a Standby Equity Purchase Agreement (SEPA) with Yorkville (YA II PN Ltd.) granting up to $6 million split into two convertible note tranches issued starting October 2025 [S2]. Yorkville holds conversion rights possibly leading to meaningful share dilution capped per Nasdaq rules.

Liquidity remains constrained—current assets totaled approximately $4.8 million against current liabilities near $7.4 million at year-end 2025 resulting in a current ratio below 0.65 [F1]. This pressured cash position coincides with repeated net operating cash deficits raising substantial doubt’s auditors expressed about continuing as a going concern [S1].

No dividends or buyback programs exist owing to extended periods of losses along with negative equity eliminating positive ROE calculations; approximated ROE figuratively exceeds 470% only due to negative denominator from equity deficit rather than genuine returns on capital deployed [F1].

Competitive Positioning & Risks

The exclusivity of Jupiter’s license from Aquanova AG for NovaSOL® boosts the perceived moat by facilitating high bioavailability resveratrol formulations unexplored widely by competitors.[S1] Nonetheless:

- Product efficacy skepticism persists particularly around resveratrol-based supplements impacting customer adoption.

- Intellectual property conflicts pose threats against Jupiter’s unique technological edge.

- Regulatory requirements for pharmaceutical development introduce long timelines plus potential costly trial failures.

- Substantial indebtedness paired with low stock trading volume limits efficient access to capital markets jeopardizing operational funding continuity.

- Non-refundable contractual fees payable under Asian service agreements without guaranteed deliverables increase financial vulnerability [S1].

Analysis Summary

Jupiter Neurosciences exemplifies an ambitious biotech start-up balancing pipeline development against early-stage consumer supplement commercialization within a highly capital-intensive sector marked by scientific uncertainty. Despite its innovative technology platform promising superior orally administered resveratrol absorption supporting neurological health claims through JOTROL™, it remains years away from meaningful commercial pharmaceutical revenues while enduring heavy liquidity challenges posing existential risks absent timely financing successes or breakthrough clinical milestones.

Investors should closely watch upcoming trial results related disclosures alongside continued capital raises under SEPA terms that will define whether Jupiter Neurosciences can transition beyond its current clinical-stage and cash-strapped status toward establishing itself as a viable participant within neurologic therapeutic avenues as well as niche nutraceutical categories focused on longevity enhancement.

Disclaimer: This report is for informational purposes only and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments