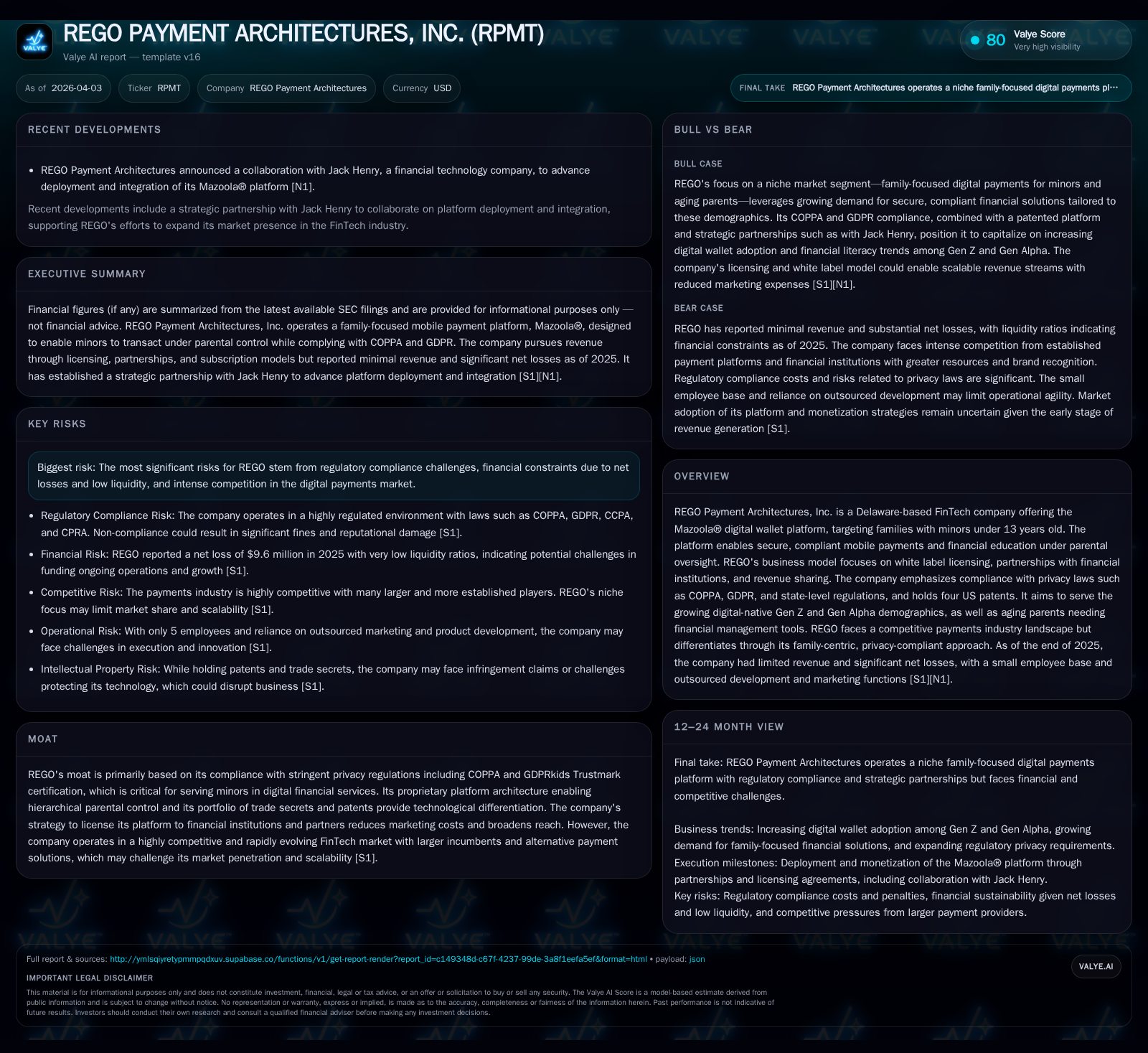

REGO Payment Architectures’ COPPA-Compliant Mazoola Platform Drives Revenue Growth Amid Continued Net Losses

REGO targets digital-native youth and aging parents with a white-label family payments platform amid competitive FinTech pressures.

REGO Payment Architectures, Inc. operates the Mazoola® digital wallet platform focused on secure, compliant mobile payments for families with minors, emphasizing privacy regulation compliance and parental controls. The company has generated limited revenue but is pursuing growth through white label licensing partnerships with financial institutions and expanding product offerings to include services for aging parents. REGO’s competitive advantage is supported by its COPPA and GDPRKids Trustmark certifications and a portfolio of patents protecting its hierarchical account architecture. While losses continue due to ongoing investment in technology and integration, recent partnerships with major banking vendors provide pathways to monetization. Key risks include regulatory compliance costs, liquidity constraints, and intense competition in a fast-moving FinTech landscape.

Company History and Business Transition

Founded in 2008 as Chimera International Group, Inc., REGO Payment Architectures underwent several name changes before adopting its current identity in 2017 [S1][S23]. Initially focused on monetizing online gaming platforms through its "Oink®" product line (discontinued in 2016), the company shifted its strategy towards delivering a comprehensive family-oriented financial management solution. This repositioning addresses the unmet demand for child-friendly financial tools combined with educational content.

Headquartered in Blue Bell, Pennsylvania, REGO’s flagship product is the Mazoola® digital wallet—a COPPA- and GDPRKids-certified platform enabling transactions for children under parental supervision. Its master-subaccount architecture enforces spending controls aligned with stringent privacy regulations essential for safe operation within children's digital finance environments [S15][S19].

Historical Financial Performance

Financially, REGO remains an early-stage company characterized by minimal revenue generation alongside significant operating losses driven by ongoing R&D and operational investments. The financial summary below captures recent trends based on the latest available annual data [F1]:

Historical performance (annual)

| FY | Rev ($) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 2250 | -10 | -6 | -9 | -7.5% | |

| 2024 | -9 | -7 | -8 | |||

| 2023 | 2073 | -7 | -16 | 0.0% | ||

| 2022 | 2073 | -6 | -15 | -21.1% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 20.0 |

| 2024 | 23.6 |

| 2023 | |

| 2022 |

Source: SEC companyfacts cache [F1].

Note: Capital expenditures and shareholder returns are not reported.

Despite persistent net losses exceeding $9 million in 2025 and operating cash flow remaining negative at over $6 million annually, REGO showed some improvement in cash burn relative to prior years. However, equity remains deeply negative at approximately -$47.9 million due to accumulated losses exceeding invested capital [F1], underscoring the capital-intensive nature of the business.

Core Products and Market Positioning

Mazoola® is built around three core pillars:

- Privacy & Compliance: Full adherence to COPPA regulations governs data collection from minors under age 13; additionally certified under GDPRKids standards to address evolving privacy frameworks internationally [S15][S19].

- Parental Oversight: A hierarchical master-subaccount model enables parents to set spending rules that automatically control subaccounts for children; this structure supports compliance while fostering financial literacy.

- Family Financial Education: The platform integrates modules teaching saving habits, chore incentives, charitable giving options, investment simulations, and responsible money management.

This approach targets digitally native younger generations—Gen Z (born 1997–2010) and Gen Alpha (post-2010)—who increasingly rely on mobile payments but lack compliant youth-specific solutions; it also extends offerings to aging parents facing heightened financial exploitation risks [S16][S17].

Industry Context & Competition

REGO operates within a rapidly evolving FinTech environment marked by increasing adoption of digital wallets globally—estimated at $15 trillion in spending projected for 2025—with over half of consumers using mobile banking regularly [S16]. Competitors include established players like PayPal’s Venmo service, Amex Bluebird family accounts, FamZoo prepaid card products oriented toward families as well as emerging neobanks.

However, none fully replicate REGO’s combination of COPPA-compliant money management tools integrated with educational content and hierarchical parental controls—a technological moat reinforced by four granted U.S. patents covering parent-child data controls and age verification systems [S20].

Growth Initiatives and Future Prospects

Key growth strategies include:

- White-label Licensing: Licensing Mazoola® technology to banks and telecom vendors enables partners to offer compliant family wallets without developing proprietary infrastructure.

- Strategic Partnerships: Agreements with Computer Services Inc. (CSI), providing access to over 500 regional banks' customers; collaboration with Jack Henry & Associates extends potential reach into thousands of financial institutions nationally [S25].

- Product Expansion: Enhancements such as charitable giving features, health marketplaces targeting families; introduction of Senior Guard prototype addressing elderly parent care needs broaden market scope.

- Data Monetization: Exploring predictive analytics from anonymized transaction data sales or contextual advertising under strict privacy safeguards.

Operationally, the company has passed SOC 2 Type I and Type II audits indicating readiness for institutional adoption; system upgrades now support segregated databases facilitating multi-client deployments crucial for scaling white-label solutions [S25].

Capital Allocation / Liquidity Challenges

The company’s operations remain capital intensive given sustained R&D spending (~$3.3 million annually) focused on compliance technology development amid complex multi-jurisdictional regulation enforcement requirements including FTC oversight related to COPPA violations [S4][S15].

Liquidity constraints are significant: current liabilities exceed current assets by roughly twentyfold ($48 million vs $0.23 million), with cash equivalents totaling only $158k at year-end 2025 [F1][S11]. Funding has been supported primarily through private credit lines extended by existing shareholders—a $20 million unsecured line expiring March 2026 bearing interest at 7%—reflecting dependence on insider capital amid limited public market liquidity options [S12][S24].

No dividends or share repurchases have been declared given ongoing net losses consistent with early-stage growth companies.

Regulatory Environment Risks

Compliance is critical amidst a complex regulatory landscape encompassing federal laws (COPPA enforced by FTC), state-level statutes including California's CCPA/CPRA with new enforcement bodies across multiple states as well as international regulations such as GDPR applicable when processing EU citizen data [S11][S15][S27]. Non-compliance risks substantial civil penalties exemplified by recent multi-million-dollar settlements involving major platforms such as Google ($170M), TikTok ($5.7M), Epic Games ($275M).

REGO mitigates these risks through continuous investment in technology safeguards alongside participation in certification programs like PRIVO’s Kids Privacy Assured Program supporting adherence to evolving legal requirements [S15].

Outlook & Key Milestones

Critical near-term milestones indicating progress toward commercial viability include:

- Completion of second-tier financial institution white-label rollouts expected Q1 2026;

- Growth in subscription conversions coupled with increased transaction volumes demonstrating unit economics;

- Successful annual SOC audits evidencing sustained compliance;

- Management of liquidity via potential equity raises or refinancing beyond current insider lending;

- Expansion into additional verticals such as government social services payment platforms or closed-network catering systems reducing transaction overheads;

- Enhanced marketing efforts targeting Gen Z/Alpha families leveraging digital channels aligned with youth media consumption patterns;

- Monetization ramp-up from ancillary offerings including senior care wallet modules and compliant data analytics.

In summary, REGO Payment Architectures remains an embryonic-stage enterprise anchored by differentiated technology tailored for emerging generational payment behaviors but faces typical early-stage challenges including profitability gaps and liquidity pressures requiring disciplined execution around partnership-driven distribution while maintaining rigorous regulatory compliance.

This analysis is based exclusively on disclosed filings without extrapolation or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments