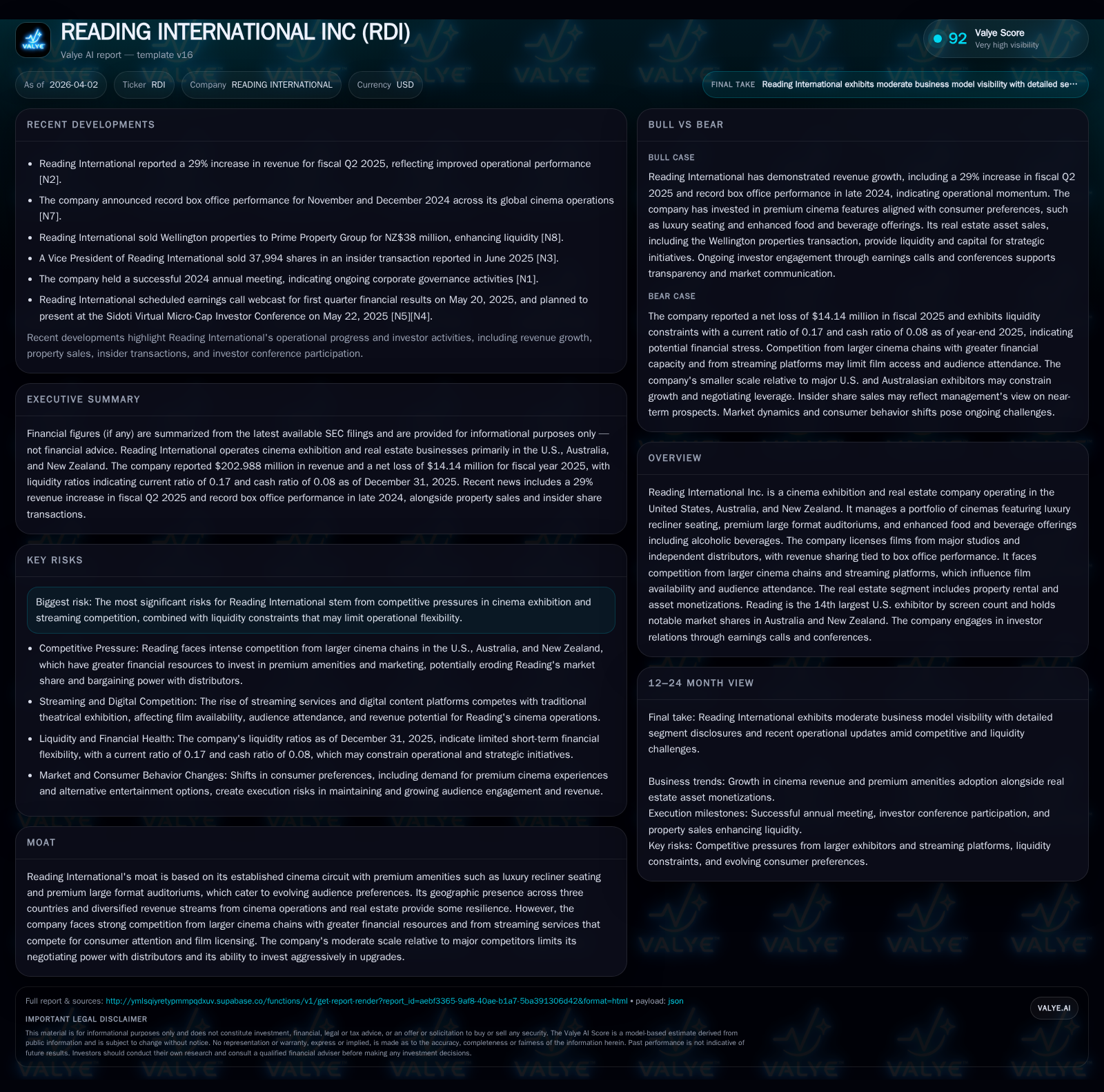

Reading International’s Multi-Market Cinema Operations Drive Performance Amid Tight Capital

Reading International leverages its premium cinema experience and real estate assets to support operational recovery while managing significant liquidity constraints.

Reading International Inc. operates cinemas across the U.S., Australia, and New Zealand, combining luxury amenities with a real estate portfolio that underpins its business resilience. Despite a modest revenue decline of 3.6% in 2025, operating losses narrowed by over 60%, signaling improved cost control amid competitive pressures from larger exhibitors and streaming platforms. The company faces tight liquidity highlighted by a low current ratio (~0.17) and substantial near-term debt but plans to mitigate this through ongoing real estate asset monetizations and refinancing efforts. Capital expenditures have contracted sharply, reflecting cautious investment, while no recent share buybacks or dividends have been reported. Future growth depends on continued premium experience demand, stabilization in box office returns, and successful execution of liquidity plans.

Revenue Trends and Operational Drivers Through 2025

Reading International Inc. posted revenues of approximately $203 million for fiscal year 2025, representing a decline of about 3.6% from $210.5 million in the prior year [F1]. While top-line softness reflects challenges facing the cinema exhibition industry—including consumer shifts toward streaming services and competitive pressure from larger chains—there are signs of operational improvement beneath the surface. Operating income losses narrowed sharply from nearly -$14 million in 2024 to about -$5.3 million in 2025, an improvement exceeding 60% year-over-year [F1]. This signals enhanced expense control or margin gains possibly driven by improved patronage for premium formats such as luxury recliner seating and premium large format auditoriums—areas where Reading has concentrated investment to meet evolving customer preferences .

Though the net loss remained negative at roughly -$14.1 million in 2025, this also improved substantially (about +60%) from prior years' deeper deficits [F1]. Moreover, operating cash flow losses shrank markedly to about -$1.6 million compared with nearly -$3.8 million in 2024 [F1]. These trends suggest incremental progress in profitability dynamics amidst a still-challenging environment.

Capital expenditures decreased considerably by roughly 76% year-over-year, falling to $1.33 million in FY2025 from nearly $5.54 million the prior year [F1]. This reduction reflects more cautious investment behavior likely driven by liquidity constraints and shifting strategic priorities.

Competitive Environment: Cinema Versus Streaming Wars

Reading International occupies a niche within the exhibition sector thanks to its multi-country geographic footprint spanning the U.S., Australia, and New Zealand combined with an emphasis on quality amenities such as luxury recliners and premium large format screens (). This positioning offers differentiation versus larger competitors who dominate market share but may not uniformly emphasize premium experiences.

However, Reading confronts strong competition both from well-capitalized cinema chains with greater scale negotiating power—and perhaps more diverse film licensing leverage—and from streaming platforms progressively encroaching upon box office audiences by offering anytime-anywhere convenience of content consumption (). The company's revenue model relies importantly on licensing arrangements tied directly to box office performance rather than fixed fees, which makes attendance trends crucial for its financial health.

The moderately sized scale relative to major competitors limits Reading's negotiating clout with distributors and impairs ability for aggressive technological upgrades or expansion beyond targeted luxury offerings (). Continued shifts in consumer behavior towards home entertainment impose persistent headwinds against growth.

Financial Health and Liquidity Status

Liquidity emerges as Reading's most significant immediate challenge. At December 31, 2025, current liabilities stood at approximately $128.6 million versus current assets near $21.8 million producing a current ratio around a precarious 0.17 [F1]. Cash and equivalents totaled roughly $10.5 million against near-term debt maturities exceeding $16 million [F1][S4][S5][S6]. Negative working capital consequently represents substantial short-term funding pressure.

The company has actively pursued refinancing and lenders have extended various debt maturities during 2025 including loans with Bank of America, Valley National Bank, Santander, National Australia Bank facilities, among others [S4][S6][S26]. Additionally, Reading has demonstrated capability to generate liquidity via real estate asset monetizations totaling over $200 million since 2021, with sales like the Cannon Park property ($20.7 million) contributing materially to debt reduction [S4][S12][S26]. Management emphasizes their belief that sufficient marketable real estate assets remain available for timely monetization required for ongoing obligations [S12].

Despite these efforts, lingering substantial doubt about going concern status persists as noted extensively in filings due to sizable liabilities against limited cash reserves [S4][S5][S12]. Nonetheless, no impairments were recorded through end-2024 or first nine months of 2025 based on discounted cash flow tests supporting recoverability of asset carrying values including goodwill [S4][S12][S17].

Historical Financial Performance

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 203 | -14 | -2 | -5 | -3.6% | +59.9% |

| 2024 | 211 | -35 | -4 | -14 | -5.5% | -15.1% |

| 2023 | 223 | -31 | -10 | -12 | +9.7% | +15.2% |

| 2022 | 203 | -36 | -26 | -28 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -3 | 77.5 |

| 2024 | -9 | 808.9 |

| 2023 | -14 | -92.7 |

| 2022 | -36 | -57.6 |

Source: SEC companyfacts cache [F1].

This table illustrates modest revenue declines alongside notable improvements in operating losses and cash flow dynamics over recent years despite ongoing net losses.

Capital Allocation Strategy

Reading International has adopted a conservative capital allocation approach amid financial pressures. Capital expenditures dropped significantly by approximately three-quarters between FY2024 and FY2025 [F1], reflecting cautious investment prioritizing liquidity preservation.

No dividends or share repurchases have been declared or executed since at least FY2020 [F1], indicating a focus on stabilizing operations and managing leverage rather than shareholder distributions [S18].

Outlook: Milestones and Expectations

Management's key near-term milestones revolve around successfully executing refinancing agreements extending debt maturities into late 2026 and continuing real estate asset sales to bolster liquidity [S4][S12]. These initiatives are critical to alleviating substantial doubt about the company’s ability to continue as a going concern.

Operationally, Reading aims to sustain momentum by enhancing premium cinema experiences across its markets in the U.S., Australia and New Zealand while navigating competitive pressures from larger exhibitors and streaming platforms (,[N1],[S1]). The company's diversified geographic presence provides some risk mitigation but requires ongoing adaptation to local market conditions.

Investor attention should focus on quarterly results revealing whether box office trends improve sufficiently to support sustainable profitability alongside progress on refinancing milestones ([N1],[S2]). Real estate monetization proceeds will remain a vital source of capital flexibility.

This memo is based entirely on publicly available data including SEC filings through March 31, 2026 [F1], news releases [N1], and company disclosures without speculative forecasts or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments