Israel Acquisitions Corp’s SPAC Journey: Delisting and Its Financial Crossroads

ISRLF confronts critical operational stagnation and capital constraints following Nasdaq delisting, underscoring pressing liquidity and strategic execution challenges.

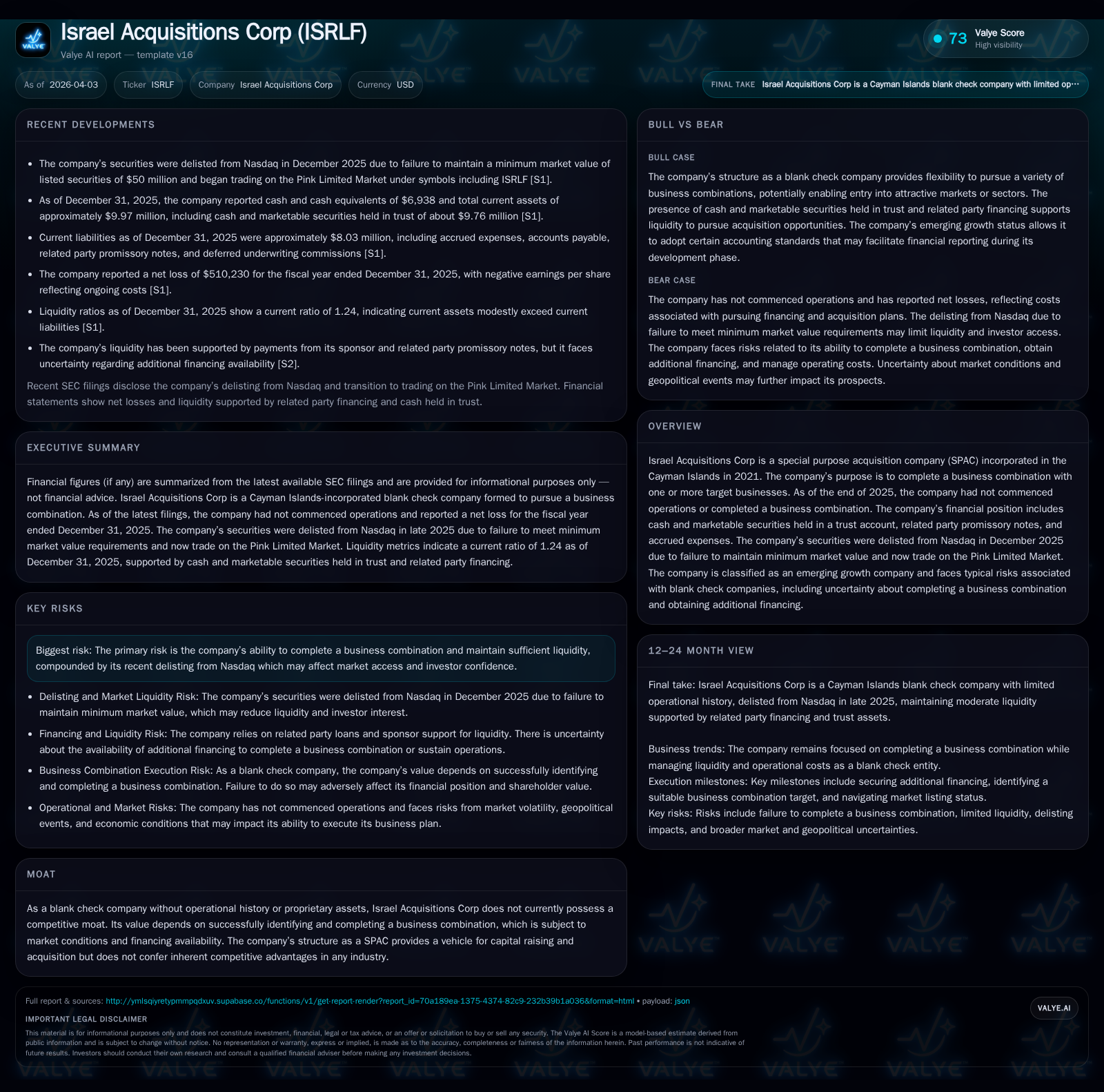

Israel Acquisitions Corp (ISRLF), a Cayman Islands-based special purpose acquisition company (SPAC) formed in 2021, has yet to complete any business combination as of the end of 2025. The company experienced cumulative operating losses with a modest improvement in operating income in 2025 but swung back to a net loss after prior net income gains, while its liquidity remained strained alongside a working capital deficit. Its delisting from Nasdaq in December 2025 due to minimum market value non-compliance has shifted trading to the Pink Limited Market, complicating capital access. Sponsor support persists via promissory notes and working capital loans; however, the absence of operational traction and looming redemption obligations weigh heavily on growth prospects.

SPAC Origins and the Absence of Operational Traction

Israel Acquisitions Corp was incorporated as a blank check entity under Cayman Islands law in August 2021 with the purpose of effecting one or more business combinations [S1][S2]. From inception through September 30, 2025, ISRLF conducted no operational activities nor generated revenues; its sole function has been managing proceeds from its initial public offering (IPO) and searching for acquisition targets [S1][S2]. As typical with SPACs, the company’s value depends entirely on completing a qualifying business combination within stipulated deadlines.

ISRLF holds no proprietary assets or revenue-generating operations; expenses relate solely to administrative costs and pursuit of acquisition opportunities [S1].

Historical Financial Performance: Loss Trends and Liquidity Metrics

Financially, ISRLF exhibits patterns common among pre-combination SPACs [F1]. Operating losses were approximately $1.05 million in FY2023, deepening to about $1.41 million in FY2024 before improving modestly to around $1.16 million in FY2025—a roughly 17% year-over-year improvement indicating some cost containment [F1].

Net income showed greater volatility: ISRLF reported net profits of $2.82 million in FY2024 largely due to accounting accretions related to redeemable shares but swung back into a net loss position of $510,230 by FY2025—a decline exceeding 118% year-over-year [F1]. This divergence reflects accounting treatments associated with redeemable shares liabilities under ASC 480 guidance typical for SPACs [S20].

Operating cash flow turned negative at approximately $258,324 in FY2025 after positive inflows near $3.35 million in FY2024 (-107.7% YoY), signaling tightening liquidity outside the trust account reserved for redemptions [F1]. The trust account itself—funded initially at about $146.6 million post-IPO—is invested exclusively in short-term U.S. government securities per regulatory mandates and cannot be used for daily operations or acquisitions prior to consummation of a business combination [S12].

Despite substantial trust assets, ISRLF displayed a working capital deficit that increased from about $1.45 million at end-2024 to over $2.48 million by September 30, 2025 excluding trust assets; concurrently, cash balances available for operations remained minimal (around $6,938 at year-end 2025) [F1][S6]. This highlights reliance on sponsor loans and promissory notes for bridging operational funding needs [S5][S22].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($) | Net YoY |

|---|---|---|---|---|

| 2025 | -1 | 0 | -1164266 | -118.1% |

| 2024 | 3 | 3 | -1409942 | -53.6% |

| 2023 | 6 | 0 | -1045934 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 74 | 6.4 |

| 2024 | 76 | -41.1 |

| 2023 | -125.3 |

Source: SEC companyfacts cache [F1].

Note: Buybacks represent Public Share redemptions pursuant to tender offers rather than traditional repurchase programs.

Delisting Dynamics and Market Implications

On November 24, 2025—the end of a six-month compliance period following notification—ISRLF failed to regain compliance with Nasdaq's Minimum Market Value of Listed Securities rule requiring at least $50 million aggregate equity value [S6]. Consequently, Nasdaq initiated delisting procedures culminating in removal from The Nasdaq Global Market by December 2025 [S6].

Following delisting, ISRLF's securities trade exclusively on the Pink Limited Market—a venue characterized by lower liquidity and regulatory oversight compared with national exchanges—which can impair trading volumes and price discovery.

This development complicates ISRLF's access to institutional capital markets amid ongoing delays completing its initial business combination.

Growth Prospects Within SPAC Constraints

ISRLF's growth prospects depend entirely on consummating qualifying business combinations valued at no less than approximately 80% of trust account assets with controlling interests sufficient to avoid registration as an investment company [S14].

As of late 2025 filings there is no disclosure of announced targets or definitive agreements; geopolitical risks including regional conflicts and macroeconomic pressures add complexity to completing transactions within extended timelines [S7].

Market volatility further challenges valuation rationales for potential targets and availability of third-party PIPE financing typically required alongside trust funds.

Sponsor Support and Capital Structure Risks

Sponsor support remains critical; as of September 30, 2025 related party promissory notes totaled approximately $1.85 million alongside accrued working capital loans providing interim liquidity for administrative expenses [S5][S22].

Trust account funds remain segregated strictly for shareholder redemptions or business combination funding—not daily operations—exposing ISRLF to funding risk if sponsor advances are curtailed.

No dividends have been declared; capital allocation focuses on managing trust assets and meeting redemption obligations.

Significant public share redemptions totaling over $73 million occurred during FY25 linked directly to shareholder exit rights exercised amid delayed deal closures [F1][S25], shrinking equity base while increasing redemption liabilities that negatively impact reported equity under GAAP.

Redemption Rights and Shareholder Value Implications

Public shareholders hold mandatory redemption rights if an initial business combination is not completed within prescribed deadlines or earlier if triggered by amendments—entitling them to cash payments from trust account balances that extinguish equity interests except warrants which expire worthless without deals consummated [S9].

This mechanism caps upside absent transactional success while creating downside risk through dilution and redemption liabilities.

Outlook and Upcoming Milestones

No explicit forward guidance is provided; key events to monitor include:

- Any extensions or amendments relating to the Combination Period beyond last known deadlines;

- Announcements regarding potential acquisition targets or agreements;

- Efforts or filings aimed at regaining Nasdaq listing compliance;

- Additional sponsor financing arrangements;

- Shareholder votes or amendments impacting redemption terms.

Failure to complete an initial business combination within approved timelines will likely result in winding-up procedures including orderly liquidation under Cayman Islands law thereby terminating shareholder positions definitively [S9].

ISRLF exemplifies structural vulnerabilities common among SPACs unable to commercialize deals timely: caught between deferred listing compliance pressures and mounting operational finance needs dependent on sponsor intervention amidst complex geopolitical risks embedded within its disclosures.

This analysis relies exclusively on disclosed financials and regulatory filings through early 2026 without extrapolation beyond stated facts or projections absent explicit company guidance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments